Related Articles

How Finalyse can help

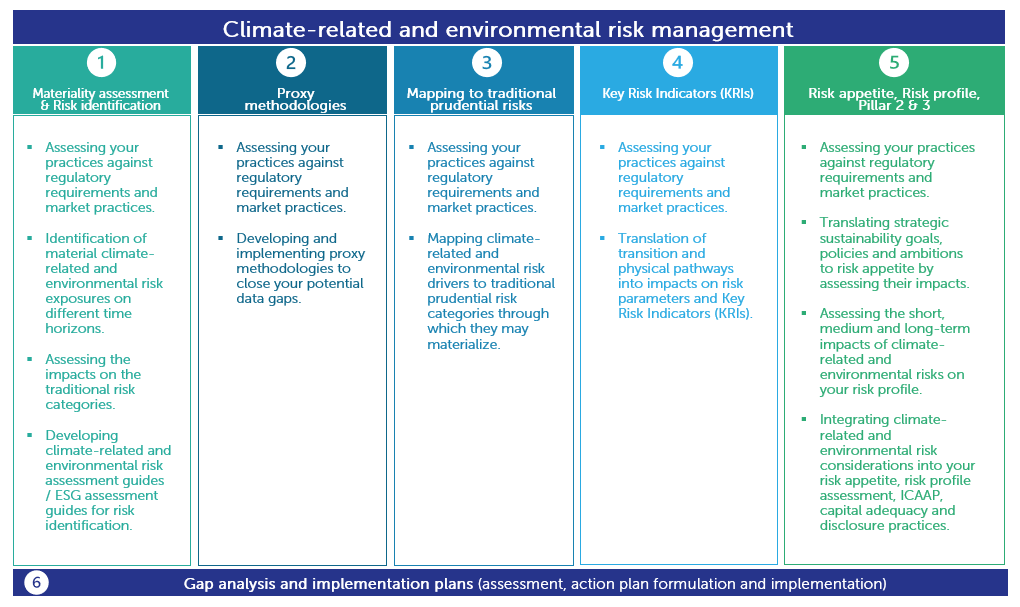

Climate-Related and Environmental Risk Management

Climate-related and environmental risks and the corresponding challenges will have important consequences to various aspects of our lives. Banks are expected to play a major role in for instance financing the transition to a sustainable economy and society.

In November 2020 the European Central Bank (ECB) published supervisory expectations towards the European banking sector: the ECB’s Guide on climate-related and environmental risks provides an overview of 13 recommendations related to Strategy, Governance, Risk management and Disclosures, and banks are expected to fully comply with them. Since then, an increasing number of national regulators and supervisors have also formulated similar expectations.

How does Finalyse address your challenges?

Gap Analysis and implementation plans:

Assessing your current practices, formulating and implementing action plans to remediate any shortcomings identified in the ECB Thematic review.

Materiality assessment and risk identification:

Identifying material risk exposures on different time horizons, and developing climate-related and environmental risk assessment guides / ESG assessment guides.

Proxy methodologies:

Developing and implementing proxy methodologies to close existing data gaps: from purely expert-based proxies to quantitatively well-underpinned methods.

Mapping to traditional prudential risks:

Mapping climate-related and environmental risk drivers (both transition and physical) to traditional prudential risk categories such as credit risk and market risk.

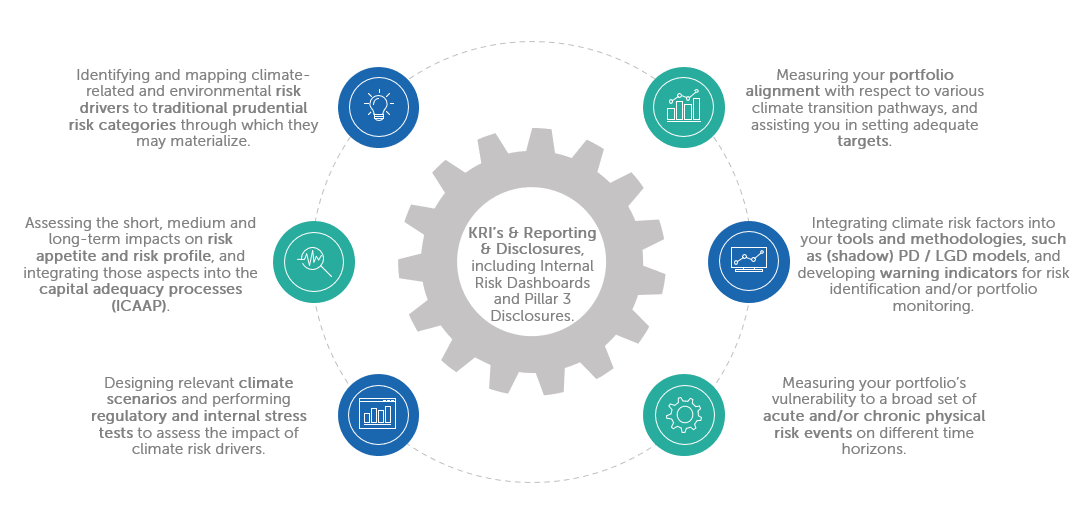

Key Risk Indicators (KRIs):

Translating transition and physical pathways into impacts on risk parameters and KRIs in order to monitor and actively manage the corresponding risks.

Risk appetite and risk profile, ICAAP, capital adequacy and disclosures:

Assessing short, medium and long-term impacts on your risk profile, and integration into your risk appetite, risk profile assessment, Pillar 2 processes and disclosures.

How does it work in practice?

The ECB’s Guide on climate-related and environmental risks, published in November 2020, provides an overview of 13 recommendations related to Strategy, Governance, Risk management and Disclosures, and banks are expected to fully comply with them. Moreover, with the effects of climate change and environmental risks being more visible than ever in our daily lives and the way business is conducted, financial institutions are more inclined to incorporate corresponding objectives and targets into their practices. However, the effective management and measurement of climate-related and environmental risks remain challenging.

Financial institutions can use their well-established risk management practices and frameworks as a starting point, but they need to enhance them to address the climate-related and environmental risks’ unique features such as the combination of short and medium to long-term impacts, nonlinearities, potential tipping points and interconnectedness among various risk sub-types.

Past experiences in scenario analysis and stress testing also provide the financial industry with the opportunity to get a quantitative view on their exposures to the transition to a more sustainable (Paris Agreement aligned or Net Zero) economy and society, as well as on their exposures to physical risks corresponding to climate-related and environmental issues. Moreover, the ECB and an increasing number of national regulators and supervisors request banks to conduct materiality assessments, various risk identification and monitoring exercises, as well as climate risk stress tests on their portfolios while taking into account various transition scenario pathways.

As climate-related and environmental risk measurements (most importantly stress testing and portfolio alignment calculations) entail a significantly longer time horizon and different methodologies compared to traditional practices, many financial institutions will have to redesign – or enhance at least – their existing toolkits in many aspects of their risk management and risk measurement.

Since the publication of the ECB’s Guide on climate-related and environmental risks in November 2020, the ECB has carried out various assessments and inspections on the banks’ preparedness and practices:

- ECB supervisory assessment of climate risks disclosures,

- ECB climate stress test 2022,

- ECB thematic review of climate-related and environmental risks

which led to the overarching conclusions that banks still have a lot to do to ensure full compliance with the ECB’s recommendations.

How can Finalyse help you with climate-related and environmental risk management?

Together with its ‘Climate change risk measurement’ services, Finalyse offers a broad range of solutions in the domain of climate-related and environmental risks:

Key Features

- Benefit from Finalyse’s extensive experience in the area of risk management and risk measurement for financial institutions.

- Ensure compliance with the recommendations set out in the ECB’s Guide on climate-related and environmental risks.

- Understand the climate-related and environmental risk drivers, their transmission into traditional prudential risk categories and their risk management implications.

- Integrate climate-related and environmental risks into financial institutions’ existing toolkits, methodologies and frameworks by using a holistic approach.

- Benefit from Finalyse’s unique approach, tailored to the specific needs and circumstances of each financial institution.

Alexandre Synadino is a managing consultant with expertise in risk data analytics, climate risk management and regulatory reporting. He is an active member of the Finalyse Climate Risk Centre. His main area of expertise lies in the research, design and development of physical risk assessments using different tools and methods. Alexandre is involved in the conceptualisation of measurement approaches to cover multiple hazard types, geographies and scenarios to respond to regulatory demands for granular and forward-looking analyses.

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Our Insurance Services

Check out Finalyse Insurance services list that could help your business.

Our Insurance Leaders

Get to know the people behind our services, feel free to ask them any questions.

Client Cases

Read Finalyse client cases regarding our insurance service offer.

Insurance blog articles

Read Finalyse blog articles regarding our insurance service offer.

Trending Services

BMA Regulations

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Solvency II

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Outsourced Function Services

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Trending Services

AI Fairness Assessment

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

CRR3 Validation Toolkit

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

FRTB

In 2025, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Trending Services

Independent valuation of OTC and structured products

Helping clients to reconcile price disputes

Value at Risk (VaR) Calculation Service

Save time reviewing the reports instead of producing them yourself

EMIR and SFTR Reporting Services

Helping institutions to cope with reporting-related requirements

CONSENSUS DATA

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Blog

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

Regulatory Brief

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Materials

Read Finalyse whitepapers and research materials on trending subjects

Latest Blog Articles

Contents of a Recovery Plan: What European Insurers Can Learn From the Irish Experience (Part 2 of 2)

Contents of a Recovery Plan: What European Insurers Can Learn From the Irish Experience (Part 1 of 2)

Rethinking 'Risk-Free': Managing the Hidden Risks in Long- and Short-Term Insurance Liabilities

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Our Team

Get to know our diverse and multicultural teams, committed to bring new ideas

Why Finalyse

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Career Path

Discover our three business lines and the expert teams delivering smart, reliable support