BERMUDIAN REGULATIONS FOR (RE)INSURERS

The Bermuda Monetary Authority (the Authority, "BMA") oversees Bermudan commercial (re)insurers and (re)insurance groups. The BMA issued a statutory and prudential regime which achieved full equivalence with the European Solvency II regime, a feature currently achieved by only two jurisdictions in the world.

Finalyse has rich experience in Bermudan insurance regulations and offers you a comprehensive set of managed services and tailored solutions. Partner with Finalyse and let us take care of your compliance with BMA regulations.

How does Finalyse address your challenges?

Head of Actuarial Function:

Review of technical provisions for EBS, assessing appropriateness of actuarial methods, models and assumptions, data quality and providing an opinion on the CISSA.

Scenario-Based Approach:

Assistance in compliance with SBA requirements including SBA modelling, approval, liquidity reporting, reinvestment strategy and model governance.

Capital/CISSA/GSSA support:

Capital planning and optimisation, CISSA/GSSA projections and stresses, including climate risk scenarios (see also here). Filling out schedules and documentation and analysis of results.

Licensing:

Advise on BMA’s licensing requirements for new (re)insurers. Assistance in the submission of the application package. Implementation of the risk and actuarial framework, policies, standards, and procedures.

Approved Actuary / Loss Reserve Specialist:

Provide opinion on the adequacy of insurance reserves.

SAA support:

Specifying asset classes, defining objectives and constraints, forming capital market expectations, establishing asset class bandwidths, validating the optimal allocation, and optimizing the asset mix.

How does it work in practice?

The Authority is responsible for the licensing, supervision and regulation of financial institutions including those conducting deposit-taking, insurance, investment, and trust business in Bermuda.

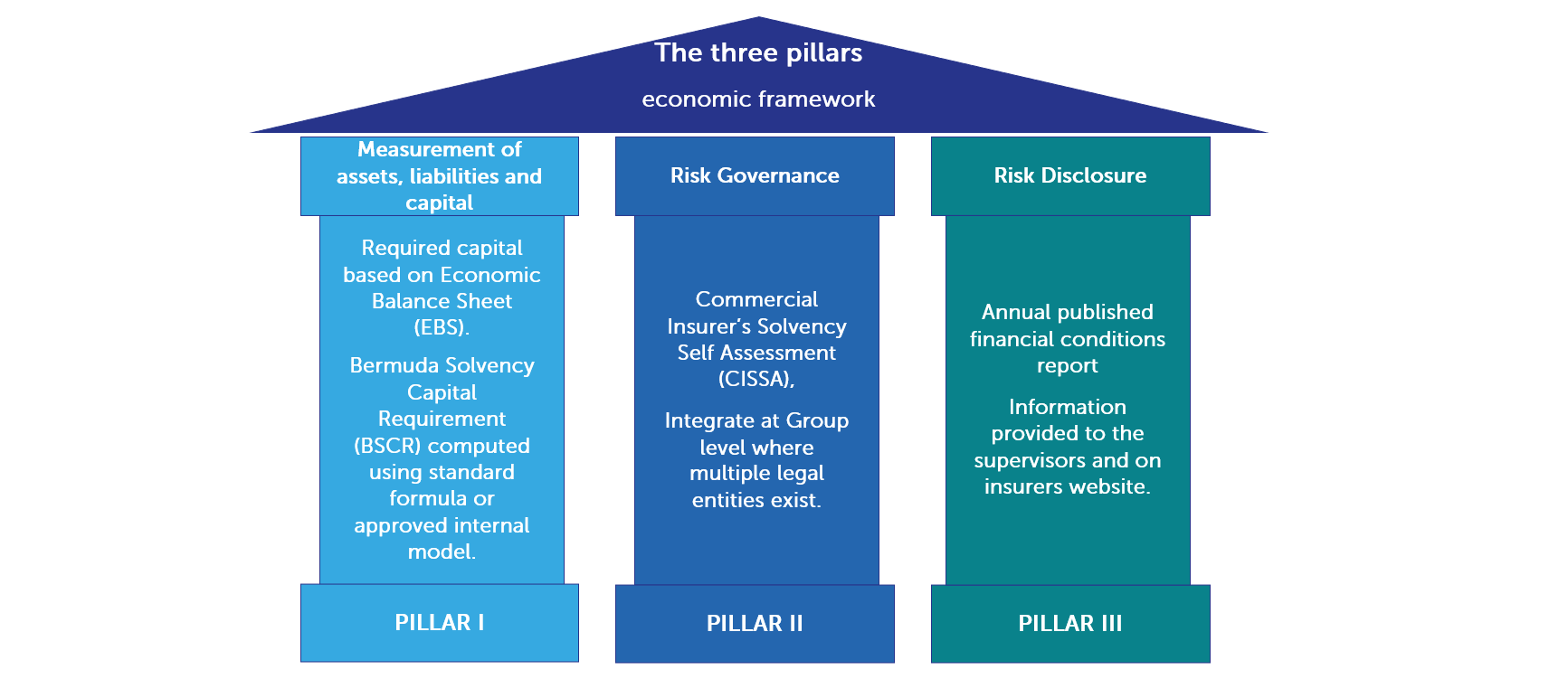

The BMA has a Solvency II equivalence and has a similar three pillar approach.

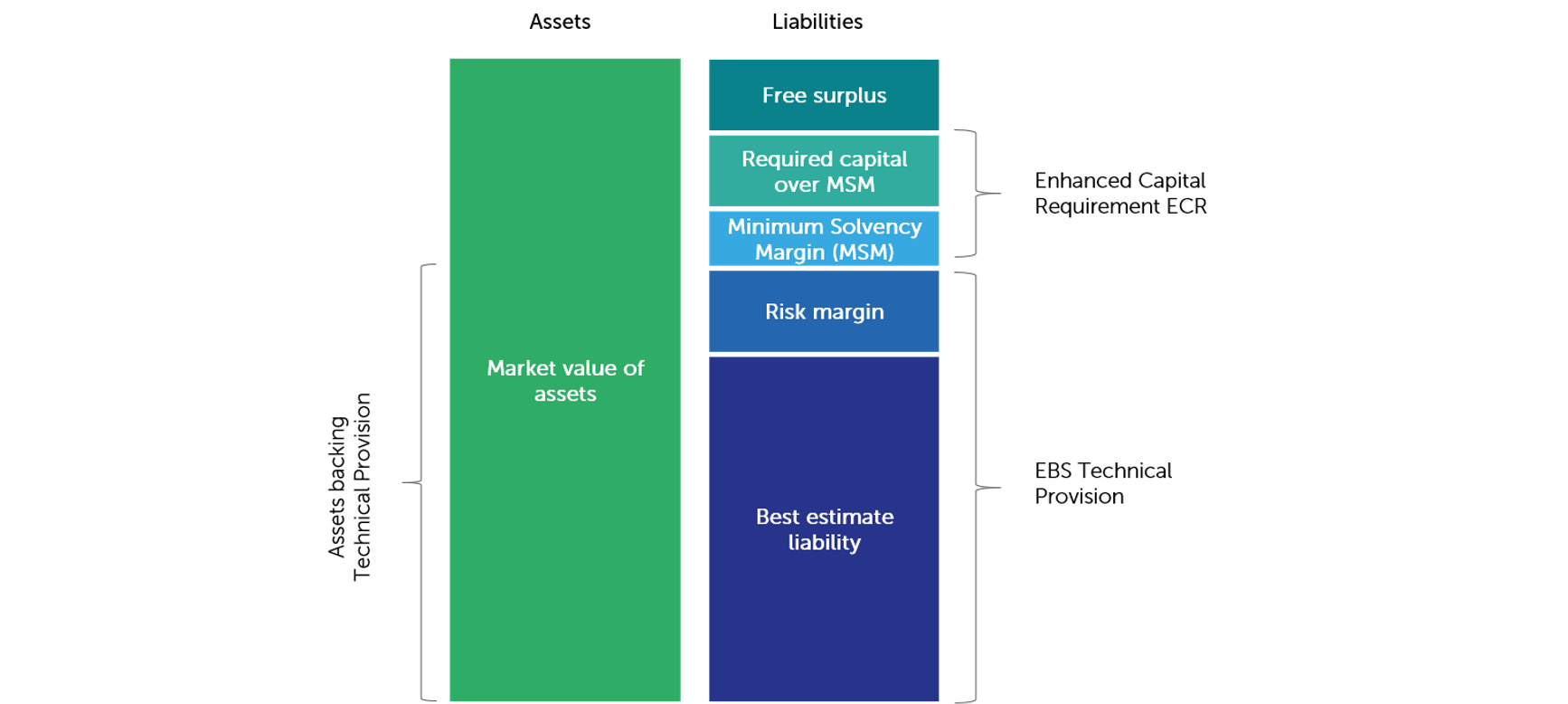

Principles of Economic Balance Sheet (EBS):

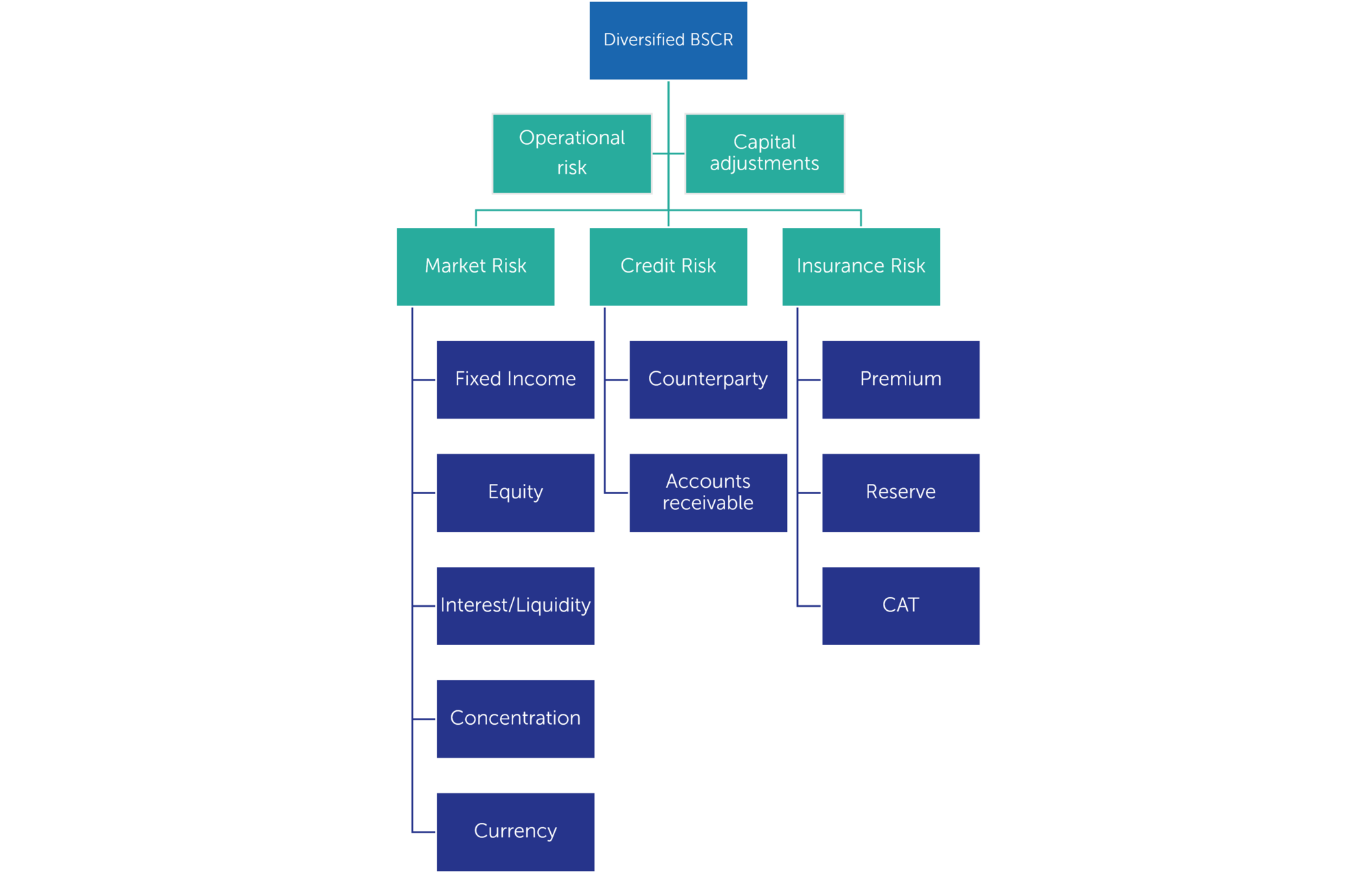

Principles of Bermuda Solvency Capital Requirements (BSCR)

Key Features

- Finalyse leverages on our extensive experience in Bermudan regulations thanks to the numerous services it has provided to BMA-regulated insurers. We can assist you in receiving approval from BMA to apply favourable capital treatment for assets and liabilities using private or internal ratings, strategic or infrastructure equity treatment or company/group specific parameters.

- We offer expertise on both the asset and liability sides of the balance sheet, such as actuarial modelling and model validation, submission of BMA returns, recovery planning, capital modelling and capital treatment of exotic assets and liabilities.

- You can also fully outsource the various key functions or processes required by the BMA to Finalyse by appointing one of our senior experts satisfying BMA’s fit and proper requirements.

Francis is a Principal Consultant in charge of our insurance practice in Dublin. He has 15 years of experience within the life and non-life (re)insurance industry. His expertise covers the areas of financial reporting, prudential regulation, and actuarial modelling. Francis has worked in both industry and consulting with extensive exposure to Solvency II and BMA-regulated clients and a keen eye on new regulatory developments.

Frans is an actuary and Financial Risk Manager with international experience in the pensions and insurance sectors. He has been specialising in actuarial valuations (AXIS), financial and regulatory reporting (IAS19, US GAAP, IFRS2, IFRS17), regulatory reporting (IORP II, Solvency II, ICS, BMA), market risk management (ALM, SAA), climate change risk management and investment consulting.