Related Articles

Solvency II

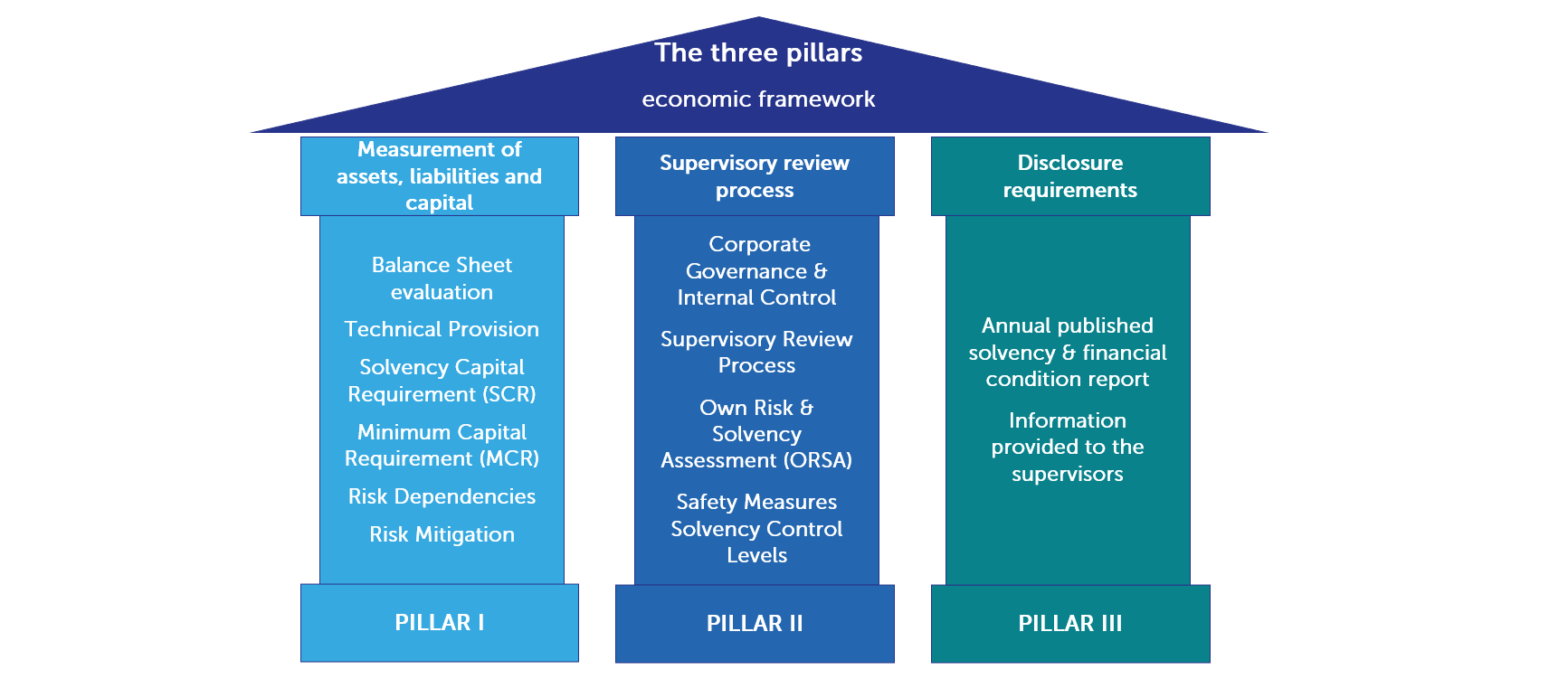

The Solvency II regime introduced on 1 January 2016 is a harmonised, sound and robust prudential framework for insurance firms in the EU. It is based on the risk profile of each individual insurance company in order to promote comparability, transparency and competitiveness.

Finalyse offers you a comprehensive set of managed services and tailored solutions. Partner with Finalyse and let us take care of your compliance with Solvency II regulations.

How does Finalyse address your challenges?

HoAF Support:

Assist with the calculation of technical provisions including assessing appropriateness of the methods, models, assumptions and data and populating QRT's, SFCR and RSRs.

Capital Modelling support:

Production of the Solvency II Capital Requirements and supporting analysis including maintaining capital model is maintained in line with the internal governance framework systems.

ORSA support:

Capital planning and capital optimization, production of ORSA projections and stresses, communicating complex concepts and recommendations to multiple stakeholders and influencing decisions through sound analytical rationale.

SAA support:

Specifying asset classes, defining objectives and constraints, forming capital market expectations, establishing asset class bandwidths, validating the optimal allocation and optimizing the asset mix.

Strategic and operational:

Actuarial support on strategic initiatives, streamline the actuarial process and enhancements to the Actuarial Function including policies, processes and tools.

Peer reviews:

Review of assumptions, methodologies, material uncertainties and potential deteriorations, expert judgement, appropriateness of models and reasonableness of the HoAF’s conclusions.

Key Features

- Finalyse offers extensive experience and expertise on both the asset and liability sides of the balance sheet, which provides the necessary scope of knowledge and skills to help determine the solution that is optimal for your business.

- Leverage on our experience in areas beyond financial reporting, such as actuarial models, IT systems including data management and storage capacities, risk management including ALM and hedging, product design, business strategies and remuneration.

- You can choose from a comprehensive set of managed services and tailored solutions to support you with various elements of Solvency II compliance, such as implementation of the key functions, performing and reviewing technical calculations, actuarial model development, risk management (including ALM and hedging), ORSA production and reporting.

- You can also fully outsource the various key functions required by Solvency II to Finalyse by appointing one of our senior experts with previous experience to fulfil these functions.

François-Xavier is a Principal Consultant with advanced expertise in Financial Markets, ALM and Risk Management, covering both banks and insurance companies. On the banking side, François-Xavier is a practice leader on Valuation, IRRBB, FRTB, VaR, Initial Margin and Counterparty Risk, well acquainted with the regulatory requirements and the market practices surrounding market risks. On the insurance side, François-Xavier has extended experience in the regulatory treatment of financial instruments, ORSA, and hedging balance sheets against interest rate, credit spread and inflation risks.

Divyank is a Senior Consultant with more than 8 years of experience and a part qualified Actuary. He has acquired expertise in Solvency II, IFRS17 and MCEV reporting and has worked for life and non-life business. He has extensive experience in Prophet modelling, DCS, statutory valuation and IFRS17 implementation and his coding skills include Prophet and DCS modelling, SAS, VBA, R.