Agile and comprehensive assessment, measurement and management of your market and liquidity risks

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Helping you comply with the Solvency II regulations as well as optimising your Solvency II balance sheet

Gary is a Principal Consultant within our insurance practice in Dublin. He has 16 years of experience within the life and non-life (re)insurance sectors covering industry, audit and consultancy roles. His expertise covers financial reporting, prudential and conduct risk management, and assurance activities. Gary has provided outsourced actuarial, risk, compliance, and internal audit function services for a wider range of insurers, reinsurers and captives.

In April 2025, the European Insurance and Occupational Pensions Authority (EIOPA) (‘EIOPA’) presented its draft regulatory technical standards (‘RTS’), in the form of a consultation paper (EIOPA-BoS-25-097), to specify its expectations for contents of pre-emptive recovery plans. This consultation comes in advance of the introduction of the Insurance Recovery & Resolution Directive (‘IRRD’). Recovery planning is not a new concept for all (re)insurers in Europe, however. In 2021, the Central Bank of Ireland (‘CBI’) marked the introduction of recovery planning regulations for Irish domiciled (re)insurers by publishing their document 'Recovery Plan Guidelines for (Re)Insurers'.

This two-part article compares the EIOPA and CBI regimes, highlighting how European insurers can learn from the Irish experience whilst also examining differences between the two frameworks.

In Part 1, we consider:

Both EIOPA and CBI regimes are prescriptive regarding the headings for inclusion in a recovery plan. There is significant overlap in the section headings required.

Article 2 of the EIOPA draft RTS stipulates that the following headings should be included:

Section 5.1 of the CBI guidelines, in comparison, requires the following headings:

Article 3(1) of the RTS bears similarities to Section 5.6 of the CBI document with both requiring a clear description of the undertaking including:

The CBI requirements further oblige undertakings to consider the ability to separate the insurer from its broader group and actions needed to secure continuity of critical functions upon such separation.

Article 3(3) of the RTS states that insurers should include details on any material changes since the prior plan. Section 5.3 of the CBI has a similar objective, albeit adopts a more prescriptive approach requiring explicit inclusion of any changes to:

Article 4(1) of the RTS and Section 5.7 of the CBI document both require insurers to include a framework of recovery indicators in their recovery plans. Clear triggers, limits and thresholds that are forward-looking are required under both.

Both frameworks also call for a series of leading indicators tailored specific to the insurer's business model and key vulnerabilities. Article 4(2) of the RTS adopts a principals-based approach with insurers required to develop indicators relevant to their business. Indicators relating to capital are the only explicitly stated minimum requirement.

Section 5.7 of the CBI document is more prescriptive and lists categories of recovery indicators which should be considered, including:

The Annex to the CBI guidelines includes additional guidance on what could be included within each of the above indicator categories. Solvency- and liquidity-related indicators are considered compulsory at a minimum.

Both frameworks stipulate that insurers should include explanations on the choice of indicators included. Again, however, IRRD is less prescriptive, simply stating that rationale should be provided.

Section 5.7(3) of the CBI guidelines states that the framework of indicators which must be:

An insurer should be able to provide the Central Bank with an explanation of how the specific calibrations of the recovery indicator thresholds have been determined.

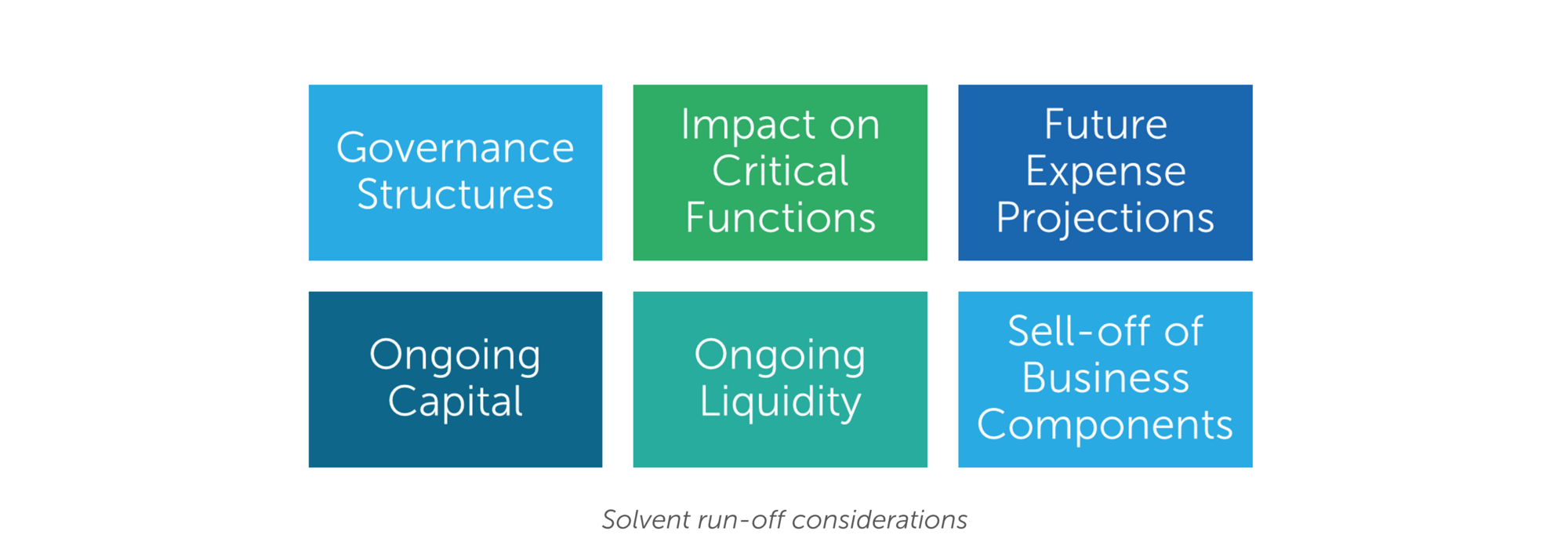

Both regimes emphasise the importance of indicators being designed to allow sufficient time for Boards and regulators to react and respond to emerging stress events. Though again, the CBI’s requirements are more detailed:

The CBI document, Section 5.7(4), make explicit reference to factors that should be considered in determining the point of closure to new business, namely:

Solvent run-off indicators do not receive focus under the IRRD proposed rules.

Both frameworks expect recovery plan governance to be integrated into the insurer’s normal systems of governance. Under both sets of requirements, sufficient narrative description must be provided to detail how the recovery plans were drawn up, and how plans would be implemented in a stressed scenario.

Plans should include specific details around:

While both regimes are very similar, IRRD places a little extra emphasis on factors that could trigger ad-hoc updates to recovery plans (Article 5). The CBI stresses the need to explore reporting and operational capacity under stressed conditions, and any impediments to such. The Irish regime also homes in on preparatory measures taken to improve effectiveness of the plan (Section 5.4 and 5.11).

While different terminologies may be used, both European and Irish regulations bear great similarities around recover planning expectations in respect of plan contents, recovery indicators and governance. The Irish requirements are slightly more prescriptive in places, though such prescriptiveness can offer useful guidance for those drawing up first time recovery plans.

In Part 2 of this article we will scrutinise remedial actions, scenario analysis and communications strategies.

A pre-emptive recovery plan is designed to help insurers prepare for severe financial stress by outlining actionable steps to restore financial stability while remaining solvent. Both the IRRD (via EIOPA) and the Central Bank of Ireland (CBI) frameworks aim to ensure that insurers can respond promptly to emerging risks through predefined indicators, governance procedures, and recovery options. These plans are not only regulatory obligations but also serve as practical tools for strengthening operational resilience.

While both EIOPA and the CBI require broadly similar elements - such as recovery indicators, governance frameworks, and summary sections - the CBI guidelines are generally more prescriptive. For instance, the CBI specifies categories of indicators (e.g., solvency, liquidity, profitability) and requires detailed rationales for indicator selection. EIOPA, by contrast, adopts a more principles-based approach, allowing for flexibility but also placing more onus on insurers to justify their methodologies.

Ireland’s earlier implementation of recovery planning regulations has provided valuable clarity and precedent for what robust plans look like in practice. The CBI’s prescriptive approach offers insurers concrete examples and expectations - especially helpful for firms preparing recovery plans for the first time under the upcoming IRRD. By studying the Irish framework, insurers can better understand regulatory expectations, avoid common pitfalls, and build plans that are both compliant and operationally effective.

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support