Written by Veronica Mazza, Senior Consultant

Nowadays, climate and environmental (C&E) risks are impossible to ignore. It has become clear that climate-related risk shocks could spread throughout the financial system, notably in the form of potential disorderly green transition or the intensification of physical risk phenomena.

Financial market losses linked to a sudden repricing of the climate risks could affect investment funds and insurers as well as trigger defaults and credit losses for banks. Supervisors are also concerned about the extent to which banks’ exposures to physical and transition risks stemming from C&E risks may affect the safety and soundness of the entire financial system.

Hence, in recent years, the ECB has launched targeted actions to include C&E risks in its ongoing supervision and has indicated addressing C&E risks in its list of priorities for 2022-2024. This article aims to go through the most relevant steps of the 2022 ECB supervisory C&E agenda and leverages on the results of the 2022 ECB climate stress test to provide preliminary commentary regarding banks’ preparedness for the existing and upcoming requirements.

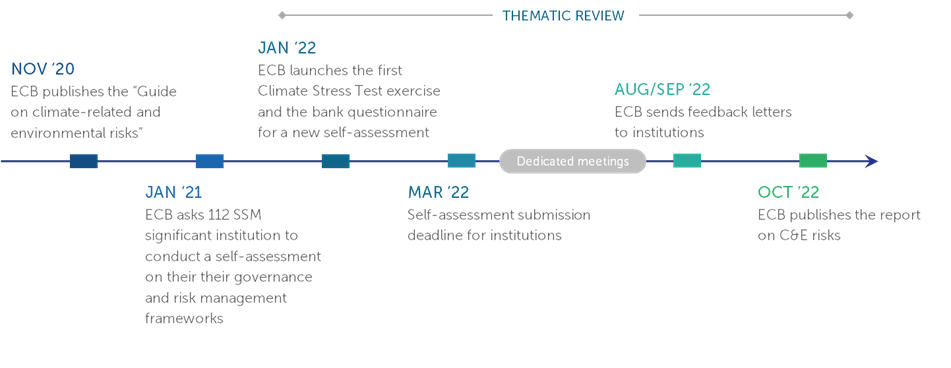

In November 2020 the ECB published the “Guide on climate-related and environmental risks” appealing on institutions to take a strategic, forward-looking and comprehensive approach in considering climate-related and environmental risks.

In the Guide the ECB set out 13 supervisory expectations for banks when formulating and implementing their business strategy, governance and risk management frameworks, and to become more transparent by enhancing their C&E risk disclosures.

It was clear that the efforts of supervisors to ensure banks address risks stemming from climate change and environmental degradation would continue.

Therefore, in 2021, in the first ever exercise of its kind, the ECB comprehensively assessed the state of C&E risk management in the banking sector asking 112 significant institutions to conduct a self-assessment of their practices related to the 13 supervisory expectations and to submit implementation plans detailing how and when they would bring their practices in line with the Guide. Since then, the ECB has performed several assessments on these practices and monitored the progress made in order to identify shortcomings on an institution-by-institution basis.

With the aim of further enhancing banks capacity to assess, quantify climate-related risks, in January 2022 the ECB launched the first bottom-up Climate Stress Test (CST) exercise. This initiative should be seen as a joint learning activity - for supervisors, for banks, and for the financial industry as whole – carried out to enhance understanding of all the relevant players in the financial industry1 about the importance of C&R risks and to strengthen supervised banks’ efforts to modelling climate risk and integrating it into existing models.

The 2022 CST results have helped competent authorities in assessing institutions’ preparedness to meet the supervisory expectations regarding climate risk management and practices. The other most relevant targeted action of the 2022 Supervisory Roadmap on C&E risks, the Thematic Review, is intended to serve similar purpose.

In the first half of 2022, along with the CST exercise, ECB has conducted the Thematic Review on C&E risks, which consists of a comprehensive deep dive into banks’ practices related to strategy, governance and risk management in the context of climate-related risks.

After setting-up dedicated meetings with institutions, the ECB is going to provide them with final feedback letters summarising the supervisory observations. The 2022 ECB C&E risks agenda will be completed with a final report on C&E risks published later this year.

After the release of the “Guide on climate-related and environmental risks”, the ECB announced a follow-up in three concrete steps. In early 2021 the ECB asked institutions to conduct a self-assessment in the light of the supervisory expectations outlined in the Guide and to draw up implementation plans to advance their management of C&E risks. In early 2022 the ECB has conducted a thematic review of institutions’ C&E risk management practices, an assessment on banks’ progress towards transparent disclosure of their C&E risk profiles and a supervisory stress test as it gradually integrates C&E risks into its Supervisory Review and Evaluation Process (SREP) methodology. This integration will eventually influence institutions’ Pillar 2 requirements.

The 2021 self-assessment provided supervisors with the state of play of the banking sector’s C&E risk management in relation to the ECB’s Guide expectations. It showed that institutions had started to incorporate C&E risks into their business environment and strategy-setting arrangements. Many of them had integrated C&E risks into related procedures and policies and roughly two-fifths of the 112 Single Supervisory Mechanism (SSM) significant institutions had included C&E risks into their regular monitoring of the business environment. However, broadly speaking, none of the institutions were close to fully aligning their practices with the supervisory expectations.

Supervisors found that institutions had started incorporating C&E risks into their lending policies and adapting their governance structures. However, when it came to the integration of C&E risks into the risk management framework as part of their ICAAP/ILAAP2 only a few of institutions had taken significant steps.

The assessment reported that relevant rooms of improvement still remained, mostly in the following areas:

Nevertheless, supervisors observed that almost all institutions had developed implementation plans to align their practices to the Guide expectations, although the adequacy of the plans and the shared timelines for addressing the existing gaps were widely poor.

As mentioned, the Climate Stress Test exercise carried out early this year has served the purpose of providing guidance to banks and helping them strengthen climate risk-related data collection and models development.

Based on the 2022 CST findings, the percentage of banks reporting that they have a climate risk stress-testing framework in place (as of the reference date of 31 December 2021) stand at around 40%3 against the 25% reported during the 2021 self-assessment.

Although some improvements were achieved since 2020, the exercise still highlighted weaknesses in climate-related risk management and processes.

The lack of quality and availability of data remains major challenge for many institutions. Banks need to invest more in climate-relevant data collection and become less dependent on the use of proxies. Climate-related data availability is one of the key factors that makes banks struggling in developing proper stress-testing frameworks and strengthening risk management more broadly.

Many deficiencies are also reported in institutions capacity to incorporate climate-related key risk indicators in their exiting framework, consider climate risk stress test results when implementing their business strategy and ensure independence between the development and validation processes in climate risk stress-testing exercise.

As already mentioned, in the first half of 2022 the ECB has conducted a thematic review on C&E risks which, along with the Climate Stress Test submission, are the main vehicle to assess where the banking sector stands in the context of awareness and management of climate-related risks and environmental degradation.

The main purpose of the review, carried out by the ECB in cooperation with the national competent authorities, is to follow up on the self-assessment exercise conducted last year investigating institutions’ climate-related and environmental strategies, as well as their governance and risk management frameworks and processes. The outcomes will feed into the SREP from a qualitative point of view, along with the Climate Stress Test results. The findings of both 2022 supervisory activities could indirectly impact Pillar 2 requirements through the SREP scores.

The preliminary results of the 2022 thematic review suggest improvements in banks actions to align their practices to the Guide’s expectations. The results also indicate that while a growing number of banks have deemed themselves to be materially exposed to C&E risks in the short to medium term, there are some that have not yet performed a materiality assessment.

Regarding banks’ disclosure of their C&E risks, set out by Expectation 13 of the Guide (Disclosure policies and procedures), the gap analysis reported that only few institutions have integrated climate-related and environmental risks into their disclosures policies. Roughly three-quarters of the institutions do not disclose whether climate-related and environmental risks have a material impact on their risk profile. This means that these institutions are unaware of the potential impact of the risks on their balance sheets or, more likely, they are aware of the impact but they are not able to quantify it due to the lack of available data and measurement techniques.

The ECB also observed that only about one in five institutions discloses the methodologies, definitions and criteria for all of the figures, metrics and targets reported as material. More than one-third of institutions do not disclose these aspects at all.4

Following the dedicated meetings, the ECB has finalised the thematic review on C&E risks, which is resulted in a detailed overview of final observations and supervisory feedback on a institution-by-institution basis. The ECB is going to share with each bank a benchmarking view and a final feedback letter with the main results of the supervisory assessment and to communicate the expected remediation dates for the identified shortcomings.

Mirroring the imperative need to manage and take into account C&E risks in all banks’ processes, climate-related topics will come to form an integral part of the ongoing supervision and the supervisory review and evaluation process (SREP). This may ultimately influence banks’ minimum capital requirements. From this perspective, the urgency for institutions to keep developing their climate-related risk management capabilities and to improve their awareness about the impact of both physical and transitional risks on the financial sector is constantly increasing.

Considering the importance and long-lasting nature of climate change and environmental degradation, the ECB asks SSM significant institutions to intensify their efforts in measuring and managing C&E risks in line with its expectations.

The 2022 ECB C&E risks Supervisory Roadmap is about to be fully completed. The preliminary available results derived from the complex architecture of the joint activities carried out by the supervisors show that some improvements have been made by the SSM significant institutions to assess, manage and disclose their C&E risks.

Nevertheless, the ECB reported that clear gaps between its expectations and banks practices still remain. Banks are supposed to submit reliable and adequate action plans detailing how and when they would fully align their practices with the Guide. In parallel, the ECB will gradually integrate climate-related and environmental risks into its methodology for the SREP, which will influence Pillar 2 capital requirements, as well as its on-site inspection methodology. The ECB sees reasonable that banks can be fully compliant with all the expectations by the end of 2024 at the latest.

In order to be able to meet this deadline, banks need to speed up in the development of climate-related risk models planning adequate processes that allow them to fill all the existing gaps and to fully integrate C&R risks in their risk management framework.

It is also worth noting that the transition to a more green and sustainable economy requires a comprehensive structural transformation of the economic system as a whole. Hence various other agencies, including the International Energy Agency (IEA), have set out pathways for the transformation of the economic sectors to achieve a clean and resilient energy system.5 Financial institutions have already tried to assess and disclose the alignment of their financing activities in the most relevant transition sectors.

In the near future, institutions will be required to disclose relevant alignment metrics by sector and estimate the distance between their financing and the 2030 milestones defined by the IEA scenario.6 Moreover, institutions will be asked to develop transition plans and manage and disclose risks relating to misalignment with the transition, and supervisors will be mandated to scrutinise these plans.

1. Although it is worth noting that only supervised institutions have been practically involved in the Climate Stress Test exercise.

2. Internal Capital Adequacy Assessment Process/ Internal Liquidity Adequacy Assessment Process.

3. For further details see “ECB – 2022 Climate Stress Test” (July 2022).

4. For further details see “Supervisory assessment of institutions’ climate-related and environmental risks disclosures” (March 2022).

5. See “Net Zero by 2050 – A Roadmap for the Global Energy Sector”, International Energy Agency, revised version (October 2021).

6. EBA/ITS/2022/01, final report implementing technical standards on prudential disclosures on ESG risks in accordance with Article 449a CRR.

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support