Related Articles

How Finalyse can help

Transition Risk Measurement

We equip financial institutions with advanced, data-driven assessments: ESG scorecards, scenario analysis, and PD model stress testing, to identify, assess, mitigate, and report climate transition risks, while supporting sustainable growth in a transitioning economy.

Transition risk assessment is not just about managing risks, it’s about embracing the future of finance. Let Finalyse help your bank navigate the transition to a low-carbon economy with confidence, ensuring long-term resilience and success.

How does Finalyse address your challenges?

Gap Analysis and Action Plans for Compliance

Detailing differences in the organisation’s current transition risk assessments

Measurement of Transition Risk on portfolio

Assessing the potential financial impact on the portfolio and strategic rebalancing in response to transition pathways

Transition Risk PD Tool

Conductging a fully customizable transition risk scenario analysis and stress testing are conducted based on NGFS scenarios, by adjusting the default ratings (PD) of the counterparties.

ESG Score Card

Development of an ESG scorecard based on the bank’s portfolio, by selecting an appropriate set of factors for the Environmental, Social and Governance Pillar. The factors will cover both qualitative and quantitative aspects.

Regulatory Compliant

Our methodologies match the ECB’s and ESRS requirements in terms of assessment level, time horizon, documentation, and measurement of materiality.

Workshops

Gain an understanding of best practices and methodologies applicable to identifying, assessing, measuring and reporting climate-related and environmental risks considering the upcoming regulatory, supervisory and market pressure.

How does it work in practice?

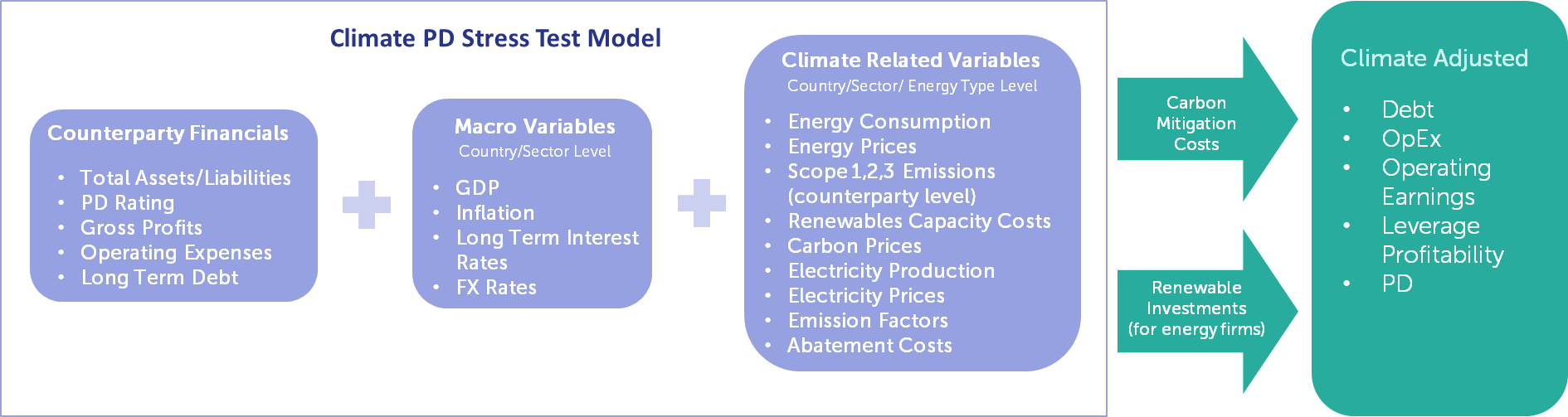

Transition risk PD tool

Finalyse has developed a powerful, forward-looking tool to perform transition risk analysis and stress testing. It is designed to compute climate-risk adjusted financials for corporates under multiple climate scenarios and years. The dynamic nature of the tool allows to quantify investments and economic costs associated with transition risk for corporates. The tool assess the impact of transition to a low carbon economy on a counterparty’s probability of default (PD). Results are then aggregated by sector, scenario and country.

Grounded in the methodology of the ECB’s economy-wide climate stress test, our approach has been enhanced to incorporate all NGFS climate scenarios and is applicable globally, beyond Europe. The tool is completely customizable as per any bank’s portfolio.

Key features of the tool:

- Projected energy consumption of counterparties based on their sector-specific energy mixes

- Country-level energy mix trajectories

- Pathways for renewables adoption and phasing out of brown energy

- Pathways for Macro variables and prices

- Climate-adjusted PDs

ESG Scorecard

Finalyse has developed a fully customizable ESG Scorecard methodology that selects appropriate set of factors for the Environmental, Social and Governance dimensions.. These factors cover both qualitative and quantitative aspects, and their selection depends on the specific purpose of the scorecard.

Under this methodology, the subfactor performance is translated into a score, by comparing the subfactor of the counterparty to a peer group. This peer group may consist of companies from the same geography, market, industry, or a combination thereof.

Prior Experience

Multilateral Financial Institution in Luxembourg: Development and implementation of a transition risk PD projection tool for the bank’s corporate portfolio, to strengthen their climate risk management

- Developed a tool to model the impact of transition risk on the corporate’s probability of default (PD), and then to aggregate by sector, scenario and country

- Analyzed the portfolio resilience, mitigation cost and investments in-line with climate adjusted PDs

Financial Institution in Brussels: ESG Tagging Project

- Spearheaded the exploration and documentation of sourcing logic for three key ESG tagging variables: ESG Purpose Transaction, EU Taxonomy Aligned Assets, and EU Taxonomy Aligned Transitional Assets.

- Delivered a comprehensive specification document outlining data sources, transformation rules, and business logic to support ESG reporting and compliance.

- Developed an SPSS-based analytical tool to estimate CO2 emissions for Alpha Credit’s car loan portfolio (2020–2023), applying the WLTP (Worldwide Harmonised Light Vehicles Test Procedure) methodology.

- Integrated EEA (European Environment Agency) datasets to map vehicle models with corresponding emission factors, enabling automated ESG tagging and environmental impact assessments.

Managing Consultant

Expert Climate Risk

Key Features

- Finalyse offers extensive experience and expertise in area of ESG and climate related assessment for financial institutions.

- Ensure compliance with the ECB and CSRD recommendations set out by ESRS, by conducting a robust transition risk measurement.

- Benefit from Finalyse’s unique approach, tailored to the specific needs and circumstances of each financial institution.

- Long Term Sustainability: A transition risk assessment aligns banks’ operations with broader societal goals like reducing carbon emissions and meeting the Paris Agreement targets.

Alexandre Synadino is a managing consultant with expertise in risk data analytics, climate risk management and regulatory reporting. He is an active member of the Finalyse Climate Risk Centre. His main area of expertise lies in the research, design and development of physical risk assessments using different tools and methods. Alexandre is involved in the conceptualisation of measurement approaches to cover multiple hazard types, geographies and scenarios to respond to regulatory demands for granular and forward-looking analyses.