Related Articles

How Finalyse can help

Corporate Sustainability Reporting Directive (CSRD) for Banks and Insurers

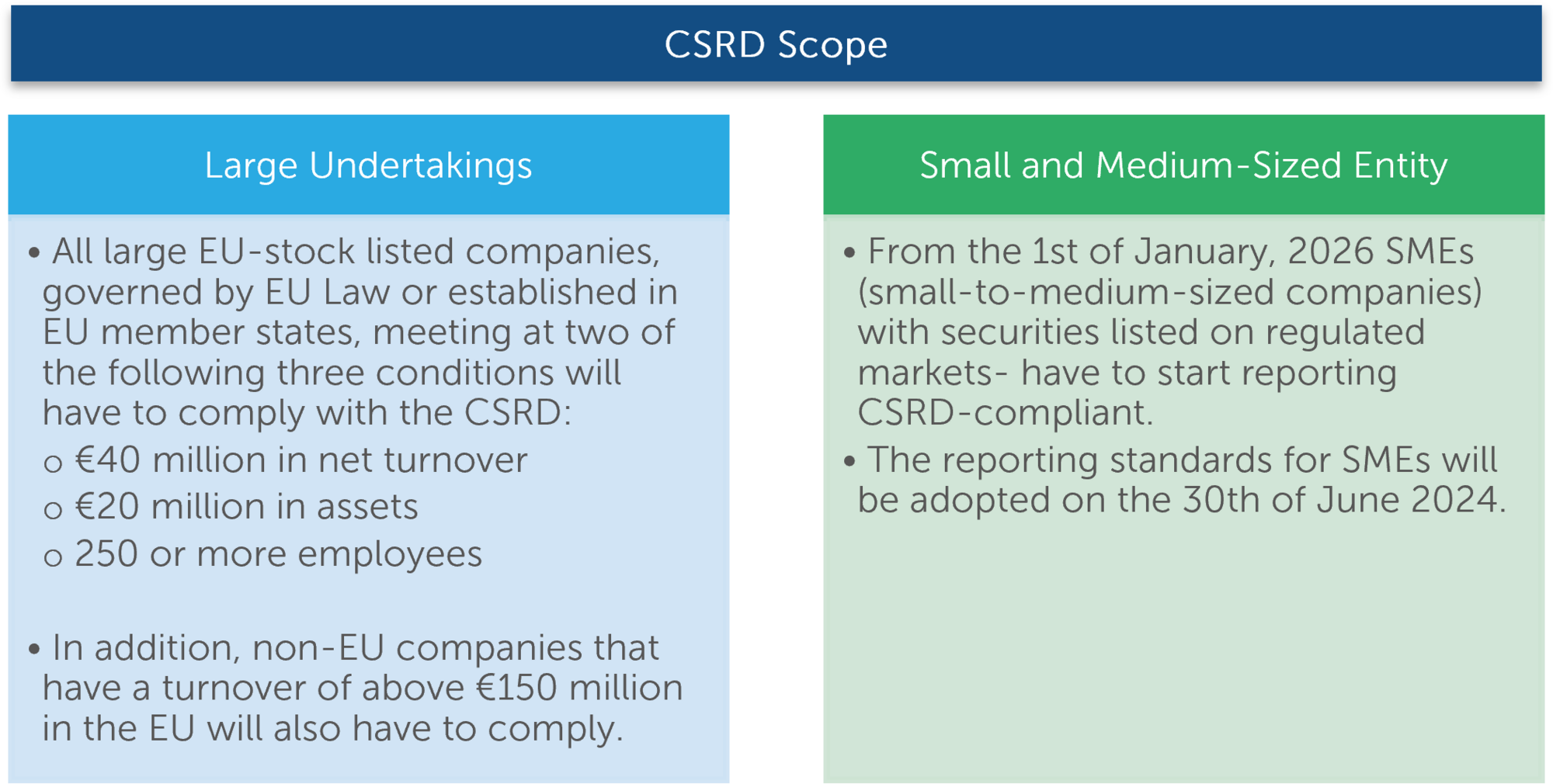

The Corporate Sustainability Reporting Directive (CSRD) entered into force in the EU on January 2023, replacing the Non-Financial Reporting Directive (NFRD). The CSRD broadens the spectrum of sustainability reporting from the 11,000 institutions covered by the NFRD to the nearly 50,000.

CSRD’s reporting framework-European Sustainability Reporting Standards (ESRS), lay out 12 chapters with over 80 disclosures, covering categories ranging from carbon emissions, pollution, waste disposal, biodiversity, social and governance. Importantly, these standards are mandated to feature in annual reports alongside financial statements, subject to stringent third party limited assurance.

The CSRD presents a unique opportunity for banks, insurers, and asset managers to integrate Environmental, Social, and Governance considerations into their fundamental business strategies. However, navigating the disclosure requirements and devising an effective reporting strategy can pose significant challenges.

Finalyse possesses extensive expertise in sustainability and climate related disclosures, enabling us to assist financial institutions in navigating the evolving CSRD landscape.

How does Finalyse address your challenges?

Governance

Establishing clear governance structure with defined roles and responsibilities within the organisation.

Double Materiality Assessment

Identification and assessment of the material risks and opportunities through the “Double Materiality” lens, considering Impact and Financial Materiality.

Gap Analysis

Producing a gap analysis, detailing differences in the organisation’s current disclosures to the CSRD requirements and proposing a roadmap for implementation of the CSRD reporting in line with the ESRS.

Limited Third-Party Assurance

Prepare for and obtain limited assurance.

Workshops

Conducting workshops for senior stakeholders, to promote an understanding of the key principles, reporting obligations, and timelines within CSRD.

Strategy Development

Setting KPIs and metrics aligning with CSRD requirements and inclusion in the existing policies to inform business strategy.

How does it work in practice?

The CSRD directs the European Financial Reporting Advisory Group (EFRAG) to establish a reporting framework called the ESRS. In total, the 12 chapters of the ESRS contain over 80 disclosures, and over 1000 both quantitative and qualitative data points related to those disclosures. The framework includes Cross- Cutting standards for reporting, required of all organizations governed by the CSRD, while the Topical standards for reporting - environmental, social and governance is mandatory for only those organizations that consider them material.

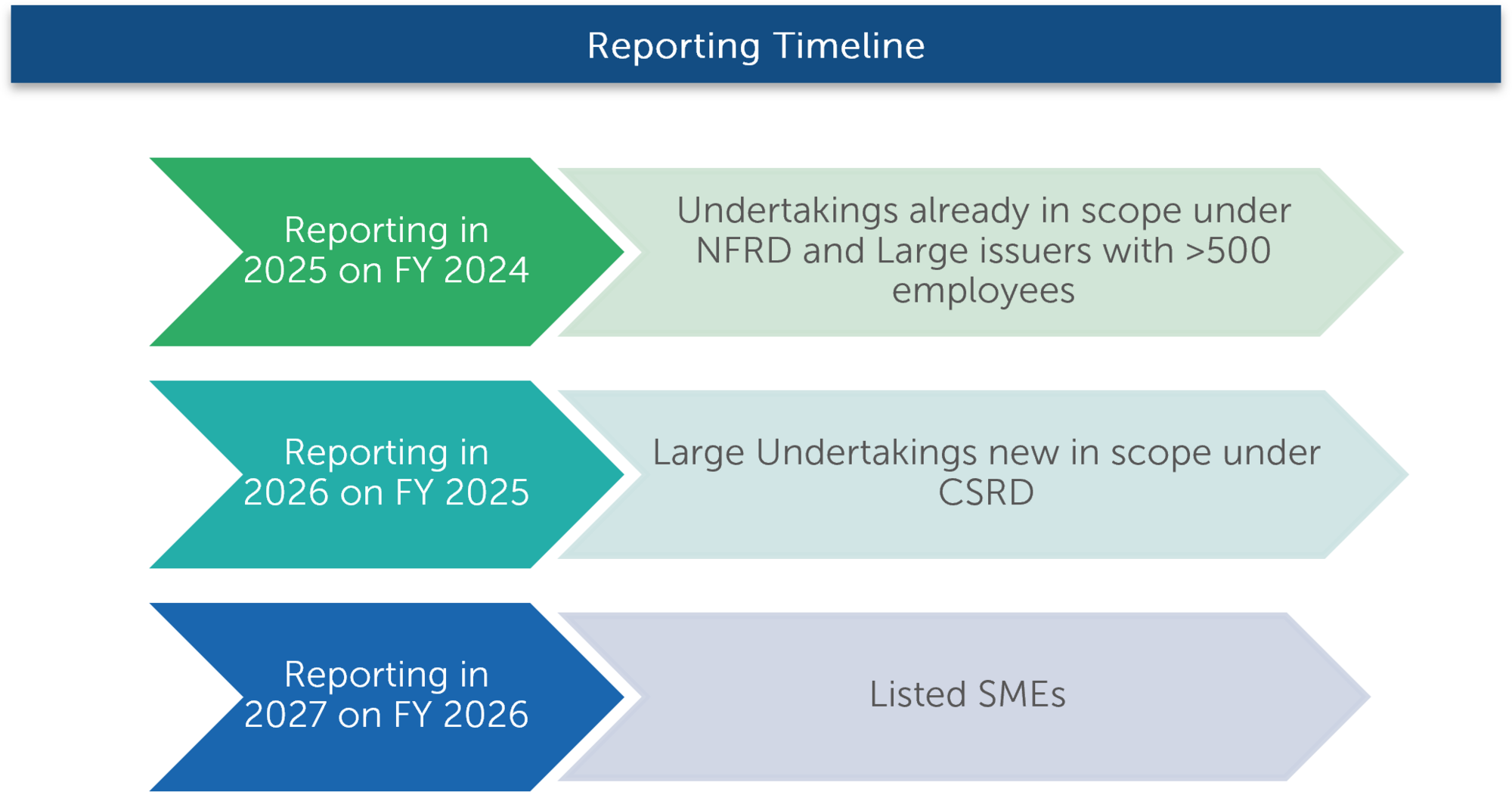

The Roadmap below highlights key milestones in the CSRD workplan:

Key Features

- Finalyse offers extensive experience and expertise in area of sustainability and climate related reporting for financial institutions.

- Ensure compliance with the CSRD recommendations setout by ESRS.

- Benefit from Finalyse’s unique approach, tailored to the specific needs and circumstances of each financial institution.

Frans is an actuary and Financial Risk Manager with international experience in the pensions and insurance sectors. He has been specialising in actuarial valuations (AXIS), financial and regulatory reporting (IAS19, US GAAP, IFRS2, IFRS17), regulatory reporting (IORP II, Solvency II, ICS, BMA), market risk management (ALM, SAA), climate change risk management and investment consulting.