Related Articles

How Finalyse can help

Climate change risk management for insurers

Climate change is expected to pose a serious risk for (re)insurers and society in the future. Without intervention, global average temperatures are expected to keep rising, along with the associated physical risks. This could increase (re)insurers' underwriting risk, challenge business strategies and negatively impact asset values. Regulators worldwide have made significant progress in providing guidance to (re)insurers on how to take account of climate change risk.

EIOPA expects (re)insurers to integrate climate change risk in their governance, risk management framework and ORSA and to perform climate change scenario analysis over the short and long term. (Re)insurers are expected to perform materiality assessments on a broad range of climate risks and analyse scenarios relevant to their portfolio. EIOPA will begin to monitor the application of their ORSA Opinion from April 2023.

The BMA similarly expects (re)insurers to address climate change risk in their governance, risk management framework and GSSA/CISSA. BMA will begin to monitor progress on the guidance during 2023, and the framework should be fully adopted by year-end 2025. BMA expects an implementation status update and at least a climate risk exposure analysis in the year-end 2022 ORSA, with continuous advancements in scenario analysis up to 2025.

How does Finalyse address your challenges?

Governance:

Integration of climate change risks in the ORSA, governance and risk management systems.

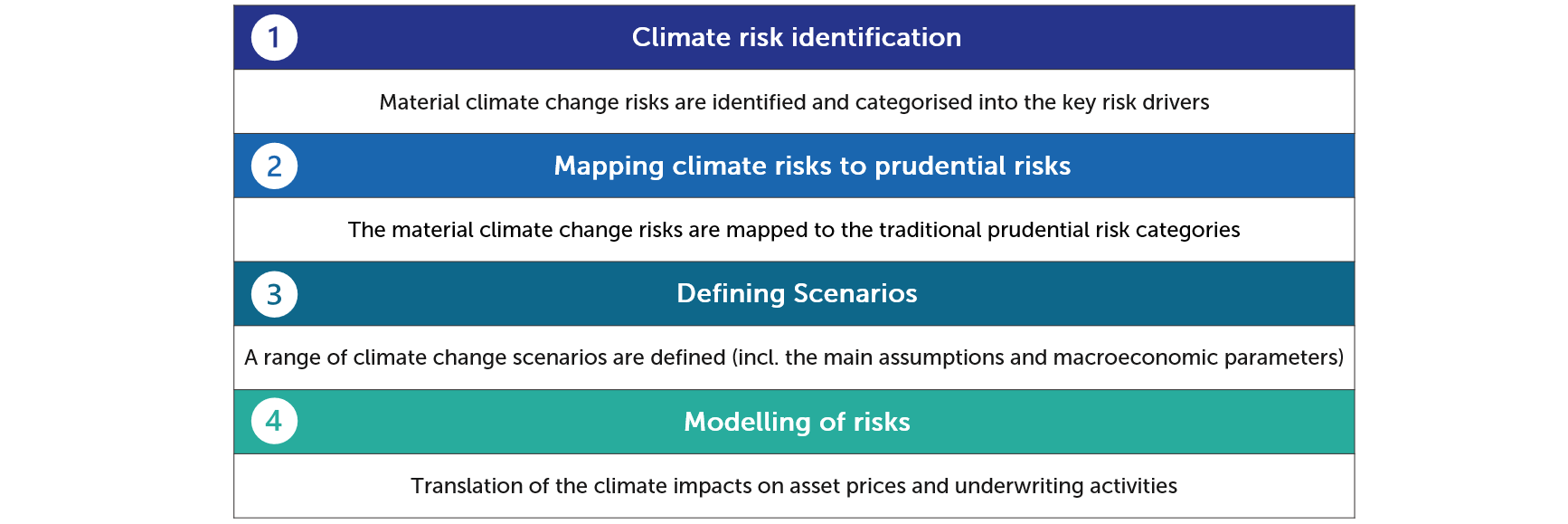

Risk identification:

Identification of a range of climate change risk exposures and materiality assessment of your portfolio.

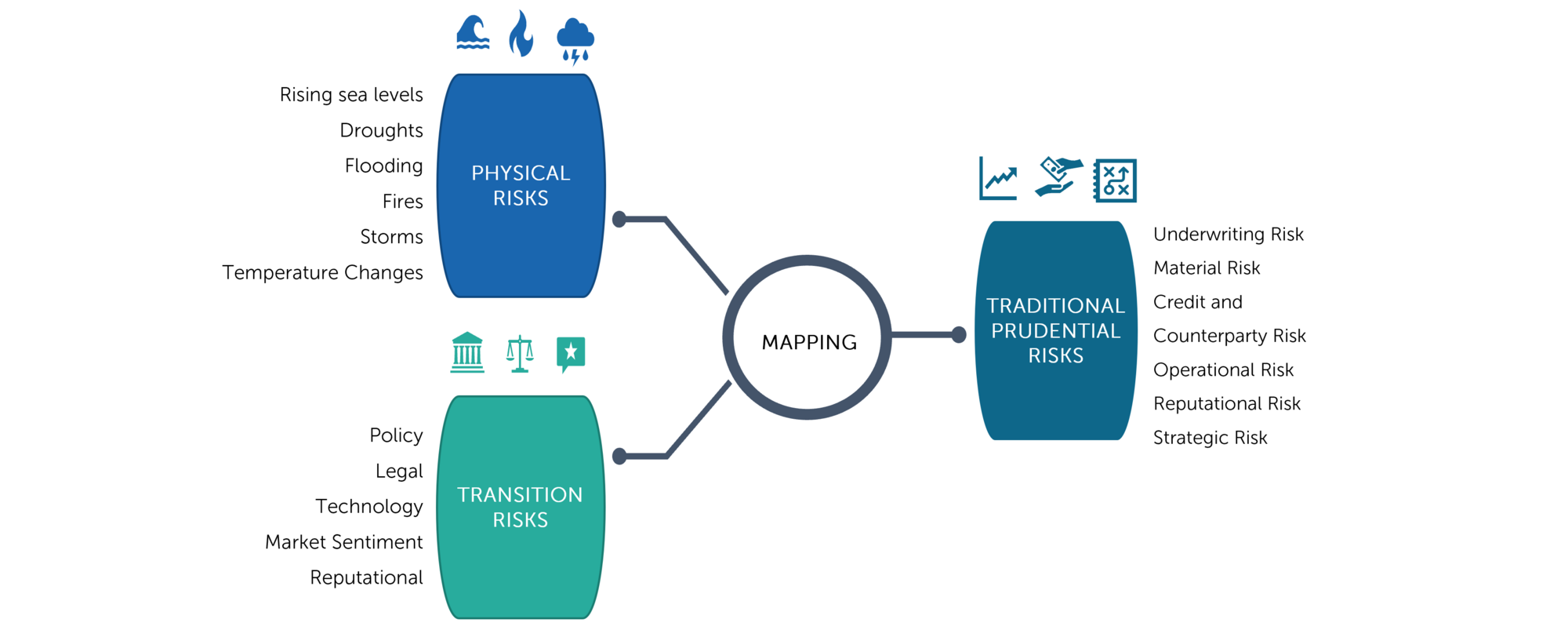

Mapping of risks:

Mapping the identified climate change risks to traditional prudential risk categories for (re)insurers.

Scenario definition:

Defining relevant climate scenarios for ORSA, leveraging online resources referenced by EIOPA (e.g. NGFS and IPCC).

Modelling of risks:

Modelling the risks for your scenarios, translating the climate projections into financial and underwriting impacts.

ORSA approach:

Defining modelling approach for ORSA scenarios, e.g. balance sheet stress tests versus projections over short or long term.

How does it work in practice?

Risk management framework for climate change risk:

Mapping of climate change risks:

Key Features

- Benefit from Finalyse’s extensive experience and expertise in the area of risk management for insurers.

- Development of a risk management framework that integrates climate change risk in your governance, risk-management system and ORSA.

- Support in complying with the ever increasing regulatory burden and alignment with the market practice.

Frans is an actuary and Financial Risk Manager with international experience in the pensions and insurance sectors. He has been specialising in actuarial valuations (AXIS), financial and regulatory reporting (IAS19, US GAAP, IFRS2, IFRS17), regulatory reporting (IORP II, Solvency II, ICS, BMA), market risk management (ALM, SAA), climate change risk management and investment consulting.

Client Cases

Integration of Climate Change Risk in the ORSA and Risk Management Framework

Finalyse supported the client with integrating climate change risk in their ORSA and risk management framework. This included performing a materiality assessment and setting a baseline scenario narrative, with the following key deliverables:

- Assessing the As-Is situation by investigating the progress made with regards to climate change risk management.

- Hosting a series of training sessions for the risk management and sustainability teams at each step of the project.

- Developing a framework for climate change risk management allowing the client to revisit and update the materiality assessments and scenarios in future.

- Development and support with the execution of the risk identification and climate risk mapping processes.

- Performing a materiality assessment for identified risks and documenting the justifications.

- Providing support with defining climate change scenarios to be used in the ORSA projections.

- Providing market insights and benchmarking on climate change risk ORSA treatments, as well as providing insights from our dealings with EIOPA and local regulators.

- Documentation of key decisions and updating relevant policies and procedures.

Following our successful project with the cleint in 2023 to integrate climate change risk into the risk management framework, Finalyse is currently supporting them on a further project to expand on and enhance the approach.

- Setting a strategy for enhancing the climate change risk management approach, for management approval.

- Developing a roadmap to implement the newly-defined strategy.

- Defining a climate change risk appetite with metrics, targets and limits, and building this into the Risk Appetite Statement.

- Establishing a process for the regular monitoring and reporting of the metrics, to ensure exposures are within the risk appetite and for management information.

Finalyse was engaged by Belfius Insurance, a Belgian insurer selling both life and non-life contracts nationally, to perform a review of their approach to climate change risk assessment. The assessment included the following steps:

- Performing a gap analysis versus the EIOPA and National Bank Belgium guidance.

- Proposing a roadmap to enhance the existing approach, along with suggested external data and tools that would be suitable for analysing the portfolio.

- Presenting the findings of the gap analysis and the suggested enhancements to senior management.

Finalyse supported the cleint in Belgium with their ESG disclosures for the Key Information Documents of some of their insurance products.

Finalyse assessed the information that was provided by the client in their Key Information Documents for their unit-linked life insurance products in light of the SFDR (Sustainable Financial Disclosures Regulation). This involved labelling the assets underlying these products into “light-green” funds, “dark green” funds and those that do not fall into either of these categories.

Finalyse supported the client with the regulatory requirements in terms of incorporating climate change risk. The project involved the following:

- Presentation of key climate change regulatory requirements from EIOPA and BMA to the management committee.

- Preparation of a roadmap for achieving compliance with these regulations.

- Hosting a training session for the group risk management team.