Francis is a Principal Consultant in charge of our insurance practice in Dublin. He has 15 years of experience within the life and non-life (re)insurance industry. His expertise covers the areas of financial reporting, prudential regulation, and actuarial modelling. Francis has worked in both industry and consulting with extensive exposure to Solvency II and BMA-regulated clients and a keen eye on new regulatory developments.

Divyank is a Senior Consultant with more than 8 years of experience and a part qualified Actuary. He has acquired expertise in Solvency II, IFRS17 and MCEV reporting and has worked for life and non-life business. He has extensive experience in Prophet modelling, DCS, statutory valuation and IFRS17 implementation and his coding skills include Prophet and DCS modelling, SAS, VBA, R.

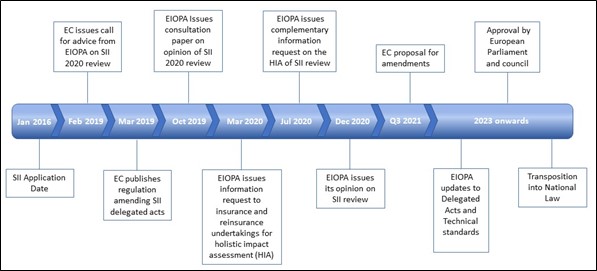

The European commission (EC) published a comprehensive review of the Solvency II (SII) Directive (The Directive) on 22 September 2021. This was based on the extensive work conducted by the EIOPA to provide its opinion on SII by the end of the year 2020 (see reference for Finalyse article as requested by the EC earlier in year 2019.

The EC has provided the proposed text of the Directive to the European Parliament and to the Council for their consideration and approval. It is expected that the approval will be made in 2023 and once this is done, the Member states must transpose it into National law within 18 months. Updates to the Delegated Acts and Implementing Technical Standards are foreseen to be applicable in the coming months.

The timeline below gives details of each milestone.

Outlined below are the changes proposed by the EC. We address in detail several key topics - long-term guarantee measures of estimating risk margin, volatility adjustment, solvency capital requirement under the interest rate risk sub-module and extrapolation of the risk-free yield curve.

The risk margin under the SII standard formula approach represents the cost of transfer of insurance obligations to a potential purchaser. It is calculated using a cost of capital approach. The EC has proposed an exponential time-dependent factor λ (lambda) to be applied to the risk margin formula, in respect of the SCR amount for year t. Below are the two-formula showing the calculation of risk margin under the current and proposed approach.

The intended application of lambda, with a value between 0 and 1, is to allow for a reduction in the impact of risks that are more distant in time. EIOPA concluded that a calibration of lambda equal to 0.975 provides a significant reduction in volatility and effectively addresses the issues identified by EIOPA. However, the EC is yet to finalise the value for this parameter. Using a simplified example of a life insurance business with a duration of 10 years and SCR of €100m at time 0, the implementation of the proposed new formula above would result in a risk margin reduction of c.€15m (approximately 20% of reduction where the cost of capital rate equals 6%).

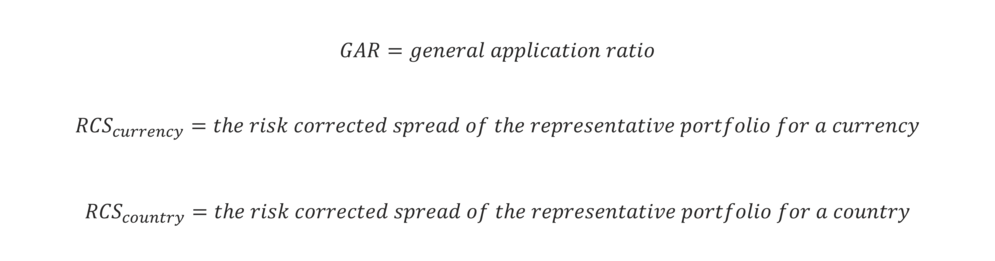

The volatility adjustment (VA) is an adjustment applied to the risk-free interest rate in the best estimate liability (BEL) calculation to reduce the impact of short-term bond spread volatility on the solvency position. It is calculated for all insurance and reinsurance eligible obligations of a currency and can be adjusted for country considerations under stressed conditions.

The formula under the current approach is:

The VA is calculated by applying a GAR of 65% on the risk corrected spread (RCS) which is based on a representative portfolio specific to a currency. Additionally, an adjustment including country-specific RCS is added under stressed conditions only if that RCS is greater than 100 bps.

As part of the SII 2020 review, there were potential deficiencies identified in the design of the VA. These include: the dampening effect of the VA being significantly higher or lower than the loss on assets, the cliff-edge effect when a country specific VA is triggered, and the failure to adequately allow for the illiquidity characteristics of the liability. The EC has proposed changes in the Directive to address some of these deficiencies and avoid any contravention of the existing VA objectives i.e., prevention of pro-cyclical behavior and mitigating the impact of bond spreads on own funds.

The proposal includes the removal of a condition that triggers country specific VA and introduces a smoothed increase in the VA via an addition to the permanent component in crisis situations.

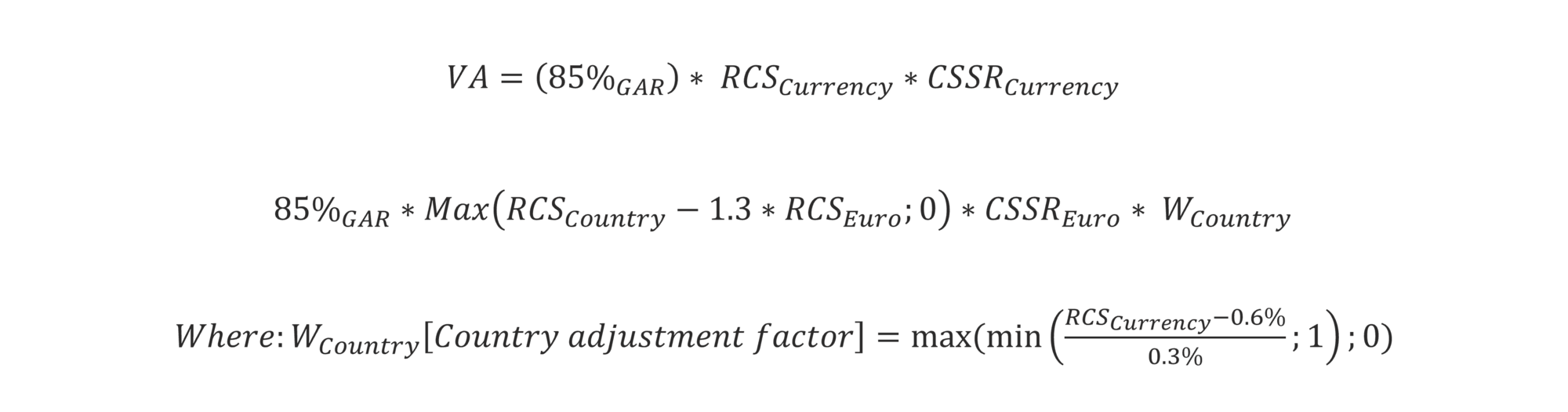

The proposed formula for the calculation of the VA is as follows:

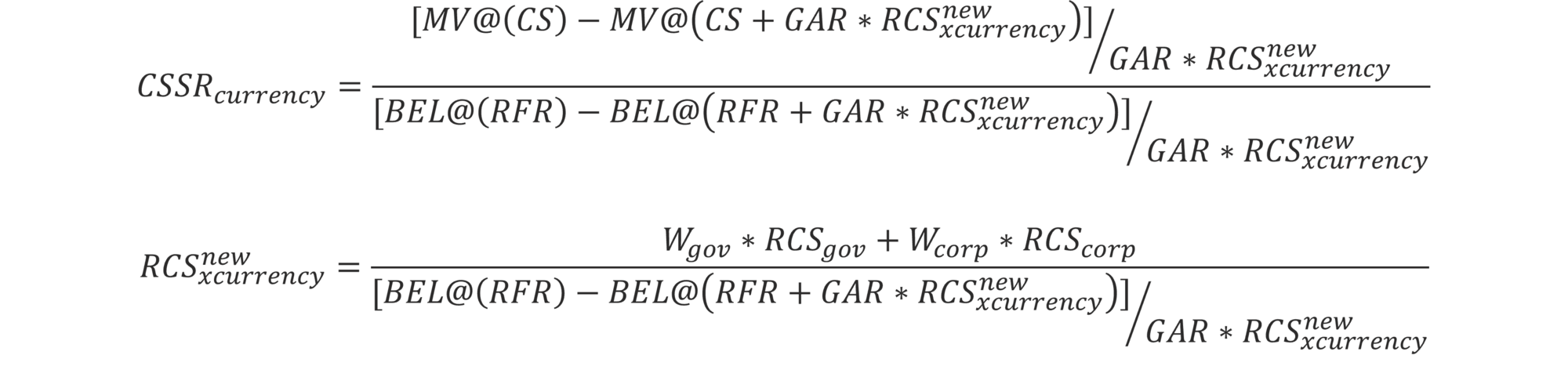

To address the issue of the movement in liability values overshooting movement in asset prices due to the application of VA, the EC has proposed a credit spread sensitivity ratio (CSSR) to be included in the calculation of VA (formula provided in the appendix). The estimation of this would be entity specific.

The CSSR can be defined as the sensitivity of assets of an insurance entity to changes in credit spreads, divided by the sensitivity of technical provisions (TP) to changes in the interest rate. This would help to reduce the basis risk with respect to EU representative portfolios, leading to a more accurate matching of spreads after VA adjustment. In addition, GAR has also been changed from 65% to 85% to capture unexpected credit and other risks.

The impact of the above amendments will depend on a company’s specific risk profile. Those entities that are in most need of the VA due to their circumstances will stand to benefit the most, while those companies that already have a well-matched asset-liability portfolio would see minimal gains. The average VA is expected to increase from 7 to 14 basis points at the EEA level.

Several issues were identified that led to under-estimation of the interest rate risk under the SII standard formula approach. These included, inter alia, actual interest rate movements being stronger than those assumed by stresses in the regulation already in place, negative interest rates not being stressed and deviation in the measurement of interest rate risk by internal model users. The concluding remarks of the impact assessment, in the SII 2020 review, state that the capital requirements are not sufficient for this material risk.

Thus, the EIOPA recommended a method that introduces new parameters to assess interest rate risk within the standard formula, along with a new formula for calculating the stressed rates. The previous formula had solely a relative shock component. The new formula includes an additive shock in addition to a relative shock, with a new set of parameters which has been calibrated to the last liquid point (LLP) of 20 years and the additive shock component. The EC has not yet provided details of the formula as these are covered by Level 2 texts. The formulas for the stressed interest rates for the calculation of interest rate risk are provided in the appendix.

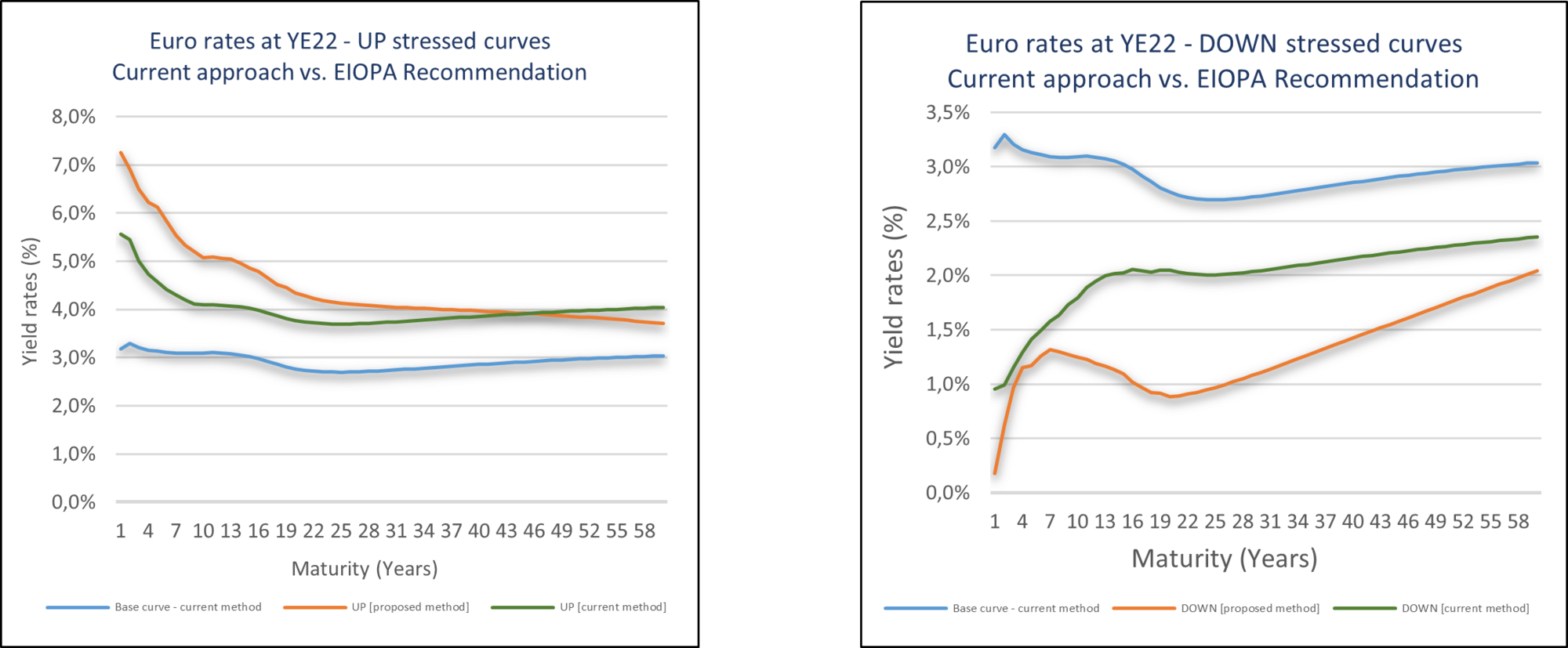

Additionally, the recommended formula ensures that the minimum shock of 1% is removed in the rising interest rate scenario and that negative interest rates are stressed in the falling rate scenario. The below graphs show a comparison of the base, current stressed and proposed stressed curves in the up and down interest rate scenario (as at Year End (YE) 2022).

The graphs illustrate a clear shift in the stressed interest rate curve when moving to the proposed method. If the Up shock is biting, the pre-diversified interest rate shock could double at earlier durations. If the Down shock is biting, this will lead to a doubling of the undiversified shock at nearly all durations. These changes are expected to increase capital requirements, particularly for entities with long-term liabilities and an asset portfolio with a significantly shorter duration than that of their liabilities. For example, a book of business with BEL at time 0 of around negative €500m, the pre-diversified SCR for interest rate risk would nearly double from €23m to €45m in the Up scenario and €21m to €39m in the down scenario.

A gradual implementation process is recommended to be grandfathered for the new definition of the downward interest rate shock that should not last longer than 5 years of time.

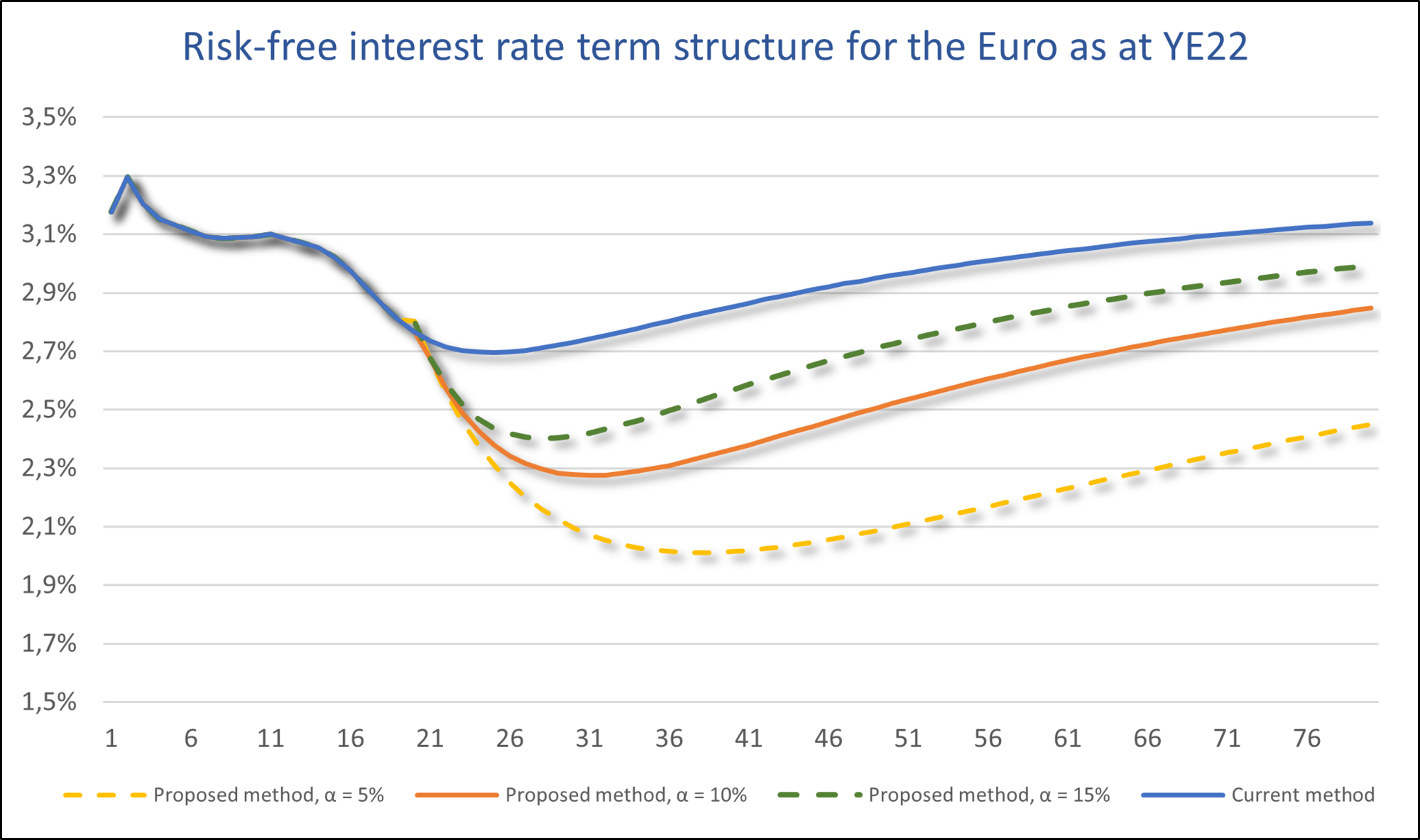

The EC has proposed to change Smith-Wilson method of extrapolating rates from the LLP, to converge to an Ultimate Forward Rate (UFR). For Euro-denominated zones, the LLP is determined to be 20 years and the convergence to the UFR happens over 40 years after the LLP.

The SII 2020 review of the extrapolation method or the risk-free yield curve indicated that the current setting of LLP implicitly impacts the interest rates beyond 20 years, which has ultimately led to under-estimation of the TPs. In addition, the deviation of the extrapolated rates from the actual market rates is a contributing factor to volatility of TPs and risk management incentives. The proposed changes to LLP are in conjunction with the convergence speed to the UFR.

There is no stipulated convergence period to the UFR with the recommended convergence factor set at 10%. The following graph shows the impact of using different convergence factors and a comparison of the current and proposed methods of extrapolating yield curve as at YE 2022.

As evident from the graph above, the proposed methodology would lead to lower interest rates and an increase in TPs for long term liabilities (durations greater than 20 years). This is aimed to enhance policyholder protection and promote good risk management, as TPs will now be closer to achieving market consistency. It is worth noting that the impact will only be seen beyond the LLP (this is 20 years for euro-denominated zones) and so the biggest impact will mainly, for example, be for annuity providers.

The Directive mentions phasing in of the method until year end 2031, gradually. The parameters shall be decreased linearly at the beginning of each calendar year until final parameters of extrapolation are applied as of 01 Jan 2032.

Other Pillar 1 amendments proposed by the EC are set out below. Some of these are not yet specified in the proposal by the EC and are covered in the implementing regulations:

The Pillar 2 changes proposed by the draft Directive include:

Amendments to Pillar 3 topics relate to reporting and disclosure requirements. Proposed changes include modifications to the structure of the Solvency Financial Condition Report (SFCR) and an external audit requirement for the balance sheet disclosed as part of the same, as well as a requirement for most insurance companies to submit pre-emptive recovery plans. Under the proposed approach, the deadline for submission of the solo SFCR will be extended from 14 weeks after YE to 18 weeks. The group SFCR deadline would also be extended by 4 weeks – from 20 to 24 weeks after YE.

The EC has proposed changes in the Directive, after careful analysis of the impact assessment provided by the EIOPA. The changes, related to Pillar 1, 2 and 3, were selected for proposal by the EC from several options that were recommended as part of the SII 2020 review.

The impact of the change in the estimation of risk margin for insurers will likely be material for most insurers. Changes proposed for the calculation of VA seems quite significant which needs to be implemented by insurers that are allowed to apply a VA. And the impact of the change in the methodology for extrapolation of the risk-free yield curve is likely to concern insurers with books of longer duration i.e., with considerable liabilities after 20 years for Euro.

The EIOPA carried out impact assessment, for most of the amendments proposed, where certain amendments, such as for risk margin is expected to let the own funds increase, while others such as for interest rate stresses, are expected to increase the SCR.

The proposed Directive intends to make the SII framework more aligned to the economic outlook and addresses the inadequacies identified. Finalyse has extensive experience in Actuarial and Risk management for insurance companies and can help you make sense of the proposals under the draft Directive including:

Proposed credit spread sensitivity ratio (CSSR) formula:

Formula for the calculation of credit spread sensitivity ratio (CSSR) used for calculating volatility adjustment under the proposed approach.

Proposed Interest rate stresses formula:

Formula for estimating interest rate curves for up and down scenario for calculating SCR interest rate under the proposed approach:

Where for different maturities m (in years):

r(m) = risk-free rate at maturity m

rup(m) = rate at maturity m in rising interest rate scenario

rdown(m) = rate at maturity m in declining interest rate scenario

s vector value is linearly interpolated between 20 and 90 years.

b vector value is zero beyond 60 years and is linearly interpolated between 20 and 60 years.

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support