Reviewed by Francis Furey, Principal Consultant.

The Insurance Capital Standard (ICS) is a consolidated group-wide capital standard for Internationally Active Insurance Groups (IAIGs). It is being developed by the International Association of Insurance Supervisors (IAIS) and their main objective is to establish a common regulatory framework that achieves comparable outcomes across jurisdictions. The ICS will provide a common language for supervisory discussions of IAIG solvency and enhance global convergence among group capital standards.

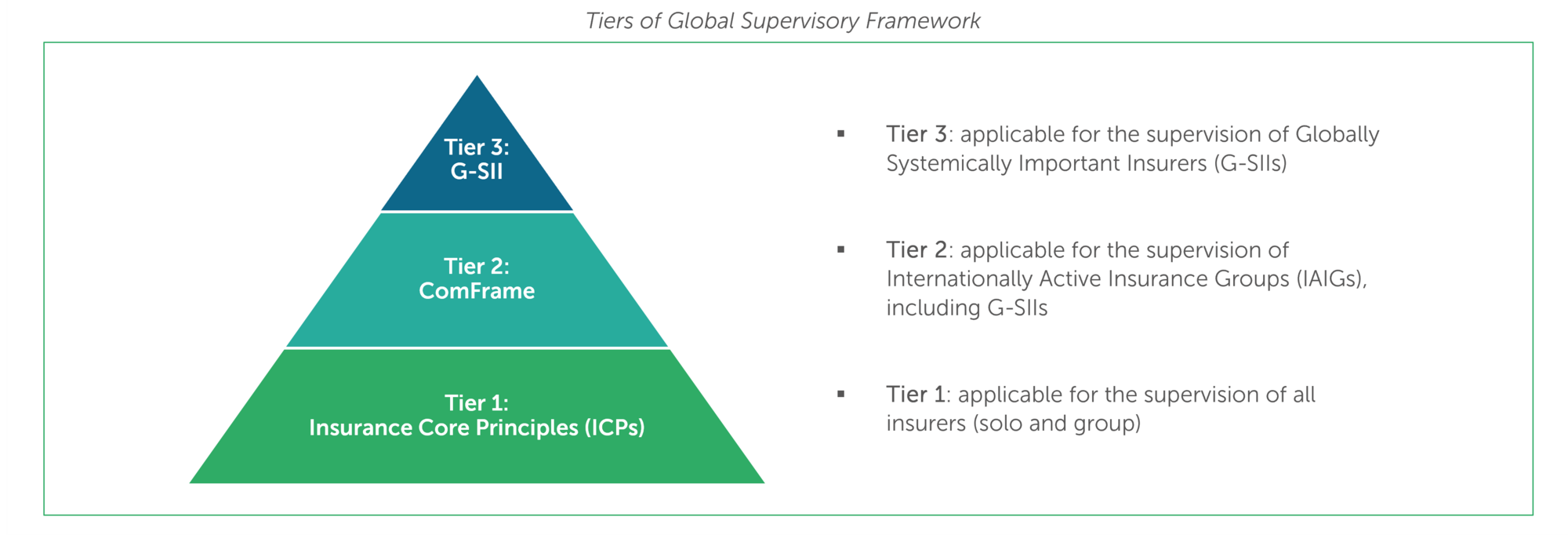

The IAIS has developed a set of principles, standards, and other supporting material for the supervision of the insurance sector. This global supervisory framework is based on a three-tiered approach. Tier 1 consists of the Insurance Core Principles (ICPs). The ICPs seek to encourage the maintenance of consistently high supervisory standards in IAIS member jurisdictions. ICP14 (Valuation) and ICP17 (Capital) relate to ICS. The Common Framework for the Supervision of IAIGs (ComFrame) consists of quantitative and qualitative supervisory requirements. The ICS will be one of the quantitative components of ComFrame.

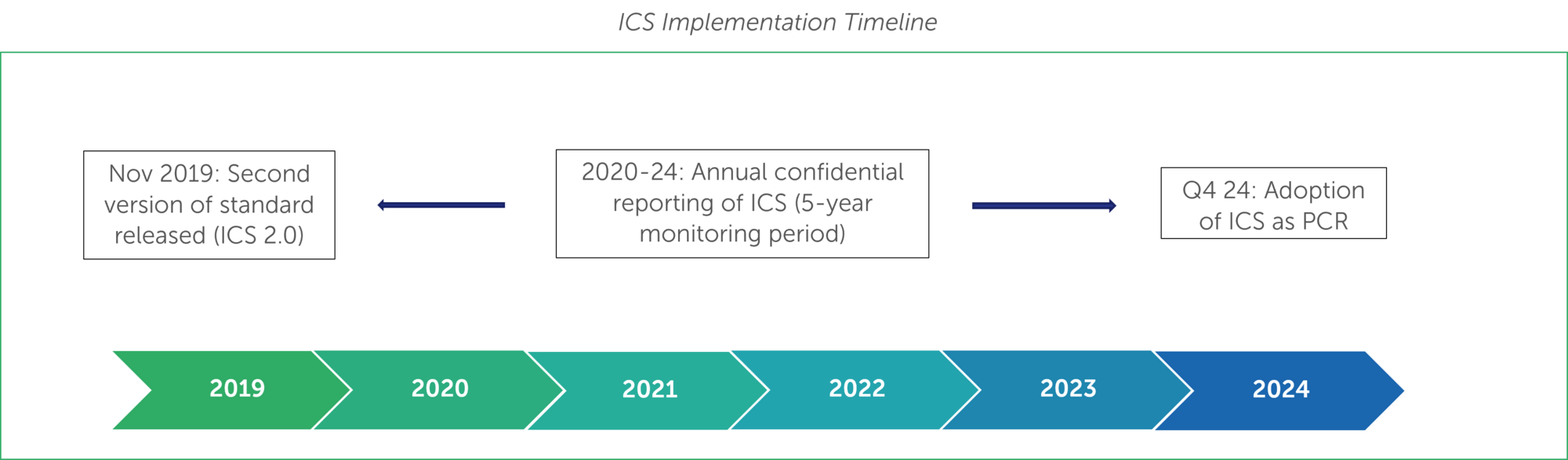

The ICS roll-out is currently in the 4th year of its 5-year monitoring period. The timeline below highlights key milestones in the IAIS’ workplan over this period. Following the end of the monitoring period in Q4 2024, the intention is for ICS to be implemented as a group-wide prescribed capital requirement.

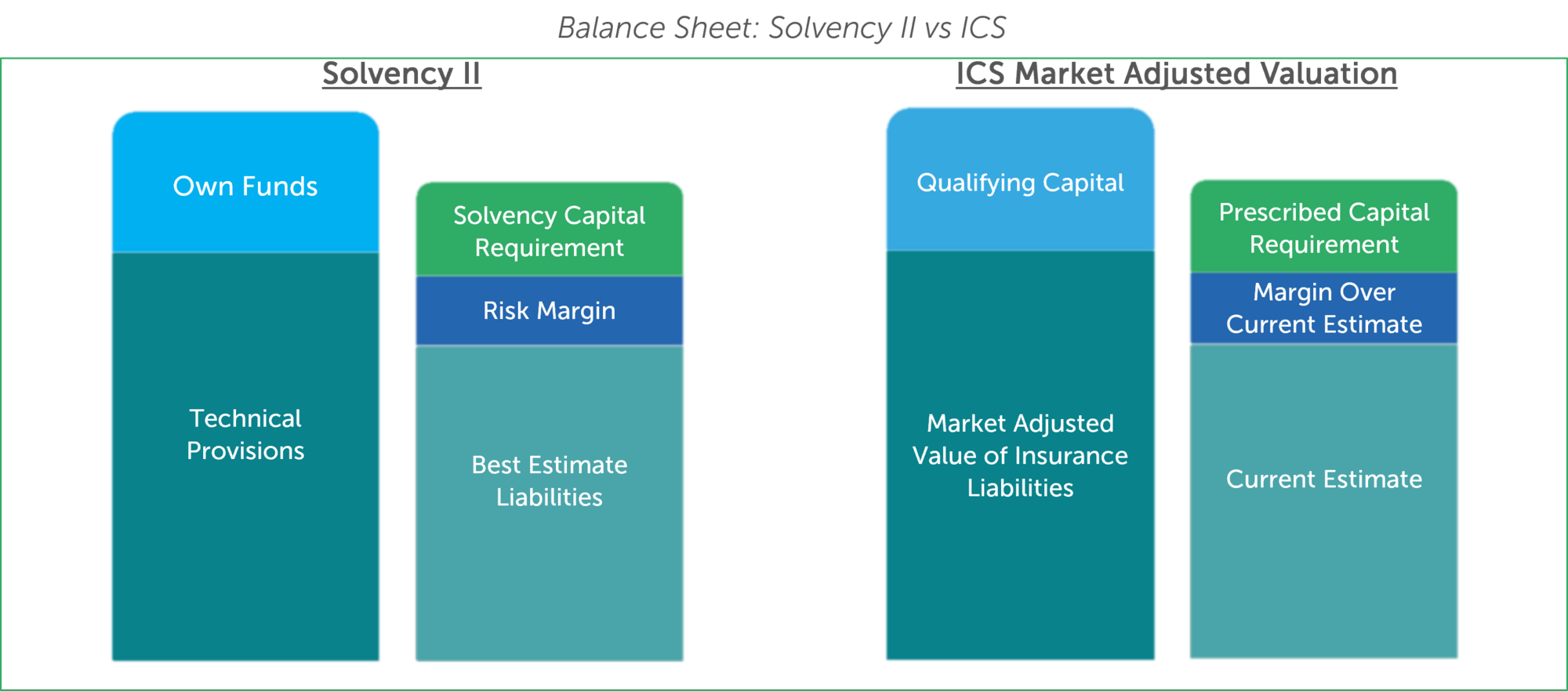

ICS consists of 3 technical components: market adjusted valuation, qualifying capital resources and a standard method for the ICS capital requirement. The building blocks of the ICS market adjusted valuation are comparable to those in the Solvency II balance sheet. This is illustrated at a high level below.

MAV insurance liabilities are the sum of the current estimate (CE) and a margin over the current estimate (MOCE). The CE is equal to the probability-weighted average of the present values of the future cash-flows associated with insurance liabilities, discounted using an adjusted yield curve.

The adjusted yield curve is based on:

The adjustment to the yield curve is determined using the “Three-Bucket Approach”. This classifies liabilities into the Top Bucket, the Middle Bucket, and the General Bucket, depending on the nature of the liabilities and the assets backing these liabilities.

The MOCE is a margin added to the current estimate, which covers the inherent uncertainty in the cash flows related to insurance obligations.

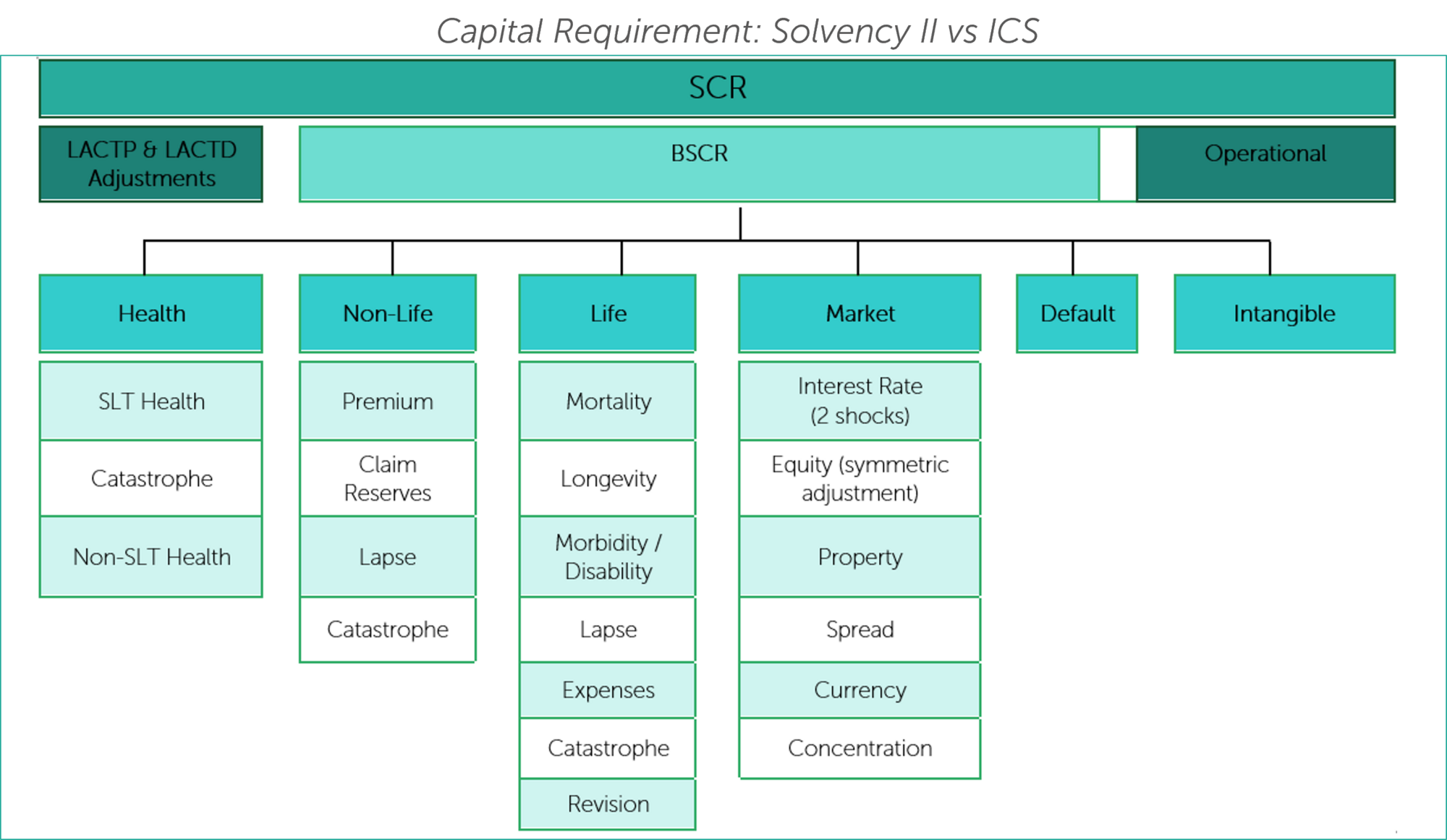

The ICS capital requirement is based on the potential adverse change in the IAIG’s qualifying capital resources resulting from unexpected changes of specified risks. The target criterion is a 99.5% Value at Risk (VaR) measure over a one-year time horizon. The reference ICS coverage ratio is calculated as:

ICS Ratio = Qualifying capital resources / ICS capital requirement

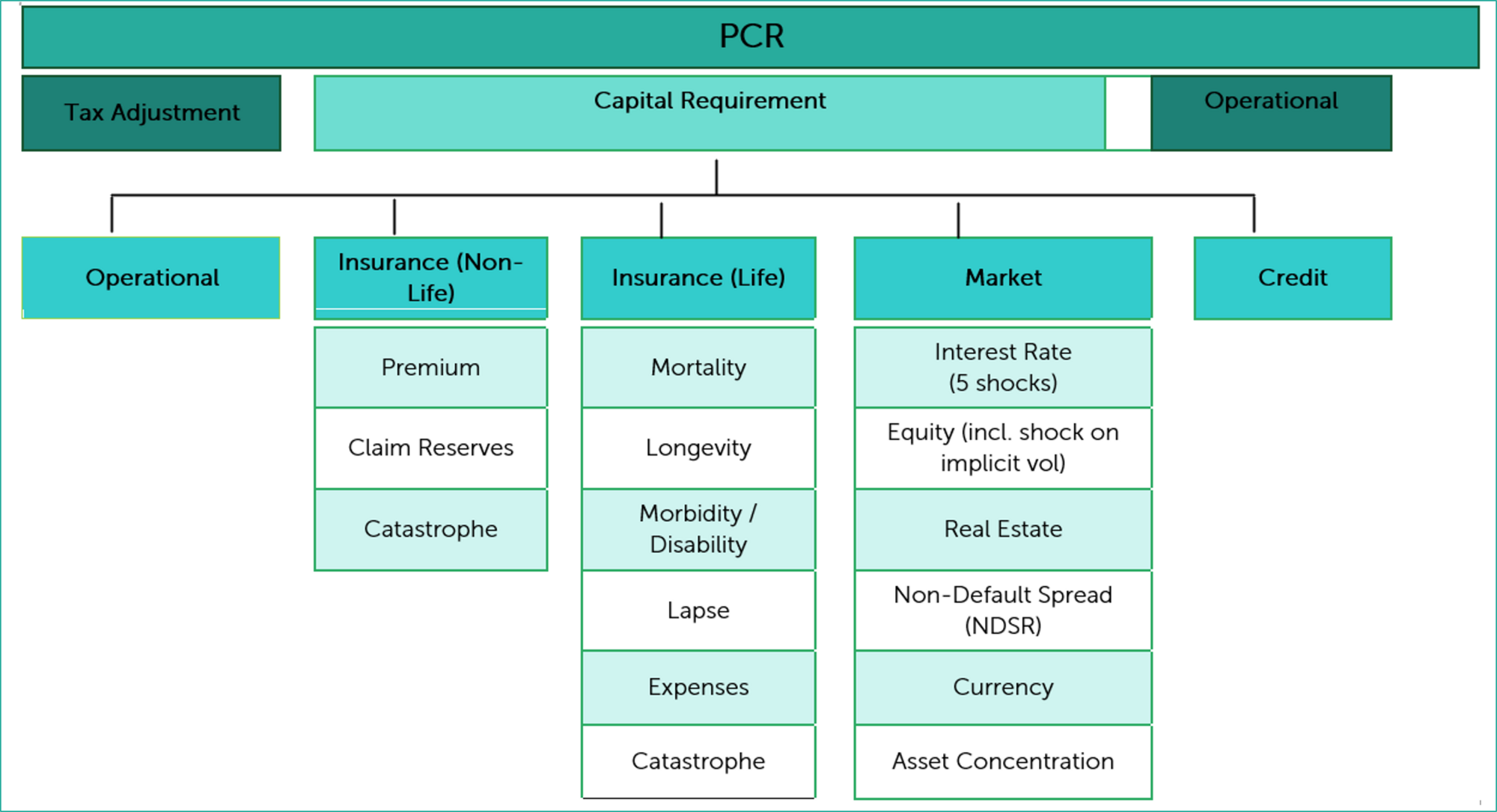

The categories of risk included in the standard method are:

Risks are measured using two approaches: a stress approach and a factor-based approach. The Prescribed Capital Requirement (PCR) under ICS is similar in many ways to the Solvency Capital Requirement under Solvency II, in respect of its calculations and its categorisation of risks.

The individual risk charges are combined in a way that recognises risk diversification, using correlation matrices. For the life insurance segment, geographical segmentation is used to calculate the risk charge. This means that the stress factor applied will vary by region. Most of the prescribed stress factors are more stringent under the Solvency II regime. For example, the SII mortality shock is +15% compared to +12.5% for the EEA region under ICS. The ICS risk map does not include a Health module. This risk is implicitly allowed for in the premium and claim reserve risk segments of the non-life module.

The interest rate risk charge is notable in that it is based on a combination of five stresses, as opposed to two stresses under Solvency II (interest rate up and interest rate down). The five stresses for the ICS interest rate risk charge are as follows:

The equity risk charge is calculated as the change in net asset value following the occurrence of a stress scenario that impacts the level and volatility of the fair value of equities. Thanks to a larger number of asset classes and shock scenarios, ICS will estimate more precisely the capital requirements for companies. This precision will in theory imply a lower market PCR compared to its SCR equivalent.

During the five-year ICS monitoring period (2020-2024) the IAIS has annually collected and analysed confidential data from volunteer insurance groups, with the objective of finalising ICS for implementation as a prescribed capital requirement by year-end 2024. IAIS recently undertook its latest public consultation on the ICS, named ‘Candidate ICS as a PCR’. This consultation brings the IAIS one step closer to achieving its target implementation date.

IAIGs based in USA are developing an Aggregation Method which, if deemed comparable, will be considered an outcome-equivalent approach for implementation of the ICS as a PCR.

In Europe, EIOPA has publicly stated its commitment to the ICS development. In their view, “the candidate ICS as a PCR goes in the right direction of implementing sound risk-based supervisory frameworks globally and is consistent with the main features of Solvency II.” For example, internal models are now acknowledged as part of the ICS, allowing the recognition of specificities in the risk profiles of large, sophisticated groups. In these last stages of development of the ICS, EIOPA remains fully engaged and calls on all EU stakeholders to engage as well.

We have outlined above the similarities between the ICS and Solvency II regulatory frameworks. This raises the question whether SII can gain ICS equivalence at some stage in the future. However, in the short term, IAIGs will need to find optimal and innovative ways to incorporate the ICS calibration into their current operating environment.

ICS reporting support:

BAU implementation:

For more information on this subject, please have a look at our article published earlier this year titled “Insurance Capital Standard: A Closer Look” which is available to download here.

Alternatively, you can contact one of our experienced consultants at insurance@finalyse.com who would be happy to help with all of your ICS needs.

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support