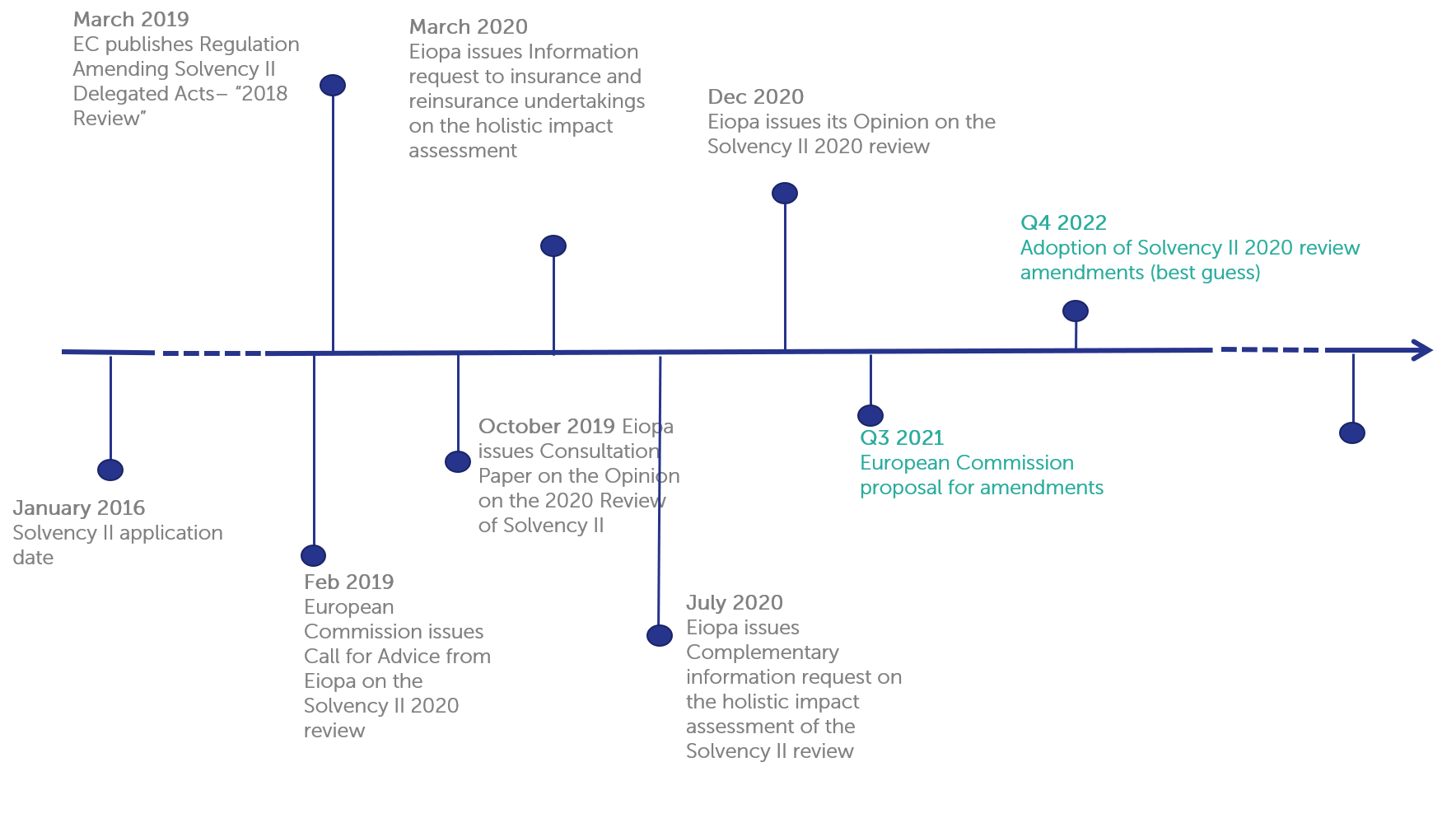

On February 2019, the European Commission (EC) requested EIOPA to provide, by the end of 2020, technical advice on the full review of Solvency II rules (EIOPA 2020 review).

The implementation of the proposed changes is expected to happen around the end of 2025.

Finalyse has produced a more extensive white paper which focuses on the following aspects of EIOPA’s proposals:

Over the next couple of weeks Finalyse plans to issue several smaller blog posts on the material changes proposed by EIOPA. The first topic we have picked concerns the volatility adjustment.

If you wish to receive a copy of this paper, please contact francis.furey@finalyse.com

There are several design concerns namely:

Over or undershooting effect of the VA

The dampening effect of the VA may exceed the effect of a loss in the market value of fixed-income assets. EIOPA has proposed that VA should be based on the undertakings’ portfolio rather than any reference portfolio and an application ratio should be applied to the adjustment which measures the duration and volume mismatch between fixed income investments and insurance liabilities of the undertaking.

Consideration of illiquidity characteristics of liabilities

EIOPA recommends the use of an illiquidity factor based on a “bucketing approach”, i.e., another application ratio should be introduced based on a categorisation of liabilities which captures the stability and predictability of cash-flows.

Underlying assumptions of VA are unclear.

The VA can be considered as a compensation for exaggerations in bond spreads or represent an additional illiquidity premium on assets that replicates the liabilities. EIOPA recommends that the VA should be split into a permanent VA reflecting the long-term illiquid nature of insurance cash flows and its implications on undertakings’ investments decisions; and a macro-economic VA that would only exist when spreads are wide during a financial crisis that affects the bond market.

Cliff effect of the country-specific increase, activation mechanism does not work as expected.

There can be a cliff-edge effect from the country VA during periods where spreads of a single Member State fluctuate around the trigger point of the country specific VA with activation and deactivation of the country specific VA leading to volatility in Own funds. EIOPA proposes that the macro-economic VA should be based on an improvement of the current country-specific increase of the VA to mitigate cliff-edge effects and improve the activation mechanism.

Misestimation of risk correction of VA

Several potential problems with this risk-correction have been identified:

Currently, the VA is calculated as a fixed percentage of a spread. EIOPA recommends that this should be based on a percentage of the spread which should be differentiated with respect to issuers, namely between sovereign exposure of EEA countries (‘government bonds’, 30%) and other bonds (‘corporate bonds’, 50%).

Overall, EIOPA recommends that all these components of the proposal should not be considered in isolation but jointly form an enhanced and more targeted design of the VA.

The level of GAR should not be set too high that it leads to under-reserving of TPs or too low that it fails to serve its main purpose to prevent the pro-cyclical behaviour on financial markets and mitigate the effect of exaggerations of bond spreads. EIOPA has therefore considered whether the current GAR factor should be changed, and if yes by which amount.

EIOPA states that some risks and uncertainties will remain even in the improved design, so the general application ratio still needs to be significantly below 100%. Therefore, it advises to increase the GAR from 65% to 85%.

All the above changes will also ensure that all risks contained in the spread are captured, whilst ensuring that VA is still effective as a countercyclical measure.

The average VA increases from 7 basis points to 14 basis points at EEA level.

Finalyse has extensive experience in risk management for insurance companies and can help you make sense of the EIOPA proposals:

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support