Comprehensive yet pragmatic solutions for your major challenges

IFRS 17 methodology, configuration, and results

Under IFRS 9 the insurers will be obliged to calculate the ECL on their portfolios. We have both the experience and eagerness to rise up to this challenge.

Set functional risk limits which are consistent with your overall risk appetite.

Written by

Brice-Etienne Toure-Tiglinatienin, Consultant

Jessica Ukendi, Consultant

Yannis Pitaras, Principal Consultant

The IFRS 17 Insurance Contracts standard was issued in 2017 and initially, it was supposed to come into effect for annual reports beginning on or after 1st January 2021. It replaces the interim Standard IFRS 4 Insurance Contracts. The standard aims at increasing transparency and comparability of financial information reported by insurance companies as it introduces a consistent accounting model for all insurance contracts based on a current measurement approach.

On the 25th June 2020, the International Accounting Standard Board (IASB) published several amendments to IFRS 17. These amendments address many of the concerns raised by the industry and aim at facilitating the implementation of IFRS17, without deviating from its underlying principles.

The amendments have three main purposes:

IFRS 17 was initially planned to be effective as from 1st January 2021 with the possibility of an early application. The exemption from applying IFRS 9 was supposed to coincide with this date. The Board finally decided to defer the effective date by 2 years to allow enough time for the adoption and the implementation of the amended IFRS 17 by the jurisdictions around the world so that the reports have the same effective date for all the jurisdictions. Therefore, the first IFRS 17 reports are now expected for annual reporting periods starting on or after 1st January 2023. The exemption from applying IFRS 9 has concurrently been extended by two years. Insurers still have the possibility to adopt IFRS 17 early if they also apply IFRS 9.

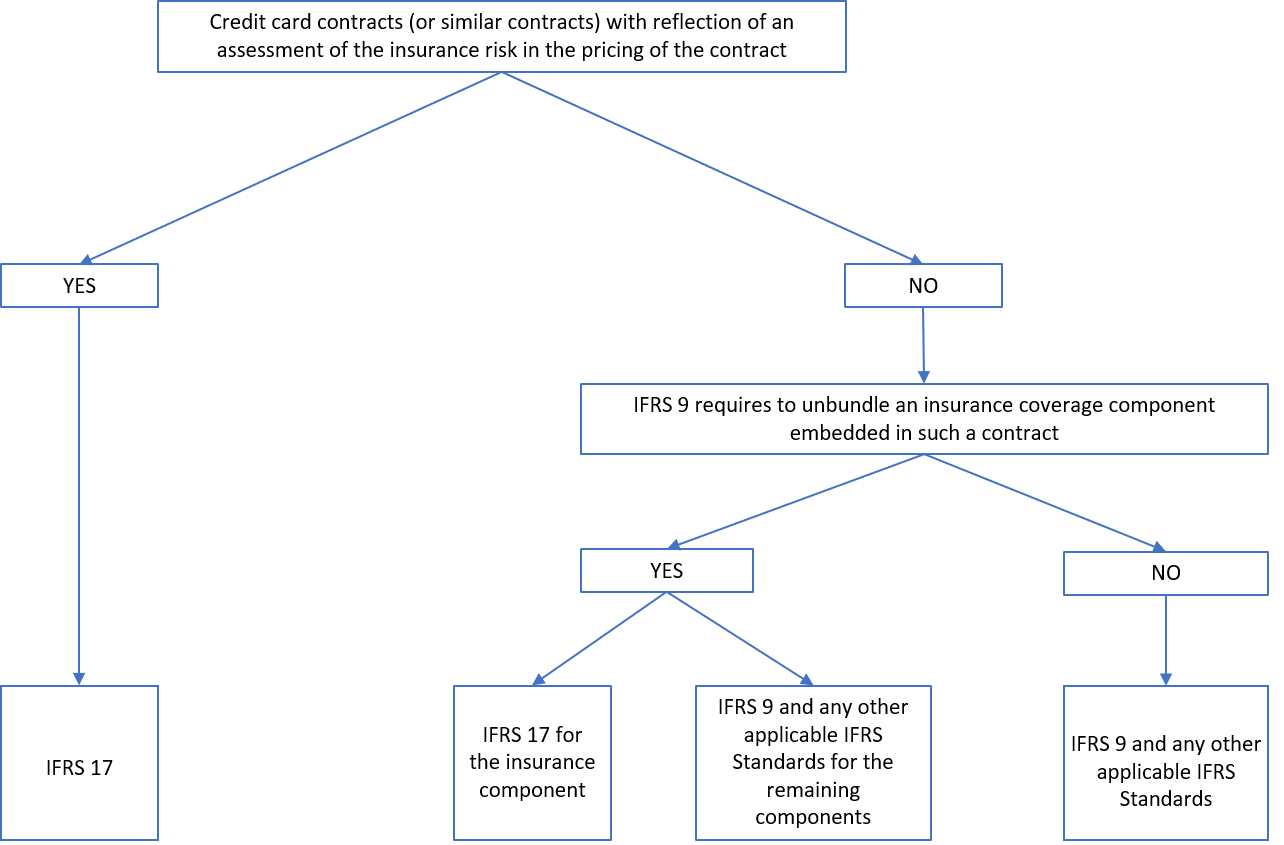

Some credit card contracts are now excluded from the scope of IFRS 17 subject to certain criteria. For instance, contracts (and similar contracts) for which there is no insurance risk in setting the price associated with an individual customer, are now excluded from the IFRS 17 Standard scope. However, if IFRS 9 requires unbundling of the insurance coverage provided as part of the contractual terms of the credit card, then the company has to separate the insurance component and apply IFRS 17 to that lone component. IFRS 9 and any other applicable IFRS Standards are applicable to the remaining credit card components.

The Board has also added an optional exclusion of loans that transfer significant insurance risk (loans with death waivers, for example) for which a company is permitted to apply either IFRS 17 or IFRS 9.

This amendment is expected to reduce implementation costs as it will allow insurers to apply IFRS 9 instead of IFRS 17 to some loans, credit cards and similar contracts.

For onerous contracts at initial recognition, IFRS 17 requires a company to recognise immediately losses in profit or loss. It was originally specified that any recoveries of those losses from reinsurance contracts held had to be recognised over time as the company receives reinsurance coverage. The amended IFRS 17 requires a simultaneous initial recognition of losses on onerous contracts and expected recoveries of those losses from all reinsurance contracts held at the time of entry or before entry to those onerous contracts. With this amendment, net cost or net gain from purchasing a reinsurance contract held will be recognised immediately hence reducing any accounting mismatch that could arise from the immediate recognition of losses on the insurance contract. The amendment applies to all types of reinsurance contracts (proportional and non-proportional reinsurance).

This amendment is likely to simplify the explanation of the accounting of reinsurance contracts held to investors.

Prior to the amendments, IFRS17 required from insurance companies to present, recognise and measure insurance contracts at the level of insurance groups.

The amendment to paragraph 78 of IFRS 17 now requires an entity to separately present assets and liabilities in the carrying amounts at the level of portfolios of insurance contracts issued and of reinsurance contracts held. In other words, the amendment changes the level of aggregation for presentation purposes in the statement of financial position from group level to portfolio level.

This amendment is expected to lead to a reduction of implementation costs and of the number of insurance contracts carrying amounts presented on the balance sheet.

IFRS 17 initially required to fully and immediately allocate the directly attributable acquisition costs to a group of contracts, even when part of these costs was related to expected contracts renewals that were to be recognised in the future. The IFRS 17 amendment now requires the allocation of a part of these costs to related expected contracts renewals. This portion of acquisition costs paid will be continuously recognised as an asset until expected renewals of those initial insurance contracts are recognised in the future.

As a result of this amendment, assets for insurance acquisition cash flows will be of a longer duration and of a larger amount. In exchange, an impairment test will be performed, and an additional disclosure will be required for these assets.

This amendment is expected to ease the understanding of the results by preventing the presentation of some insurance contracts as loss-making because of the excess of acquisition costs over the premium of the initial contract, while renewals are expected.

Originally, the IFRS 17 required that the profit (CSM) in the BBA approach (insurance contracts without direct participation features) is recognised over time as the company provides an insurance coverage. IFRS 17 Amendments instead require to recognise profit as the entity provides insurance coverage or any investment-return service.

The amendment is expected to make the results easier to explain as it changes the pattern of profit recognition to better align it with the provision of different services by the company.

Initially, IFRS 17 only allowed insurers to apply the risk mitigation option to insurance contracts with direct participation feature (variable fee approach (VFA)) when using derivatives to mitigate financial risk. The amendment enables a company to also apply the risk mitigation option when mitigating financial risks using reinsurance contracts held or non-derivative financial instruments measured at fair value through profit or loss (PVPL).

This amendment is expected to reduce accounting mismatches and make it easier to explain the accounting for insurance contracts to investors.

Prior to the amendments, a company did not have the possibility to change the estimates (such as fulfilment of cash flows related to future service, CSM) made in previous interim reports, in subsequent interim reports and in the annual report. The IFRS 17 Amendments now give insurers the option to change the estimates made in previous interim reports when applying IFRS 17 subsequently. Insurers are required to apply their choice of accounting policy consistently to all insurance contracts issued and all reinsurance contracts held.

This amendment is expected to give to entities subject to interim financial statements the choice of applying the less costly option.

IFRS 17 Amendments also contain transition reliefs for the application of the modified retrospective approach and the fair value approach relating to loss recoveries in reinsurance contracts held, recognition of assets in insurance acquisition cash flows paid, effects of previous interim reports, investment contracts with discretionary participation features, contracts acquired in their settlement period, the date of application and the use of the fair value approach for the risk mitigation option, all at the transition date.

IFRS 17 Amendments address a lot of concerns and implementation challenges raised by the insurance market. Notably, they provide some flexibility and cost reduction to ease the implementation without fundamental changes to the IFRS 17 itself. In our view, the most important amendments are the recovery of losses through reinsurance held contracts, the allocation of acquisition costs to expected contract renewals and the use of the risk mitigation option as they enable insurer to disclose information based on the current measurement and avoid accounting mismatches. However, a part of the industry was notably calling for annual cohorts not to be used for contracts in the variable fee approach with significant mutualisation and for all contracts at transition, at a minimum. However, the Board considered the risk of loss of information as too great and confirmed its decision to keep annual cohorts.

Companies will now focus on the implementation and testing (including dry runs) of the amended IFRS 17 Insurance Contracts. They will have one period of adjusted comparative IFRS 17 information starting on 1 January 2022 before the effective date beginning on 1 January 2023.

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support