Related Articles

How Finalyse can help

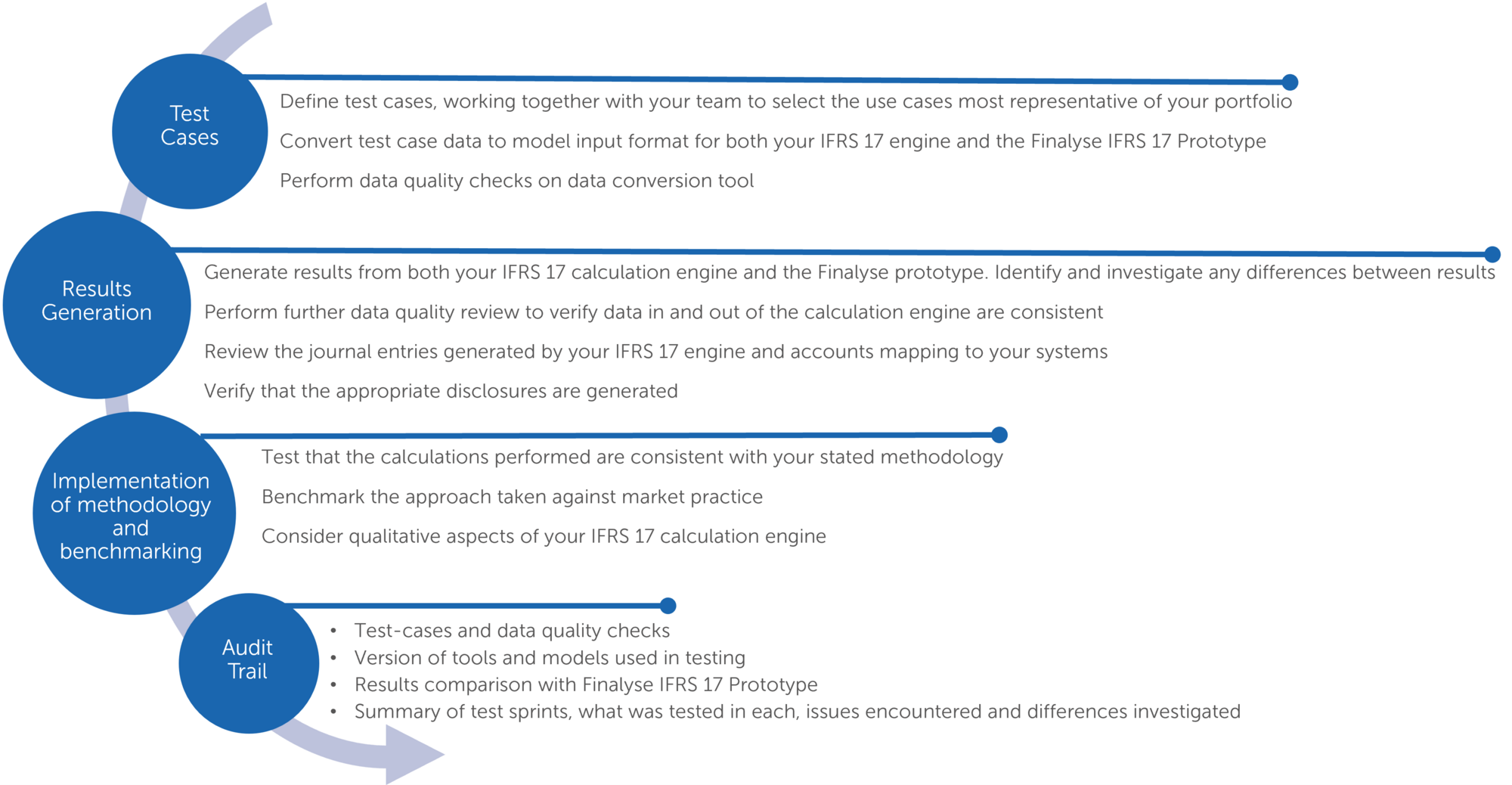

IFRS 17 Validation

IFRS 17 will be effective from 1 January 2023 and it will change the recognition, measurement, presentation and disclosure of insurance contracts. It directly impacts how insurers value their insurance liabilities and recognise profits.

Insurers must define methodologies for non-prescribed items such as discount rate, risk adjustment, contract boundaries. New systems must be developed to handle data, perform calculations and generate accounting ledger entries.

How does Finalyse address your challenges?

Validation of your entire IFRS 17 landscape.

Including methodology, configuration and output from accounting engine (cashflows, journal entries and disclosures) which helps provide assurance and identify any gaps in your process.

Our in-house IFRS 17 Toolkit includes:

- CSM Actuarial Prototype

- CSM Generator

- New business generator

- BS Generator

- P&L Generator

- Risk adjustment prototype

- Pre-defined use cases for validation

Independent model validation review.

Setting key design principles, assessing implementation of the methodology, data, assumptions and documenting results.

Assistance in performing your parallel runs and reconciliations with the current IFRS 4 and with the solvency balance sheet

Technical and process recommendations and benchmarking will allow you to refine your approach ahead of transition

Audit Trail with clear documentation of our independent validation process which can be used as support for external audit and future reviews

Key Features

- The introduction of the IFRS 17 standard will bring increased scrutiny from external audit and management. Independent validation from Finalyse provides assurance and will give you a view of how your approach compares to market practice.

- Our experience in model implementation, testing and configuration allows us to have an efficient approach to validation. This approach includes an established testing method, pre-defined use cases, our in-house IFRS 17 Toolkit, pre-defined validation policy and process.

- Working with Finalyse, you will gain insights into the key profit drivers under IFRS 17 and support in developing your Management Information and KPIs under the new standard.

- Finalyse has a business acumen in areas beyond financial reporting, such as actuarial models, IT systems (data management and storage capacities), risk management (ALM and hedging, product design) business strategies and remuneration.

Frans is an actuary and Financial Risk Manager with international experience in the pensions and insurance sectors. He has been specialising in actuarial valuations (AXIS), financial and regulatory reporting (IAS19, US GAAP, IFRS2, IFRS17), regulatory reporting (IORP II, Solvency II, ICS, BMA), market risk management (ALM, SAA), climate change risk management and investment consulting.

Divyank is a Senior Consultant with more than 8 years of experience and a part qualified Actuary. He has acquired expertise in Solvency II, IFRS17 and MCEV reporting and has worked for life and non-life business. He has extensive experience in Prophet modelling, DCS, statutory valuation and IFRS17 implementation and his coding skills include Prophet and DCS modelling, SAS, VBA, R.