Related Articles

How Finalyse can help

IFRS 17 implementation

IFRS 17 will apply as from 1 January 2023. Depending on which stage of the IFRS 17 implementation process you are, Finalyse can help you with the gap analysis, the proof of concept, the development of the right tools and processes to meet the target operating model, your impact analysis, the parallel runs and the go-live launch.

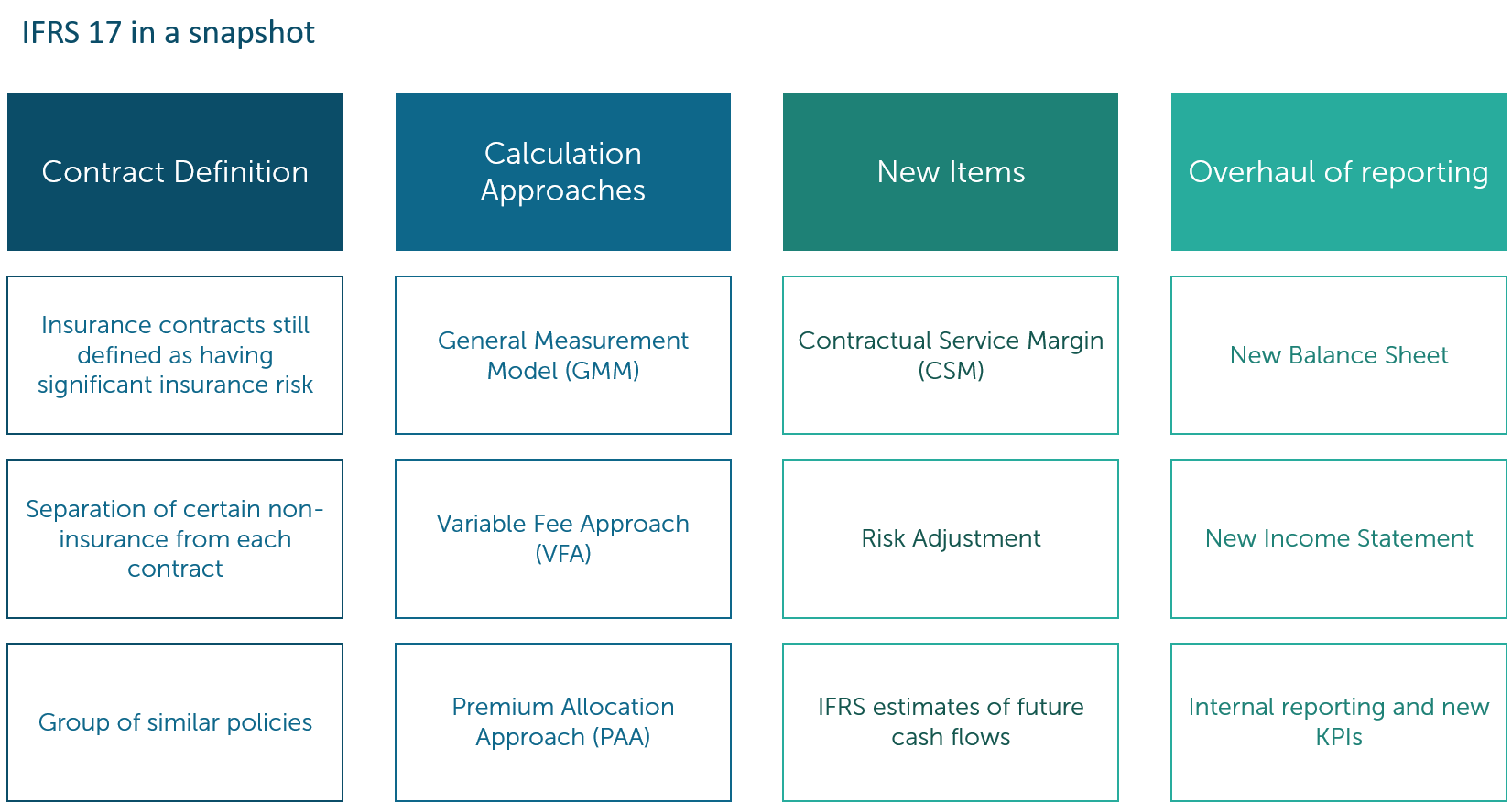

The new accounting standard changes the recognition, measurement, presentation and disclosure of insurance contracts. It directly impacts how insurers value their insurance liabilities on their balance sheet and how they recognise profits in their Income Statement.

How does Finalyse address your challenges?

We define business, functional, and technical requirements

We facilitate coordination between functions such as Finance, Actuarial and IT in the process of accounting systems upgrading

We design and test use cases, and deploy parallel and dry runs

We help insurers select the right risk mitigation techniques and ALM strategies to reduce IFRS 17’s Income Statement and Balance Sheet volatility

We help you select your target operating model / IT tool

We offer parallel implementation of IFRS 17 and IFRS 9

How does it work in practice?

We have a team of IFRS 17 subject matter experts, including actuaries, and a dedicated competency centre with significant hands-on experience in the development and implementation of target operating models for all aspects of financial reporting, including the integration of actuarial and accounting processes as well as the data management and quality processes.

Key Features

- Leverage on our experience in areas beyond financial reporting, such as actuarial models, IT systems including data management and storage capacities, risk management including ALM and hedging, product design, business strategies and remuneration.

- IFRS 17 is a principle-based standard, and as such, it is subject to interpretation in several areas. Additionally, it provides for a number of options to be selected by insurers from day one. It is, therefore, important that combinations of options and approaches are tested against carefully defined insurance and economic scenarios before taking any final decisions.

- With the temporary exemption from IFRS 9 for insurers, you can bring the two standards into line and apply them together as from January 2023. Finalyse offers its experience in the parallel implementation of both standards.

Divyank is a Senior Consultant with more than 8 years of experience and a part qualified Actuary. He has acquired expertise in Solvency II, IFRS17 and MCEV reporting and has worked for life and non-life business. He has extensive experience in Prophet modelling, DCS, statutory valuation and IFRS17 implementation and his coding skills include Prophet and DCS modelling, SAS, VBA, R.