Agile and comprehensive assessment, measurement and management of your market and liquidity risks

SAA optimisation based on your risk tolerance and specific business needs

Combining a technological and practical approach to deliver actuarial and risk modelling solutions

Insights from the Joint Committee Update on Risks and Vulnerabilities in the EU Financial System – Spring 2026 (JC 2026 06)

Sankesh Jain is a nearly qualified actuary with expertise in actuarial reporting and actuarial model modernization within life insurance along with diverse experience in pensions, and regulatory reporting. He specializes in Solvency II and IFRS 17 modelling, reserving, and capital calculations. Skilled in tools such as Excel, VBA, SQL and Python, he supports actuarial valuations, stress testing, and risk reporting. His experience spans actuarial controls, governance, and pension advisory, supported by a strong academic background in quantitative finance and statistics.

European insurers enter 2026 from a position of strength. Solvency ratios remain robust, capital buffers are strong, and higher interest rates have bolstered investment income. However, the latest update from the Joint Committee of the European Supervisory Authorities (ESAs) suggests that this resilience may mask a more important development: the nature of risk is changing.

Rather than being driven primarily by cyclical market movements, the current risk environment is increasingly shaped by geopolitical uncertainty, structural interconnectedness, and the potential for non-linear shock propagation. This shift does not necessarily imply greater risk today—but it does mean that risks are becoming harder to anticipate, model, and manage using traditional approaches.

Geopolitical risk is now cited as the primary macroeconomic concern by 51.4% of respondents in the Joint Committee survey. While geopolitical events have always influenced financial markets, what is different today is the speed, scale, and simultaneity with which these effects are transmitted across the system.

Recent geopolitical tensions have demonstrated how quickly shocks can feed into energy markets, inflation dynamics, and interest rate expectations. For insurers, this creates a dual impact. On the asset side, market volatility increases through movements in interest rates and credit spreads. On the liability side, inflation-sensitive lines—such as motor and property—experience rising claims costs.

From a modelling perspective, the challenge lies in the transmission mechanism. Geopolitical events do not affect solvency directly; they propagate through multiple financial variables simultaneously. This means geopolitical risk can no longer be treated as a qualitative overlay in ORSA. Instead, it must be translated into quantitative shocks across key risk drivers, including market, credit, and underwriting risk.

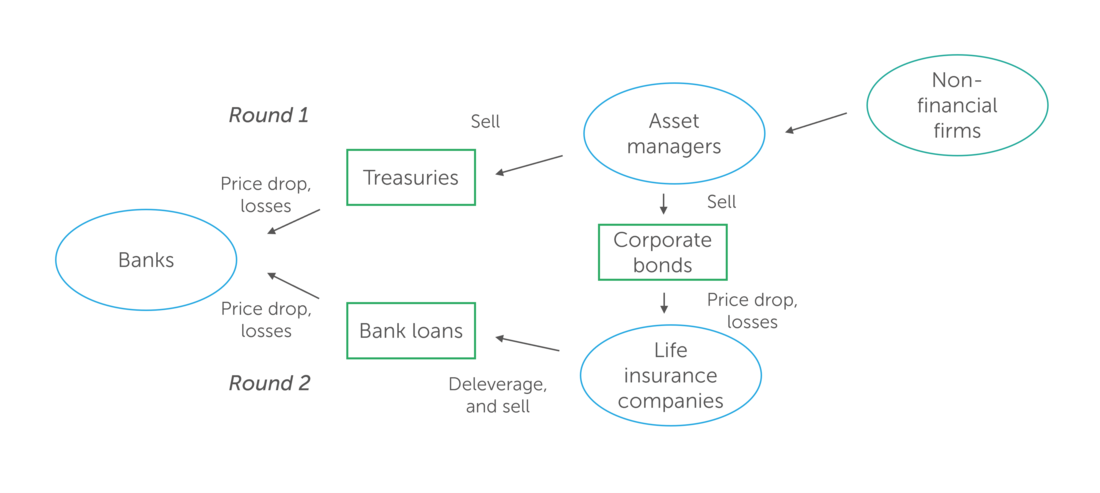

A second key theme emerging from the report is the increasing interconnectedness of financial markets. Insurers are no longer exposed solely to their own portfolios, but to a broader network that includes banks, asset managers, private markets, and global counterparties.

This has important implications for how stress events unfold. Rather than remaining contained within a single asset class or sector, shocks can propagate across the system through multiple channels. For example, liquidity stress in segments of the private credit market in 2023–2024 highlighted how redemption pressures and valuation uncertainty can spill over into broader markets.

For insurers, this means that risk is no longer additive, but increasingly multiplicative. Correlations between asset classes tend to increase during periods of stress, amplifying losses beyond what traditional models—often calibrated on stable historical relationships—would predict.

The growing allocation to private equity and private credit represents another important structural trend. These assets offer attractive yield and diversification benefits, but they also introduce distinct risk characteristics, including illiquidity, limited transparency, and valuation uncertainty.

A key challenge is that the apparent stability of private assets may be misleading. Because these assets are not priced continuously, changes in market conditions are often reflected with a lag. Evidence from recent market developments supports this: in 2023-2024, several large private credit and real estate funds in the US and UK imposed redemption limits due to liquidity pressures, highlighting the mismatch between asset liquidity and investor expectations.

For insurers, this raises a critical question: are current frameworks adequately capturing the economic risk of these exposures, or relying on accounting stability as a proxy for resilience?

Despite strong recent market performance, the Joint Committee notes that financial markets remain vulnerable to abrupt repricing. In particular, the report highlights the risk that even moderate shocks could trigger disproportionate corrections.

For insurers, this creates a “double impact” on solvency. A market shock reduces Own Funds through asset value declines, while at the same time increasing the Solvency Capital Requirement due to higher volatility and spread risk. This interaction can significantly amplify the impact on solvency positions.

The Joint Committee’s findings point to a clear conclusion: risk is not only evolving, but becoming more interconnected and system-driven. The key question for insurers is therefore not simply how to measure risk, but how to respond to it.

In practical terms, this requires several shifts in approach.

First, insurers should move towards integrated stress testing frameworks that capture the interaction between multiple risk drivers, rather than assessing risks in isolation.

Second, geopolitical risk should be translated into quantitative scenarios, ensuring that its impact is consistently reflected across market, credit, and underwriting risk modules.

Third, greater attention should be given to liquidity risk and valuation uncertainty, particularly in private market exposures, including the use of liquidity-adjusted stress scenarios.

Finally, insurers should strengthen forward-looking risk governance, combining model-based outputs with expert judgement to better capture emerging and non-linear risks.

The Spring 2026 Joint Committee update does not signal an immediate deterioration in financial stability. However, it does highlight a more fundamental shift: from a system characterised by stable and largely independent risks, to one where risks are increasingly interconnected, non-linear, and difficult to model.

For insurers, resilience remains important—but adaptability is becoming critical. The ability to translate emerging risks into actionable insights will be a key differentiator in navigating the evolving financial landscape.

At Finalyse, we continue to assist financial institutions and insurers in developing more integrated, forward-looking risk frameworks that are aligned with the realities of today’s risk environment.

If you would like to discuss how these developments may impact your organisation or explore how to enhance your risk framework, feel free to get in touch with your usual Finalyse contact.

Geopolitical risk has always influenced financial markets, but its impact has become more immediate and widespread. Recent developments show that geopolitical events now transmit rapidly into inflation, interest rates, and credit spreads, affecting both assets and liabilities simultaneously. This makes geopolitical risk a more direct driver of solvency and capital requirements than in the past.

Insurers should move beyond treating geopolitical risk as a qualitative overlay and instead translate it into quantitative stress scenarios. This includes modelling its impact across multiple risk drivers—such as market, credit, and underwriting risks—and assessing combined scenarios rather than isolated shocks. Integrating expert judgement alongside model outputs is also key to capturing non-linear effects.

Private market assets, such as private equity and private credit, introduce illiquidity, valuation uncertainty, and limited transparency. While they can enhance yield, their risks may not be fully visible in normal conditions due to infrequent pricing. Under stress, delayed valuation adjustments and limited exit options can amplify the impact on solvency, making liquidity risk management a critical consideration.

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support