The highest possible predictive power of your models

How confident are you that your risk models show what you need to see? Would your regulator agree?

Expertise, guidance, and peace of mind through every step of your ICAAP and ILAAP journey

The European Central Bank (ECB) will conduct a 2026 geopolitical reverse stress test on 110 directly supervised banks, evaluating how shocks (e.g., conflicts, sanctions) could cause severe capital/liquidity failure. Unlike traditional tests, the reverse approach starts from a predefined outcome (300 basis point depletion in CET1) and works backward to determine the scenarios and transmission channels that could lead to such a result.

This article aims to examine geopolitical risk in the current context through three main lenses: its role as a cross-cutting systemic shock for financial institutions; its gradual integration into the prudential supervisory framework; and the emergence of a new approach to shock analysis, one that places greater emphasis on the coherence and plausibility of scenarios rather than on the mere quantification of losses.

Russia’s annexation of Crimea in 2014 marked a significant turning point in Europe’s geopolitical landscape, as it called into question a security framework long based on principles such as territorial integrity and the peaceful settlement of disputes between European states.

In February 2022, Russia launched a large-scale military operation in Ukraine, which significantly expanded the scope of the conflict. Beyond its immediate political and security implications, the conflict has also been associated with economic repercussions leading to a surge in energy prices, disruptions in global agricultural markets, and a sharp acceleration of inflation across Europe. 1

However, war in Ukraine is only one element of a broader geopolitical environment characterized by several persistent areas of tension. In the Middle East, ongoing regional conflicts continue to affect political stability and occasionally disrupt strategic trade and energy routes. 2

At the same time, the strategic rivalry between China and the United States has led to persistent trade tensions, affecting global value chains, investment flows, and economic growth. 3

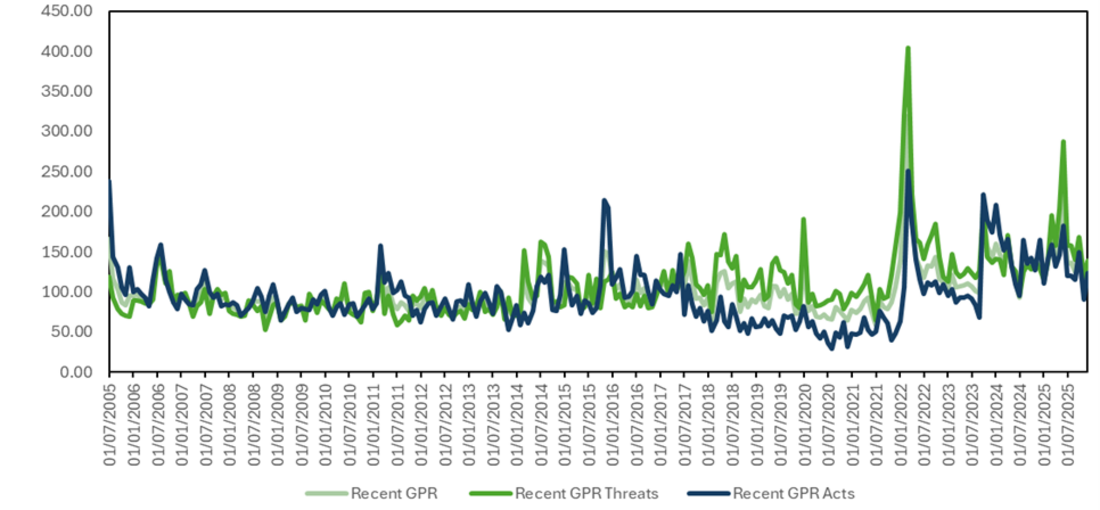

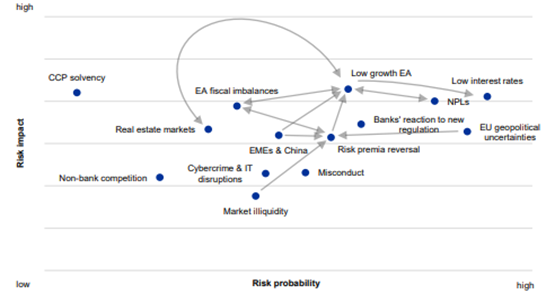

This accumulation of tensions is clearly reflected in the evolution of the Geopolitical Risk (GPR) Index 4, as shown in Figure 1 : The “threats” and “acts” components both point to a marked increase in geopolitical risk since the mid-2010s, with pronounced spikes during major international crises. This pattern suggests that geopolitical risk can no longer be viewed as a rare or purely exogenous shock, but rather as a structural feature of the global macro-financial environment.

For financial institutions, this has translated into increased volatility, credit deterioration, and a challenge to modelling frameworks built on assumptions of stability. It is in this context that the European Central Bank announced the implementation of a reverse stress test focused on geopolitical risk in 2026, aimed at assessing banks’ ability to identify and manage this risk.

In its communications, the European Central Bank relies 5 on the definition proposed by Dario Caldara and Matteo Iacoviello 6, according to which geopolitical risk refers to « the threat, realisation and escalation of adverse events associated with wars, terrorism and any tensions among states and political actors that affect the peaceful course of international relations.».

This broad definition implies that geopolitical risk does not constitute a standalone category in the traditional prudential sense, but rather a cross-cutting factor capable of simultaneously affecting all conventional banking risk categories.

The ECB explicitly highlights (see Figure 2) that geopolitical shocks propagate through multiple economic, financial, and operational channels, making them particularly difficult to capture within analytical frameworks based on linear and historically calibrated relationships (such as PD and LGD models).

Recent experience provides several concrete illustrations of these transmission mechanisms, and Russia’s invasion of Ukraine in February 2022 stands out as a textbook example in this regard. Given Europe’s heavy reliance on Russian gas imports, the conflict quickly led to major energy supply shocks. The successive shutdown of several strategic gas flows to Europe in 2022 7 resulted in a sudden and severe disruption to gas supply across the continent.

These supply disruptions translated into a sharp surge in energy prices, with gas prices rising by more than 160% over the course of 2022 and electricity prices increasing by around 125% in the euro area, according to aggregated data from Eurostat and the European Commission 10.

These energy shocks acted as a powerful macroeconomic transmission channel, quickly spreading beyond the energy sector to affect the broader real economy. Rising production costs fueled a general increase in the prices of goods and services, including industrial and agricultural commodities, contributing to a surge in euro area harmonized inflation to 10.6% in October 2022 8.

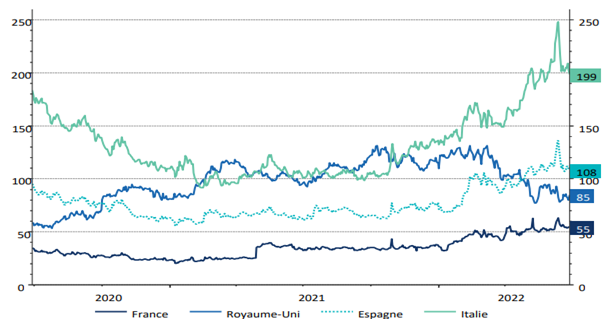

From a sovereign market perspective, as illustrated in Figure 3, these tensions resulted in a significant widening of ten-year yield spreads relative to the German Bund. 9

Figure 3 shows that Italy was particularly affected, owing both to its structural sensitivity to rising interest rates and to the tense domestic political environment at the time. 10 This episode illustrates how a global geopolitical shock can interact with pre-existing national vulnerabilities and amplify financial fragmentation dynamics.

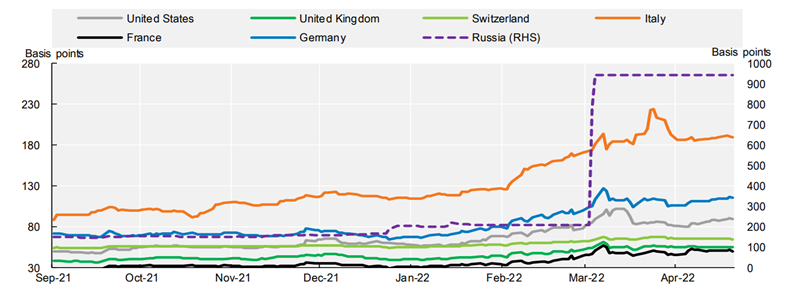

At the same time, the conflict and the associated economic sanctions generated spillover effects within the European banking sector. Several institutions, particularly in Italy and Germany, saw their CDS spreads widen in 2022, reflecting a market reassessment of risk.

According to the OECD 11, this deterioration was driven in part by the direct exposure of certain banks to Russia through their local subsidiaries, by potential losses linked to the forced suspension of operations, and by heightened legal and reputational risks in the context of international sanctions.

Another, more recent example illustrates the persistence and diversity of geopolitical shocks that can affect financial institutions. In early April 2025, the U.S. administration’s announcement of a substantial increase in tariffs, amid an escalation of the trade war, was interpreted by markets as a major political shock. Equity markets reacted sharply, with the S&P 500 falling nearly 6% in a single session and more than 10% over two days. Beyond the equity market correction, this episode highlighted acute tensions in funding markets. According to Reuters, the two-year USD swap spread relative to the Treasury turned sharply negative, reaching around -20 basis points. 12, a level historically associated with periods of marked stress. Reuters notes that this movement reflected strains in funding markets, in the context of heightened risk aversion and a strong flight to safe assets. 13

These different episodes illustrate that geopolitical risk rarely materializes through a single channel. Instead, it unfolds through a combination of macroeconomic, financial, and operational shocks, often with indirect, lagged, and non-linear effects, making their modelling particularly challenging.

It is precisely this complexity that has led European supervisors to view geopolitical risk not as a standalone risk category, but as a structural factor capable of undermining the robustness of internal risk management frameworks. This, in turn, justifies the use of analytical tools such as reverse stress testing to explore institutions’ deeper vulnerabilities.

For a long time, geopolitical risk did not constitute a standalone prudential category within European banking supervision. Until the late 2010s, it was mainly treated as an exogenous macroeconomic factor, indirectly incorporated into adverse stress test scenarios, alongside growth, market, or liquidity shocks.

This approach is clearly reflected in the ECB’s annual supervisory reports prior to 2022. As illustrated in the figures, in the respective contexts of the Brexit referendum and its implementation, the ECB identified geopolitical tensions as one of the most significant risks in its 2016 and 2019 annual supervisory reports. However, these geopolitical tensions were presented primarily as a general source of uncertainty weighing on the economic outlook, without any specific methodological translation within the supervisory framework. 14

A more marked shift emerged from 2022 onwards, in the wake of Russia’s invasion of Ukraine. In its 2022 Annual Supervisory Report, the ECB described geopolitical shocks as amplifying factors, capable of spreading rapidly and in a non-linear manner across the financial system. This implicitly challenged the notion that such risks could be adequately captured through standard macroeconomic scenarios alone.

“Russia’s war (..) also brought economic and financial turmoil to Europe and right across the globe, gradually turning into a fully-fledged macroeconomic shock.”

Andrea Enria, Chair of the Supervisory Board, ECB. ECB Annual Report on supervisory activities

This analytical shift has gradually been reflected in the formal supervisory agenda. The supervisory priorities for the 2024–2026 period, published in November 2023 15 , explicitly call on banks to strengthen their resilience to macro-financial and geopolitical shocks. The ECB emphasises that institutions must be prepared for greater volatility in funding sources, rising funding costs, a potential deterioration in asset quality, and further corrections in financial markets.

At the same time, the ECB acknowledges the limitations of common-scenario stress tests in capturing this type of risk. The 2025 EU-wide stress test conducted by the European Banking Authority incorporates a hypothetical escalation of geopolitical tensions, notably through trade fragmentation and supply chain disruptions. However, this approach relies on a single scenario applied uniformly to all institutions, which limits its ability to uncover bank-specific vulnerabilities, particularly in a banking system characterised by significant heterogeneity in geographic and sectoral exposures.

This limitation was explicitly acknowledged by the Chair of the ECB’s Supervisory Board in a speech delivered on 9 December 2025 16, where she noted that a common scenario may not necessarily represent the most severe scenario for a given institution.

“The EBA stress test applies a common adverse scenario to all banks, which then leads to different capital impacts across banks. This ensures comparability. But it also means that the scenario may be more severe for some banks than for others, so that the results may not reflect the most severe risk scenario individual banks need to prepare for.”

Claudia Buch, Chair of the ECB’s Supervisory Board, 2025

Against this backdrop, the ECB announced on 12 December 2025 the launch of a thematic reverse stress test focused on geopolitical risk, to be conducted in 2026 and covering 110 significant institutions. The exercise is built around a common target outcome (a decline of at least 300 basis points in the CET1 ratio) from which each bank is required to develop its own plausible geopolitical scenarios.

The choice of reverse stress testing reflects the nature of geopolitical risk itself: high uncertainty, limited historical precedents, and complex transmission channels that are not easily captured by predefined scenarios.

A key feature of the exercise is its explicit integration with the ICAAP framework. The ECB has stated that the geopolitical reverse stress test will be carried out as part of the 2026 ICAAP cycle, relying on banks’ own processes, models, and internal data. The aim is to assess the genuine robustness of internal capital adequacy frameworks, rather than institutions’ ability to respond to a stand-alone supervisory exercise. Through this approach, the supervisor is effectively assessing banks’ capacity to identify material institution-specific risks, to design and model severe scenarios, to aggregate risk data in a consistent manner, and to define management actions aligned with their capital planning and recovery arrangements.

From a prudential perspective, the ECB has explicitly ruled out any automatic impact of the exercise on Pillar 2 Guidance. However, it has indicated that the results will be used for qualitative purposes within the SREP framework. This approach is consistent with the SREP methodology, under which weaknesses identified in the ICAAP, particularly in areas such as stress testing, governance, capital planning or risk data aggregation, may influence the overall assessment of capital adequacy and lead to targeted supervisory measures. 17

The geopolitical reverse stress test scheduled for 2026 forms part of a broader shift in European banking supervision, marked by the recognition of geopolitical risk as a structural driver of financial stability. It reflects a gradual move in prudential analysis away from a narrow focus on loss quantification toward a broader assessment of banks’ internal capacity to anticipate, analyze, and manage extreme shocks in an environment shaped by persistent uncertainty.

This evolution goes beyond a single exercise. It points to a deeper change in how supervisory authorities approach rare, complex, and potentially non-linear risks.

“ .. heightened geopolitical risks are having an impact on the post-war global institutional order and international economic relations…These evolving risks mean that supervision also has to evolve, and it is evolving.”

Claudia Buch, Chair of the Supervisory Board, ECB, 2024

“Many analytical tools rely on past data. So, at the precise moment when forward-looking risk assessments are needed to cut through uncertainty and identify emerging vulnerabilities, these tools may become less useful.”

Claudia Buch, Chair of the Supervisory Board, ECB, 2024

This approach is explicitly advocated in the Guidelines on environmental scenario analysis 18

published by the EBA on 5 November 2025. The Guidelines state that scenarios should be designed to cover a wide range of plausible futures and that their primary purpose is to inform strategic reflection and the identification of vulnerabilities, rather than to produce forecasts or exhaustive loss estimates.

The EBA stresses that, in the context of risks characterized by long time horizons, limited historical data and uncertain dynamics, the added value of scenario analysis lies primarily in the analytical process itself. This includes the explicit formulation of assumptions, the analysis of transmission channels and the use of expert judgment, rather than the numerical precision of the results. The parallel between environmental and geopolitical risks is especially instructive. In both cases, historical data are limited, dynamics are uncertain and effects may be non-linear, which reduces the relevance of purely quantitative approaches.

“When conducting a scenario analysis, and in the light of current knowledge, institutions should keep in mind that scenario analyses are designed to inform, not dictate, decision-making. Much of the benefits of a scenario analysis lies in the process itself – fostering strategic reflection, identifying vulnerabilities, and promoting cross-functional collaboration – rather than quantitative outputs alone.”

EBA, Guidelines on environmental scenario analysis, EBA/GL/2025/04

The approach adopted by the ECB for the 2026 geopolitical reverse stress test is fully consistent with this logic. By relying on reverse stress testing and embedding the exercise within the ICAAP framework, the supervisor implicitly acknowledges that geopolitical shocks, much like environmental risks, are poorly suited to analytical frameworks based on historical extrapolation and linear economic relationships.

The objective is not so much to produce a precise measure of losses as to test institutions’ ability to reason coherently under extreme scenarios, to understand the causal chains linking a geopolitical shock to a deterioration in capital, and to identify the management levers that could be mobilized in a context of heightened uncertainty.

Taken together, these developments point to a gradual shift in the European prudential framework toward logic centered on analytical and organisational resilience. In this context, the quality of reasoning, the understanding of transmission mechanisms, and the robustness of internal processes become core supervisory concerns, alongside traditional quantitative indicators.

The 2026 geopolitical reverse stress test can thus be seen as a concrete expression of this change in paradigm, in which supervisory authorities seek less to constrain banks through precise numerical outcomes than to assess their capacity to think through and manage extreme shocks in a structurally uncertain environment.

From a methodological standpoint, a geopolitical reverse stress test can be structured around five key steps, consistent with the prudential expectations expressed by the ECB.

The exercise begins with the identification of the capital deterioration threshold (a decline of 300 basis points in the CET1 ratio), corresponding to a situation of significant yet plausible vulnerability for the institution.

The objective is to determine which combination of geopolitical shocks could lead to this outcome.

Define a Taxonomy of Geopolitical Tensions

Starting from the target outcome, the bank develops a limited number of coherent scenarios based on a structured taxonomy of geopolitical tensions, for example:

Category | Examples of Observable Variables |

Trade War / Trade Restrictions | Trade volume growth, Tariff level, Supply chain pressure index |

Energy & Commodity Shock | Oil price, Gas price, Commodity price index |

Sovereign Stress | Sovereign bond spread, Bank credit spread, Interbank spread |

Military Conflict / Security Risk | Conflict event count, Defense spending growth |

Cyber / Infrastructure Disruption | Number of cyber incidents, Operational loss indicator, Cyber risk index |

Table 1:Classification of Geopolitical Risks and Empirical Proxies

Each category is associated with observable macro-financial variables such as energy prices, sovereign spreads, freight indices, bank CDS spreads or geopolitical risk indicators, allowing the intensity of tensions to be measured. These variables form the vector of geopolitical drivers:

Constructing Synthetic Taxonomy Factors

For each category  , a synthetic factor is constructed as a weighted average of standardised variables:

, a synthetic factor is constructed as a weighted average of standardised variables:

Where each variable is standardised via a z-score:

With:

: historical mean

: historical mean : historical standard deviation

: historical standard deviationThis ensures Comparability across heterogeneous variables.

Dynamic Modelling of Geopolitical Risk (GPR)

A synthetic geopolitical risk indicator (e.g. GPR) is modelled as a function of the taxonomy factors:

This specification assumes that the current level of the GPR index depends both on its recent value, capturing the persistence of geopolitical risk over time, and on new geopolitical information Xt that may update or shift the level of risk.

Optionally, the model can be estimated separately for:

which respectively capture geopolitical tensions that signal potential conflicts and the realization of geopolitical events.

The implied stressed GPR path is simulated:

For the estimation of the model, machine learning models (Random Forest, XGBoost, etc.) and Model explainability tools such as Shapley values (SHAP) can be used to capture complex relationships and verify that the transmission channels between observable variables and geopolitical risk factors are economically coherent.

These tools can allow us to quantify how each variable contributes to the target outcome and to identify potential interaction effects within the model, thereby ensuring that the underlying mechanisms driving the results are well understood. Indeed, as explained earlier, in this exercise, the primary objective is not the precision estimates, but the clear identification and understanding of the transmission chains linking geopolitical shocks to financial risk metrics.

Transmission to the Bank’s capital

The standardised geopolitical factor

is used for risk transmission. For credit risk, the geopolitical stress factor affects parameters as follows:

Probability of Default:

This specification is consistent with widely used PD models based on logistic regression. Under this formulation, a positive geopolitical shock ( ) increases the probability of default when

) increases the probability of default when  .

.

LGD and EAD are adjusted directly from their baseline values:

These specifications reflect the economic channels through which geopolitical stress may affect credit risk. In periods of geopolitical tension, collateral values and market liquidity may deteriorate, leading to higher recovery losses and therefore higher LGD. At the same time, borrowers may increase the utilization of available credit lines due to heightened uncertainty or financing constraints, which increases EAD.

The parameters  ,

,  , and

, and  measure the sensitivity of the different components of credit risk to geopolitical shocks. In practice, these parameters can be estimated using econometric models linking variations in PD, LGD, and EAD to the geopolitical risk indicator

measure the sensitivity of the different components of credit risk to geopolitical shocks. In practice, these parameters can be estimated using econometric models linking variations in PD, LGD, and EAD to the geopolitical risk indicator  , based on historical data.

, based on historical data.

Beyond credit risk, the geopolitical stress factor may also influence:

Under reverse logic following steps are applied:

Until:

The resulting scenario identifies the minimum combination and intensity of geopolitical tensions required to generate severe capital deterioration.

As a next step, scenarios are validated against historical benchmarks (e.g., extreme quantiles such as 99%–99.5% and consistency with past geopolitical crises). The objective is to ensure that the shocks are severe, historically anchored, and narratively credible, while remaining consistent with the identified transmission mechanisms.

The exercise must go beyond loss quantification and assess feasible mitigating actions:

Crucially, the operational credibility and timing of these measures must be evaluated under severe and persistent geopolitical stress.

Drawing on extensive experience in regulatory stress testing, ICAAP, SREP and broader risk management frameworks, Finalyse can support you in structuring and securing your geopolitical reverse stress test from end to end.

Finalyse can help you:

Through its hands-on experience in prudential exercises and recognized quantitative expertise, Finalyse can assist in turning the geopolitical reverse stress test into a solid, defensible, and decision-oriented strategic tool for capital management.

Contact banking@finalyse.com

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support