Strategic Asset Allocation (SAA) for Insurers

Our Strategic Asset Allocation (SAA) approach operates with a long-term planning perspective, employing robust investment management principles. We employ a dynamic asset allocation strategy geared toward achieving your investment objectives, whilst factoring in pre-set investment constraints and risk tolerance levels.

The determination of the optimal SAA is a complex, multifaceted process that involves balancing risk and return. It requires collaboration from multiple internal functions such as Asset Management, Asset Liability Management (ALM), and Risk Management. It also necessitates addressing the interests of external stakeholders, including shareholders, policyholders, and regulators.

At Finalyse, we bridge this gap by incorporating an academic perspective with a pragmatic approach to defining the target SAA. Our tailored solutions guide insurers in managing the intricacies of this balancing act at every step of the process. This approach allows you to secure optimal asset allocations that align with your risk tolerance, investment return objectives and insurance business specificities. Our goal is to provide a dynamic, robust foundation, enabling you to navigate market challenges and capitalise on growth opportunities.

How does Finalyse address your challenges?

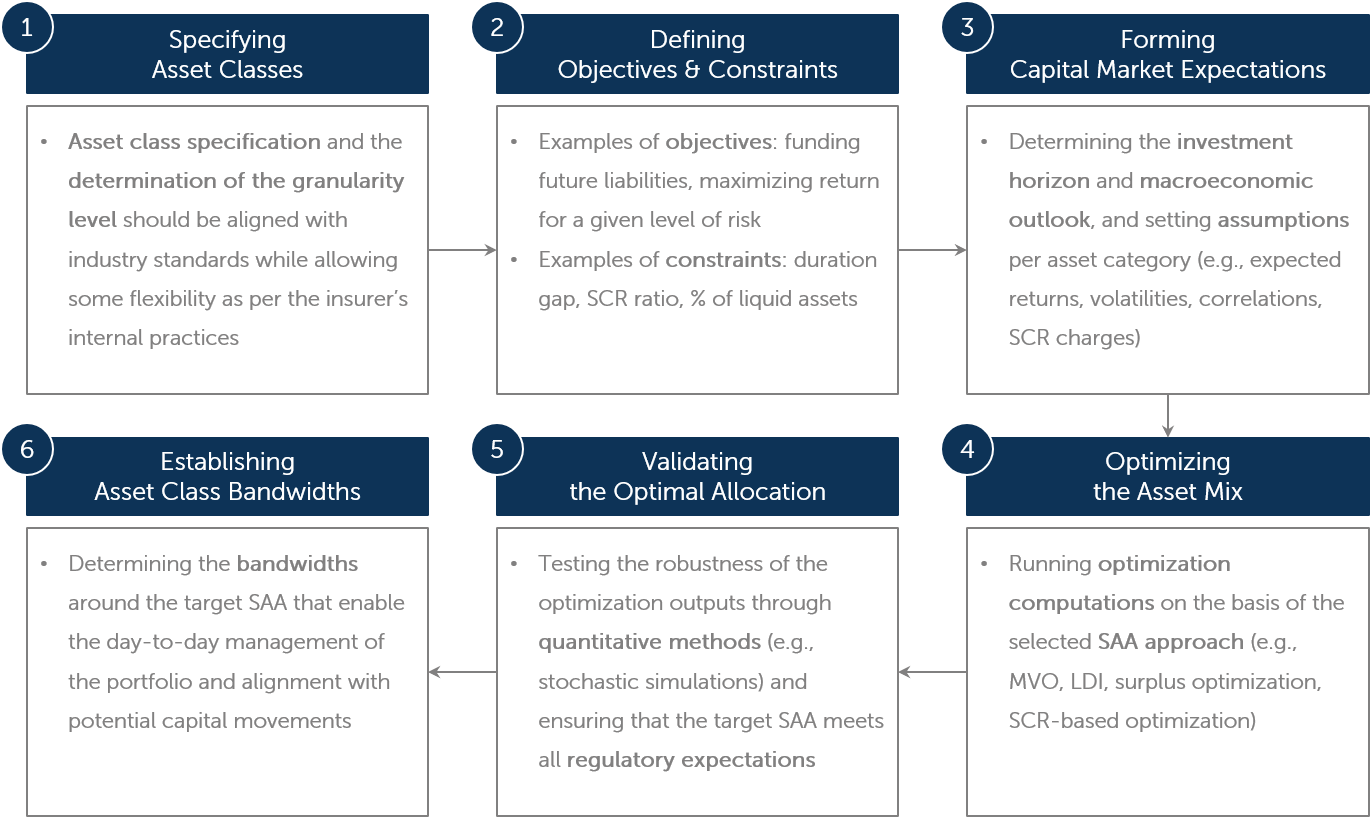

Develop and Implement SAA Optimisation Model and Calculation Engine

Design and Implement an End-to-End Process for the Target SAA's Definition

Integrate Capital Planning, Balance Sheet Management and the Risk Appetite Framework

Align with Regulatory Requirements, like ORSA and the Standard Formula Appropriateness Assessment

Model the Best Estimate Liability cash flows and their Relationship with Asset Cash Flows

Design Derivatives Hedging Strategies for Managing DV01 and CS01

How does it work in practice?

Target SAA determination – the process:

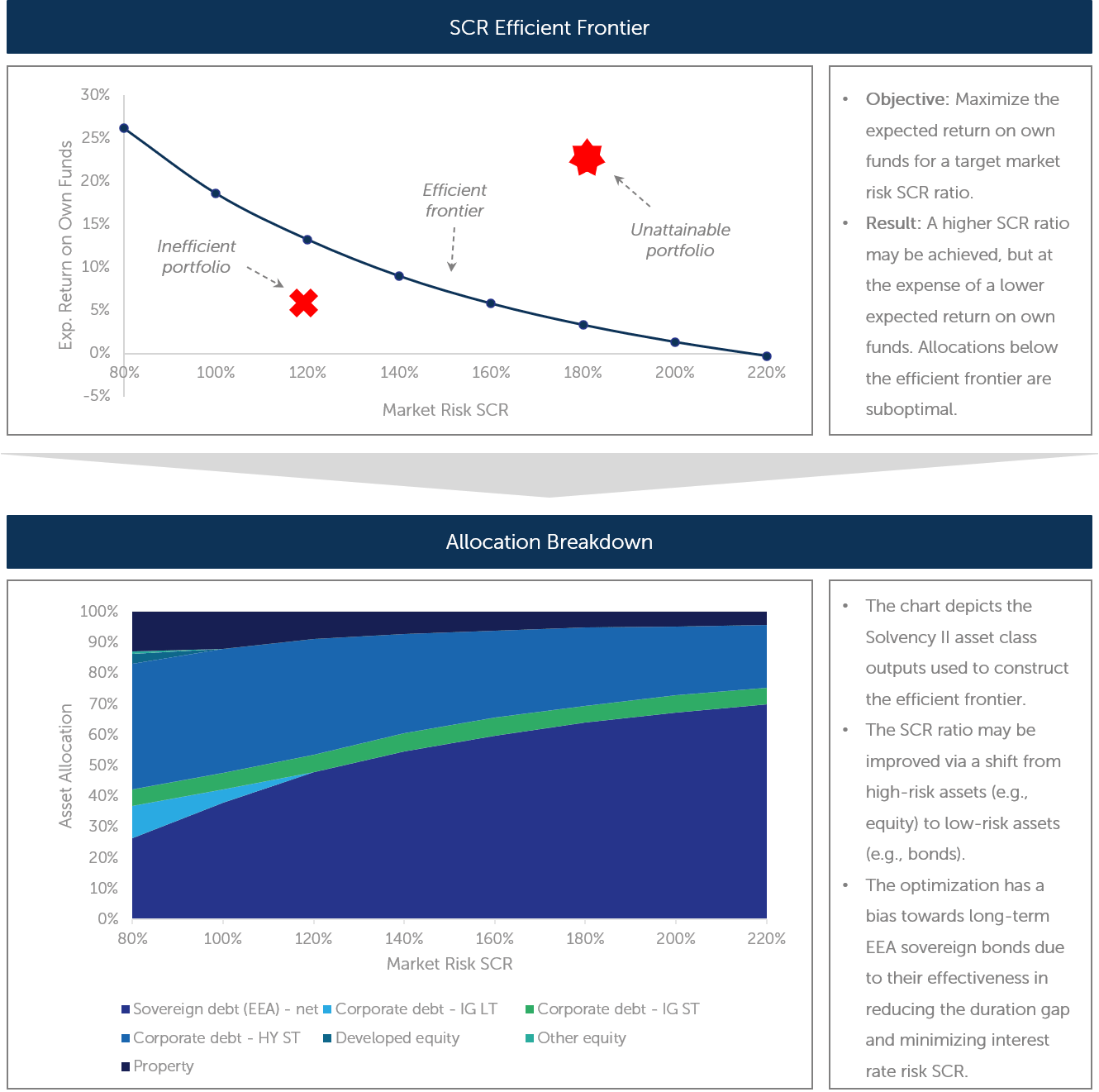

Visualizing the optimal allocation – an example:

Key Features

- A properly defined SAA is crucial for managing the insurer’s solvency and liquidity risks, while generating returns sufficient to meet policyholder pay-outs and maximize shareholder wealth.

- Given the ever increasing regulatory scrutiny in the context of the European Solvency II framework, the SAA must respect the fundamental guiding principles and accepted market practices.

- Finalyse offers extensive experience and expertise on both the asset and liability sides, which provides the necessary scope of knowledge and skills to help determine the SAA that is optimal for your business.

Frans is an actuary and Financial Risk Manager with international experience in the pensions and insurance sectors. He has been specialising in actuarial valuations (AXIS), financial and regulatory reporting (IAS19, US GAAP, IFRS2, IFRS17), regulatory reporting (IORP II, Solvency II, ICS, BMA), market risk management (ALM, SAA), climate change risk management and investment consulting.

François-Xavier is a Principal Consultant with advanced expertise in Financial Markets, ALM and Risk Management, covering both banks and insurance companies. On the banking side, François-Xavier is a practice leader on Valuation, IRRBB, FRTB, VaR, Initial Margin and Counterparty Risk, well acquainted with the regulatory requirements and the market practices surrounding market risks. On the insurance side, François-Xavier has extended experience in the regulatory treatment of financial instruments, ORSA, and hedging balance sheets against interest rate, credit spread and inflation risks.

Sankesh Jain is a nearly qualified actuary with expertise in actuarial reporting and actuarial model modernization within life insurance along with diverse experience in pensions, and regulatory reporting. He specializes in Solvency II and IFRS 17 modelling, reserving, and capital calculations. Skilled in tools such as Excel, VBA, SQL and Python, he supports actuarial valuations, stress testing, and risk reporting. His experience spans actuarial controls, governance, and pension advisory, supported by a strong academic background in quantitative finance and statistics.