Integrating climate change risk into your ORSA, governance and risk-management system

Upskill your key stakeholders on climate change risk management in our free educational workshop.

Evelyn is an actuary and Managing Consultant in Finalyse Dublin. She has 15 years’ experience between consulting and life industry. Evelyn has expertise in regulatory and financial reporting (Solvency II, BMA EBS, IFRS, US GAAP), actuarial and capital modelling, external audit, and risk management. She is currently focusing on climate change risk management and CSRD requirements.

Frans is an actuary and Financial Risk Manager with international experience in the pensions and insurance sectors. He has been specialising in actuarial valuations (AXIS), financial and regulatory reporting (IAS19, US GAAP, IFRS2, IFRS17), regulatory reporting (IORP II, Solvency II, ICS, BMA), market risk management (ALM, SAA), climate change risk management and investment consulting.

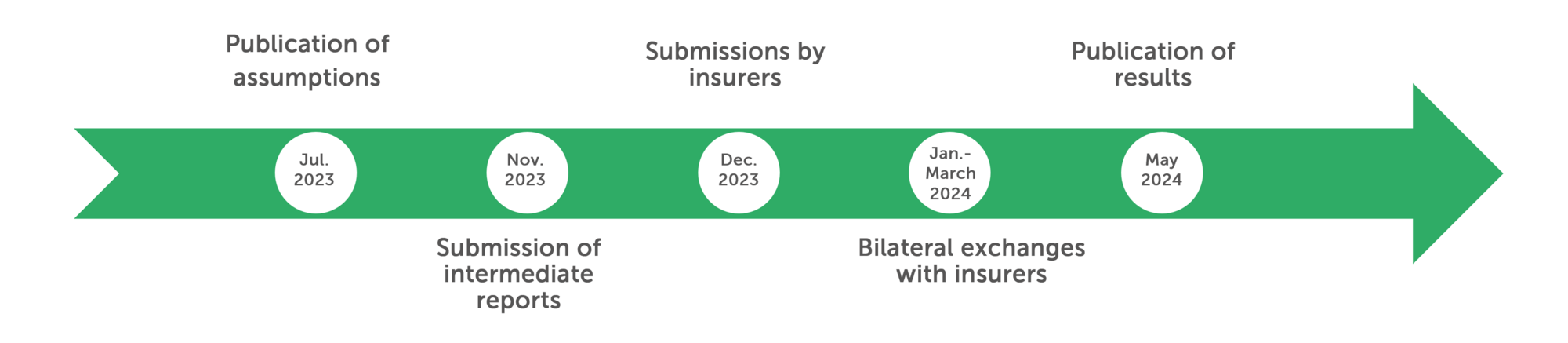

France’s Autorité de Contrôle Prudentiel et de Résolution (ACPR) launched its second climate change stress test exercise in July 2023, which is aimed at insurers. Although the exercise is voluntary, ACPR anticipates significant participation. Insurers are asked to submit intermediate reports by 30th November and final submissions by 31st December 2023, and to have both submissions checked by their administrative, management or supervisory body (AMSB).

The timing of the exercise coincides with the requirement for insurers to include climate change risk analysis in their ORSA, for which monitoring by EIOPA commenced on 1st April 2023. The ACPR scenarios, with the focus on insurance, may therefore be a welcome point of reference for insurers who wish to enhance their ORSA scenarios for climate change risk in the months and years ahead. ACPR includes the following timeline in its paper on scenarios and main assumptions.

Source: Scenarios and main assumptions of the 2023 ACPR insurance climate exercise, July 2023

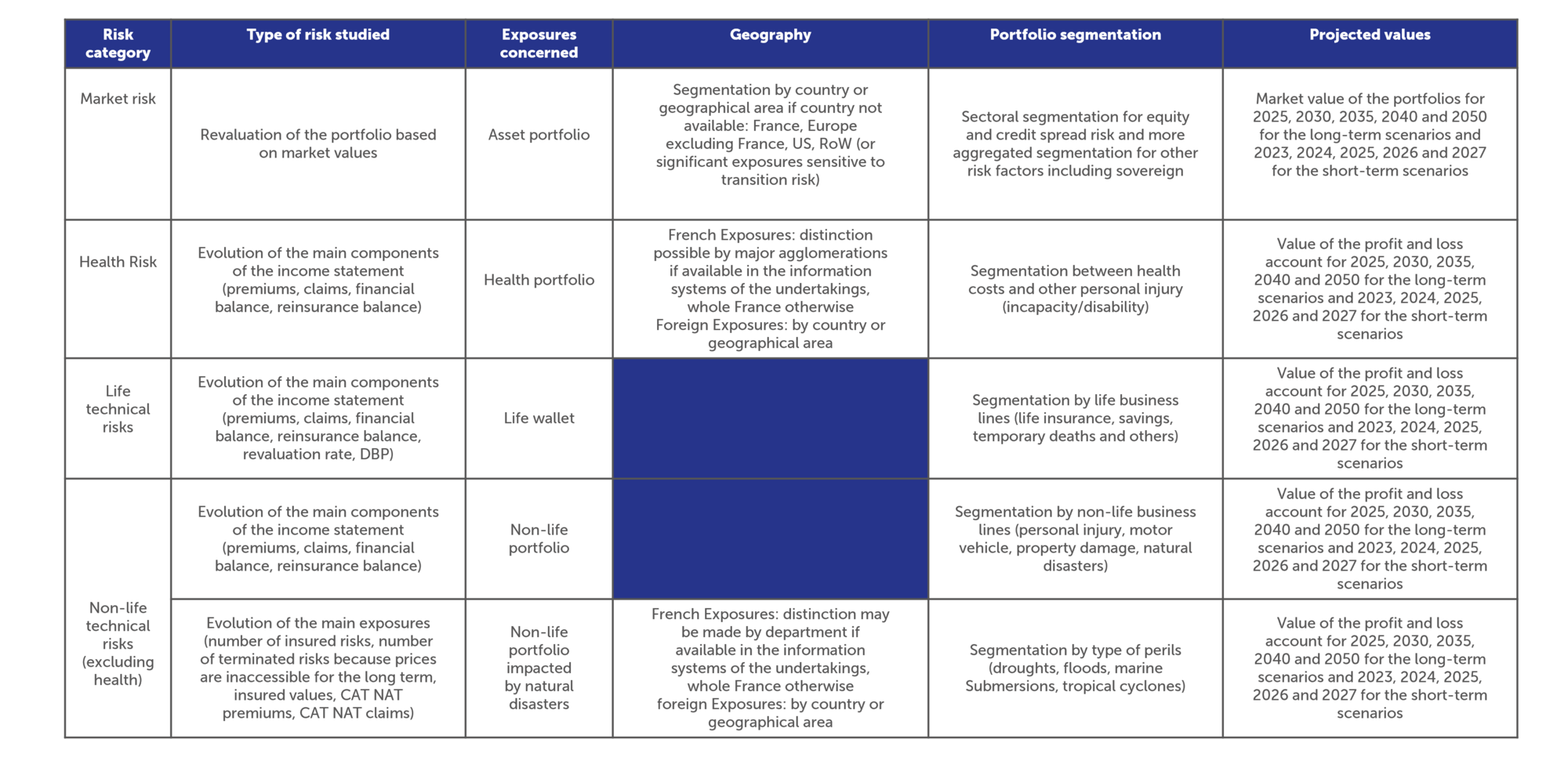

The prudential risk categories in scope of the exercise are market risk and underwriting risk for property damage, motor, health, and life insurance lines of business. The exercise includes three long-term scenarios with assumptions up to 2050 – two stress scenarios, which follow different transition pathways, and a baseline scenario. A short-term stress scenario with assumptions up to 2027 is also included, which aims to assess the vulnerabilities in insurers’ current balance sheets.

The following paragraphs outline the objectives of the exercise and the scenarios based on the paper titled Scenarios and main assumptions of the 2023 ACPR insurance climate exercise. The detailed assumptions are presented in the Annex to the ACPR paper. In the accompanying Technical Guide, ACPR provides additional details on the scenarios and how to use the assumptions.

In the context of climate change risk, ACPR has stated a twofold mission – aiming to safeguard the stability of the financial system and to implement favourable conditions for the financing of an orderly transition. The stress testing exercises support this mission by raising awareness of climate-related financial risks, enhancing the ability of financial institutions to analyse those risks, and encouraging the use of long-term thinking in business planning and strategy. The 2023 exercise also allows ACPR to update its assessment of insurers’ vulnerabilities to climate change risk and the assessment tools it uses to analyse the consequences for the financial system as a whole.

The key enhancements compared to the 2020-2021 exercise relate to the modelling of physical risk and the inclusion of the short-term scenario. The methods for incorporating chronic physical risk into the asset side assumptions have improved and the liability side physical impact assumptions have been provided at a more granular level. The short-term scenario consists of a series of acute physical impacts followed by a financial market shock, which acts as a test of insurers’ solvency under extreme stress.

The approach taken for deriving long-term stress scenarios is in line with the 2020-2021 exercise. ACPR has developed two long-term stress scenarios based on the Network for Greening the Financial System (NGFS) output. These form the basis of the projected macroeconomic and financial assumptions and are used to assess the impact of chronic physical risk and transition risk on assets. In addition, one of the Intergovernmental Panel on Climate Change (IPCC) pathways is used to derive acute physical risk impacts on liability side assumptions for property damage, motor, health, and life insurance.

In a change from the 2020-2021 exercise, the 2023 exercise asks insurers to perform projections under a third long-term scenario, which acts as a baseline scenario. This was developed by the National Institute of Economic and Social Research (NIESR) and is described by ACPR as a fictitious scenario because it has been calibrated to exclude all effects of both physical and transition climate change risks. This provides a common baseline for all insurers and the impacts of both orderly and disorderly transition scenarios will be measured in terms of their deviation from that baseline. This will give an estimate of the cost of orderly transition as well as the difference in cost between the orderly versus disorderly pathways.

For the asset side and market risks, ACPR in conjunction with Banque de France teams derived assumptions based on the Phase III update to the NGFS scenarios, published in September 2022. Among the Phase III enhancements were improvements to the modelling of physical risk, including the incorporation of chronic physical risk impacts in the macroeconomic variable projections. This fits with ACPR’s objective of taking better account of physical risk. The updated modelling approach extrapolates observed damage, using the Kalkuhl & Wenz (2020) damage function, to estimate the effects of chronic physical risks by 2100.

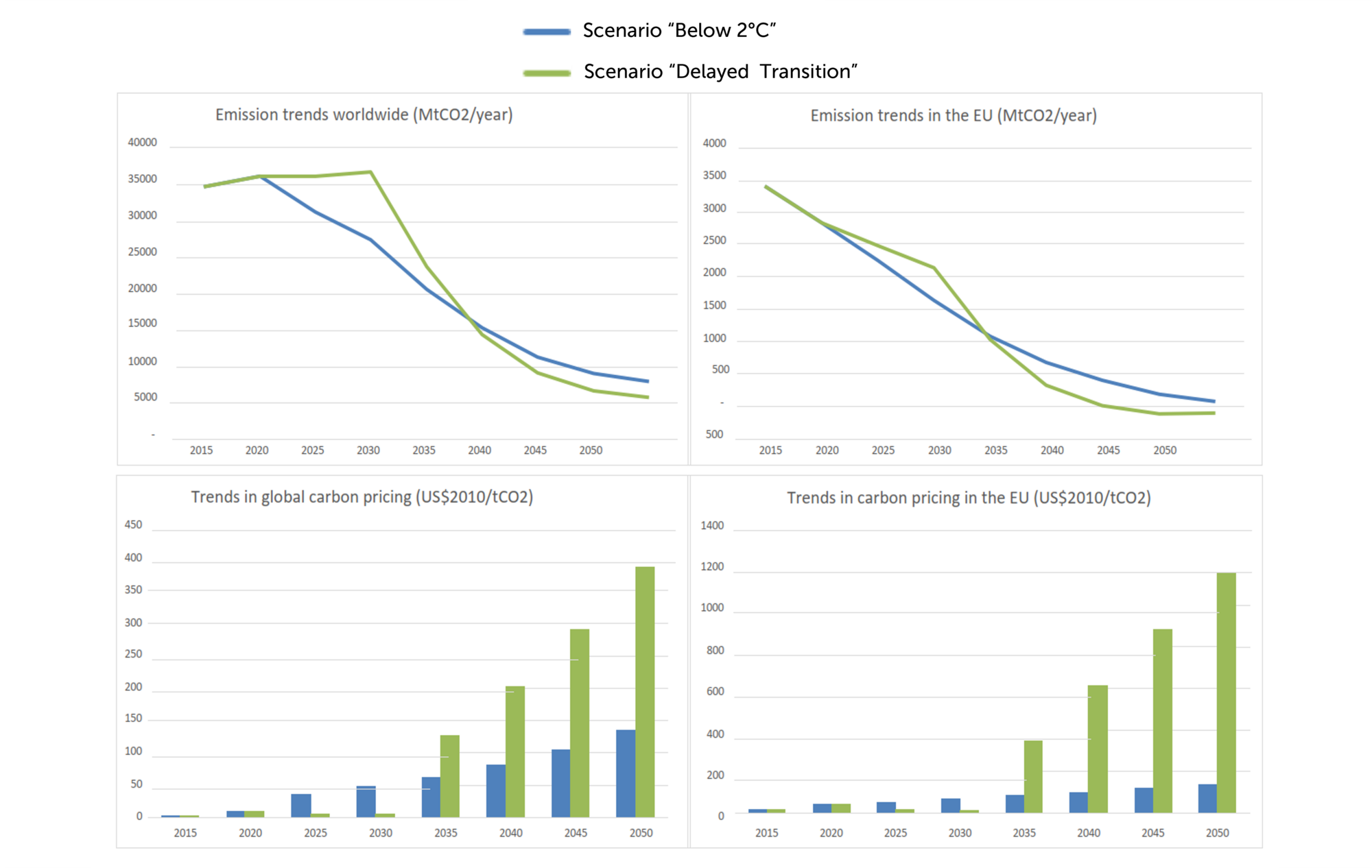

The NGFS scenarios selected were the Below 2⁰C and the Delayed Transition scenarios. The projected temperature increase by the year 2100 is the same in these scenarios, with both calibrated so that the probability of a temperature increase of below 2⁰C by 2100 is 67%. This results in physical risk impacts of the same scale.

The difference between the scenarios is the timing of the transition. The Below 2⁰C scenario represents an orderly transition and assumes early adoption of environmental regulations, gradual green technological advances, and alignment between countries. The Delayed Transition scenario represents a disorderly transition and assumes a delayed response followed by harsher regulations to compensate for the inaction, but with divergence across the globe. The difference stems from the carbon price variable, which increases gradually from 2025 in the orderly scenario, but has a sharp and sudden increase in the year 2035 in the disorderly scenario.

The following illustrations from ACPR show the projected emissions pathways and carbon prices.

Source: Scenarios and main assumptions of the 2023 ACPR insurance climate exercise, July 2023

Insurers are asked to revalue their bond and equity portfolios at fair value under each scenario using a marked-to-market approach. This will involve asset pricing projections for each sector, allowing for changes in credit spread per sector, and government bond valuations. This is described in more detail in the Technical Guide. Where the best estimate liabilities depend on financial income, the liability values should be adjusted accordingly.

Macroeconomic assumptions for variables such as GDP, inflation and unemployment are provided for four geographic regions: France, Rest of Europe (including UK), USA, and Rest of the world. Other financial assumptions include projected risk-free interest rates for maturities of 1 to 20 years from EIOPA and projected stock market indices, credit risk spreads and sovereign interest rates for various geographical areas (France, Germany, Italy, Spain, UK, Euro area, US, and Japan). The equity indices are broken down by sector for 22 groups of NACE sectors and the credit risk spreads are provided for 12 grouped sectors. Sectors identified as less carbon-sensitive are grouped into aggregate categories.

National real estate price trajectories are also provided, along with regional-specific real estate price shocks for France to reflect the Climate and Resilience law that is coming into effect in the country.

On the liabilities side, climate change effects mainly relate to the acute physical risk impacts. These may result in increased frequency and cost of extreme weather events, increased spread of tropical diseases and epidemics, and associated increases in disability and mortality rates. These increases will not only impact insurers’ liabilities, but also the pricing of insurance, and could result in some risks becoming uninsurable. This would have a knock-on impact on the insurance gap and government compensation schemes.

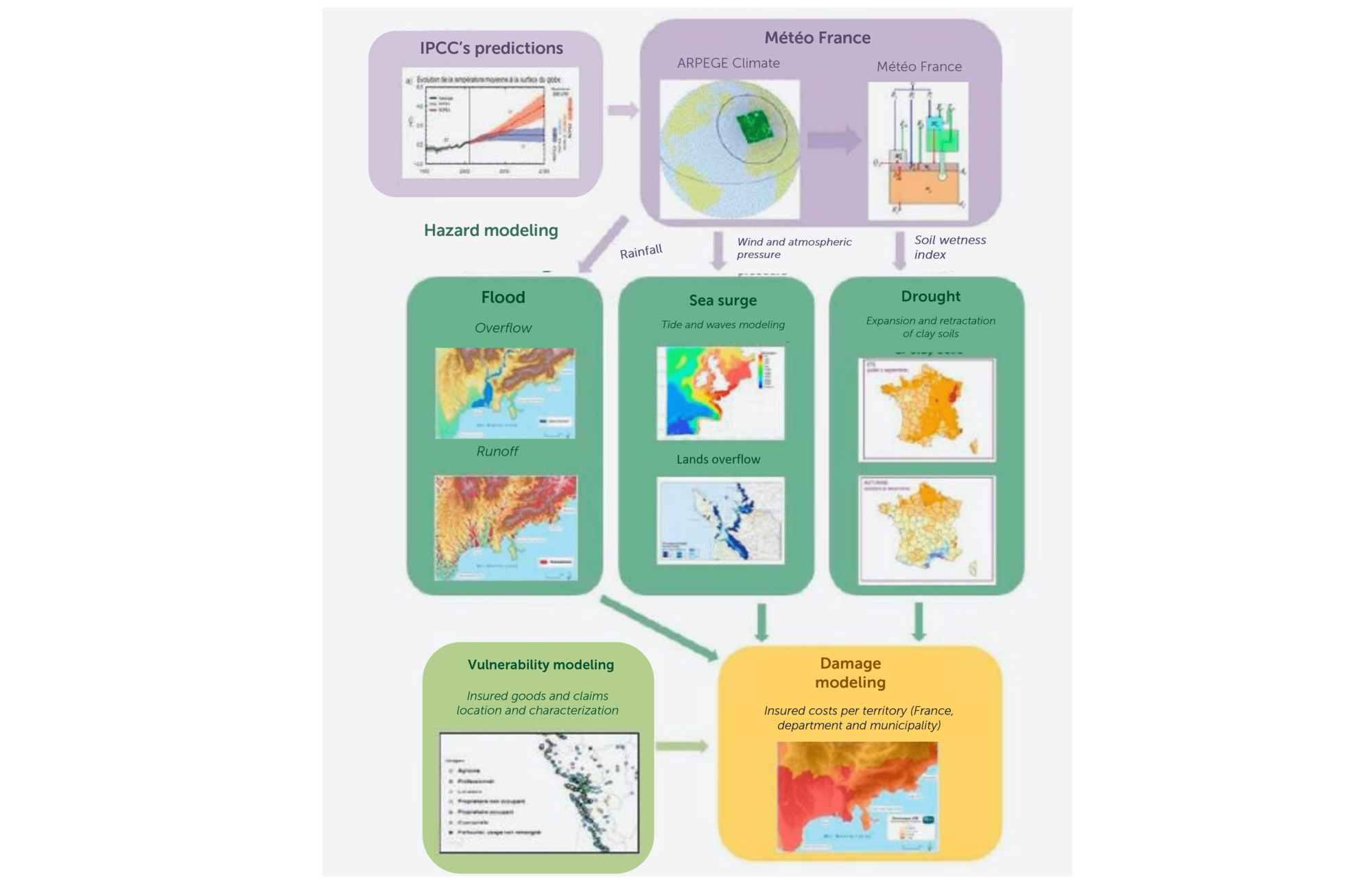

Acute physical risk projections for non-life insurance risks are prepared in line with the RCP 4.5 pathway which has a projected temperature increase of between 0.9⁰C and 2.0⁰C in the year 2050. This is consistent with the NGFS scenarios used to assess the impact on the assets. For property damage and motor insurance, the Caisse Central de Réassurance (CCR) offers to provide insurers with projected loss experience for exposures in France and overseas French territories. A more granular set of damage projections is available from the CCR compared to the 2020-2021 exercise, with a distinction between changes to insured stakes and changes to hazard rates.

The analysis by the CCR is based on projections made by Météo France using its Arpège Climat model and a local hydrometeorological model for soil wetness in France and Corsica. These models provide projections up to 2050 based on the RCP 4.5 pathway for perils such as river floods, droughts, coastal floods, and cyclonic storms. In addition to the peril projections, demographic projections by INSEE (the French National Institute for Statistics and Economic Research) were used to estimate the number of risks in different regions of France up to 2050. The output is a set of projections for each French municipal region for the value of damages to be covered, the mean loss estimates, and the loss estimate for the 95th quantile of damages as estimated by the CCR.

The following illustration from the ACPR paper shows the process flow for the CCR analysis.

Source: Scenarios and main assumptions of the 2023 ACPR insurance climate exercise, July 2023

Insurers are asked to make allowance for changing policyholder demand upon premium increases for home insurance by including policy terminations in the projections when the premium exceeds a given threshold for the location. This applies to optional policies only, where the homeowner is the occupier, and assumptions for termination threshold by department within France are provided by ACPR. Insurers are also asked to project impacts on any catastrophe perils that they are exposed to but that are not covered by the CatNat natural disaster compensation scheme in France.

Insurers who do not wish to get assistance from the CCR and instead derive their own damage projections must comply with the physical risk pathways appended to the Technical Guide to allow for comparability. For exposures outside of French territories, the Technical Guide lists freely available models and data that insurers may rely on to derive damage projections.

For health insurance risks and mortality rate projections, ACPR has conducted an analysis in conjunction with the reinsurance broker AON. The analysis focuses on projected increases in the spread of vector-borne diseases and air quality in line with the IPCC’s RCP 4.5 pathway. The Annex to the APCR paper provides the resulting projected impacts on mortality rates, healthcare costs, and work stoppage for the entire French territory and the largest urban areas.

Following the format of the 2020-2021 exercise, the projections of climate, macroeconomic and financial variables are provided in 5- or 10-year increments for years 2025 to 2050. Insurers may use a dynamic balance sheet assumption for the long-term scenarios, meaning that the projected asset and liability portfolios can be adjusted to reflect future management actions and adaptation measures that they expect to take. Insurers may assume different adaptation actions under each scenario.

Insurers are asked to submit details of their investments broken down by asset type and sector over the projection period. This will give ACPR information on the asset reallocation decisions taken over time and allow them to check that the aggregate investment holdings are consistent with the projected financing needs of the economy over time.

The 2023 ACPR exercise includes a short-term scenario affecting mainland France, involving a sequence of acute physical risk impacts followed by a financial market shock. This scenario assesses the sensitivity of insurers’ current portfolios to extreme events and allows insurers to see how events might unravel over their strategic planning and ORSA timeline. It also acts as a test of solvency under extreme conditions. The impact of the stress will be measured against the baseline scenario.

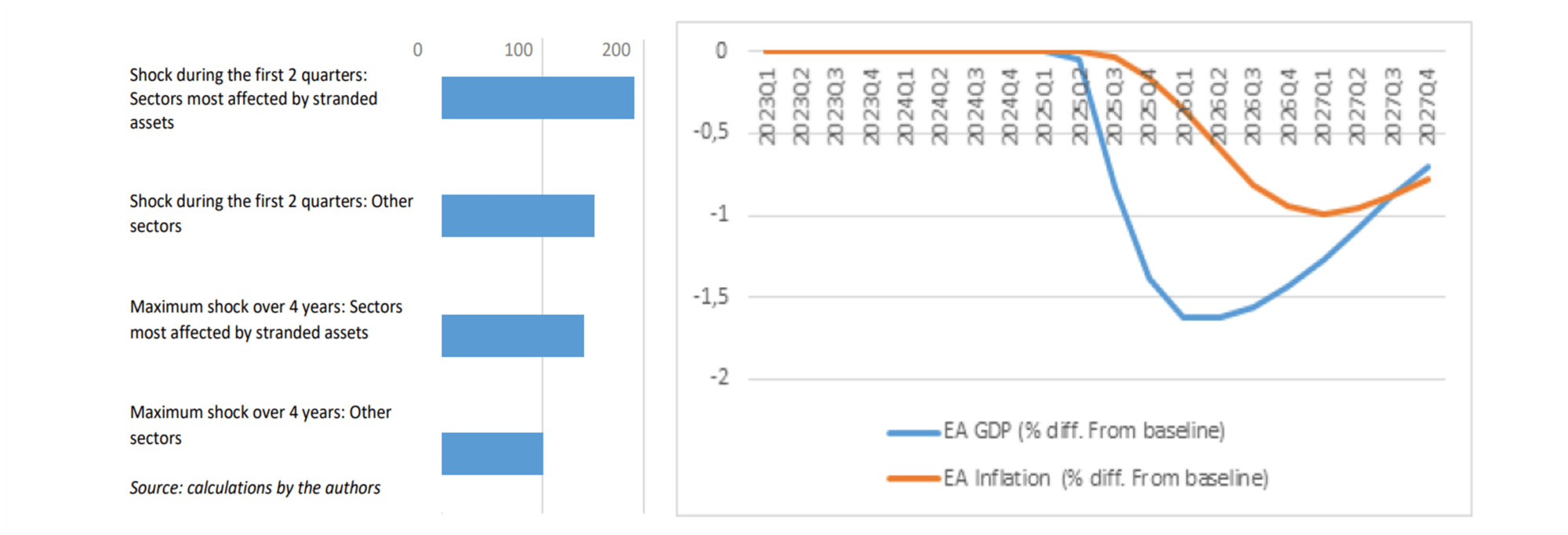

The sequence of events is described by ACPR as hypothetical and as extreme, but plausible. During 2023 and 2024, the drought and heatwave events that occurred in Europe in 2022 are assumed to repeat. The first quarter of 2025 sees heavy rainfall and elevated temperatures, accelerating snowmelt. This results in a historic flood in the Durance River, causing the Serre-Ponçon dam to burst and leading to a wave of high water flooding the downstream region in Q1 2025.

The occurrence of this sequence of events – affecting life, infrastructure, and property – is assumed to lead to heightened market awareness of climate risk and the swift announcement of strict carbon regulations in many major economies. This creates a market shock since markets had not taken adequate account of climate risk, leading to a significant loss in the value of assets sensitive to transition risk in Q2 and Q3 of 2025. Contagion and generalised uncertainty mean that spread shocks affect all sectors and equity values plummet. Markets are assumed to stabilise by Q4 2027 but at lower levels compared to 2024, pre-shock. This is expected to have a disinflationary impact on the Euro area.

Insurers are asked to project the short-term scenario using a static balance sheet assumption, meaning that the balance sheet at year-end 2022 is projected forward without changes for management actions to adapt the insurer’s liability portfolio and investments. For projection years 2023 and 2024, insurers are asked to set their liability assumptions in line with their observed loss experience from 2022 for non-life insurance and to use the AON mortality and healthcare costs data from 2022 for life and health insurance. For the impact of the dam burst in Q1 2025, AON provides mortality assumptions at a department level and the CCR provides non-life sector loss experience assumptions.

Short-term stress financial assumptions are derived by ACPR in conjunction with Banque de France teams using the same methodologies as used for the long-term assumptions. Assumptions are provided for each year, from 2023 to 2027, including projections of sector-specific stock market index performance and credit spreads, and sovereign interest rates. These are provided for France, the Euro area, USA, and Japan. The sectoral breakdown uses 12 grouped NACE sectors for both credit spreads and equities. Financial assumptions for a short-term baseline scenario are also provided. These were derived from the 5-year GDP and inflation trajectories in the long-term NIESR baseline scenario for each country or economic area.

The following illustrations show the projected short-term impacts on credit spreads and Euro area GDP and inflation from the ACPR paper.

Source: Scenarios and main assumptions of the 2023 ACPR insurance climate exercise, July 2023

For the intermediate reports submission in November 2023, insurers are asked to provide projections of their asset composition for the long-term scenarios at 5- or 10-year intervals. This will allow ACPR to check that the aggregate investment holdings are consistent with the projected structure of the financing needs of the economy.

To assess the impact on premium affordability and changing policyholder demand, ACPR asks for a qualitative submission. This involves a questionnaire asking for descriptions of management actions that would be taken in response to worsening climate events such as changes to underwriting, pricing and reinsurance policies. This is supplementary to the quantitative modelling of the termination thresholds for optional property damage policies described in the liability side section above.

ACPR also asks insurers to provide a methodological note along with quantitative submissions, outlining the results, any assumptions and simplifications used, and elaborating on any management actions within the projections.

The submission templates for the long-term scenarios include a simplified balance sheet and other ad hoc statements, similar to the 2020-2021 submissions. The short-term submission templates are aligned to the sectoral granularity within the short-term assumptions. ACPR includes the following table in its paper to summarise the statements requested from insurers in addition to the balance sheet projections.

Source: Scenarios and main assumptions of the 2023 ACPR insurance climate exercise, July 2023

ACPR’s 2023 stress test exercise will deliver a robust assessment of the insurance sector in France, with participation expected to cover over 80% of insurance exposures. This will be a valuable exercise for insurers, as they develop and enhance their climate change risk management framework. It will encourage long-term thinking alongside assessing the current sensitivities of the sector. Since the launch of the ACPR exercise in July, Europe has seen extreme wildfires and soaring temperatures in the south along with the wettest July on record in parts of the British Isles. Enhanced understanding of the vulnerabilities of the current balance sheet is crucial to managing climate-related risks.

The timeline for the exercise is relatively short, with interim reports requested before 30th November 2023 and final submissions by the end of December 2023. The modelling required to quantify the scenarios is quite involved, requiring projections of both the asset and the liability sides of the balance sheet under multiple scenarios, along with the revaluing of investments under each scenario on a marked-to-market basis.

In this article, we have focused on the high-level description of the scenarios and the objectives outlined in the ACPR “Scenarios and main assumptions…” paper. The Annex to the ACPR paper and the Technical Guide provide details of the assumptions and how to use them. If you are interested in finding out more, our Finalyse experts are at hand to discuss the details of the exercise and to help your team develop a suitable modelling approach.

Finalyse has extensive experience and expertise in risk management for insurers. We can assist you in the development and implementation of a climate change risk management framework. Our team of talented insurance professionals can support you in various areas:

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support