Helping you comply with the regulations as well as optimising your Economic Balance Sheet (EBS)

Integrating climate change risk into your ORSA, governance and risk-management system

SAA optimisation based on your risk tolerance and specific business needs

Written by Evelyn McNulty, Senior Consultant

In August 2022, the Bermuda Monetary Authority (“BMA”) published the Guidance Note on the management of climate change risk (“the guidance”) which outlines the BMA’s expectations for commercial insurers and insurance groups. This is part of a wider movement in the insurance and banking sectors to recognize climate change risk and begin to analyze exposures and vulnerabilities. This is a strategic priority for regulators who wish to create a resilient financial sector and contribute to sustainability.

The physical and transition risks stemming from climate change will impact underwriting activities, asset portfolios, strategies and operations. The guidance notes that the insurance industry in Bermuda plays an important role in the climate change risk domain. There is significant exposure to natural catastrophes and a variety of other risks from across the globe, as many large reinsurance entities are located there. The BMA expects insurers to incorporate climate change into their risk management framework and strategy and take a long-term view, to help ensure resilience and financial soundness of the sector and to enable the sector to be proactive in offering insurance solutions, and to contribute to transition and mitigation.

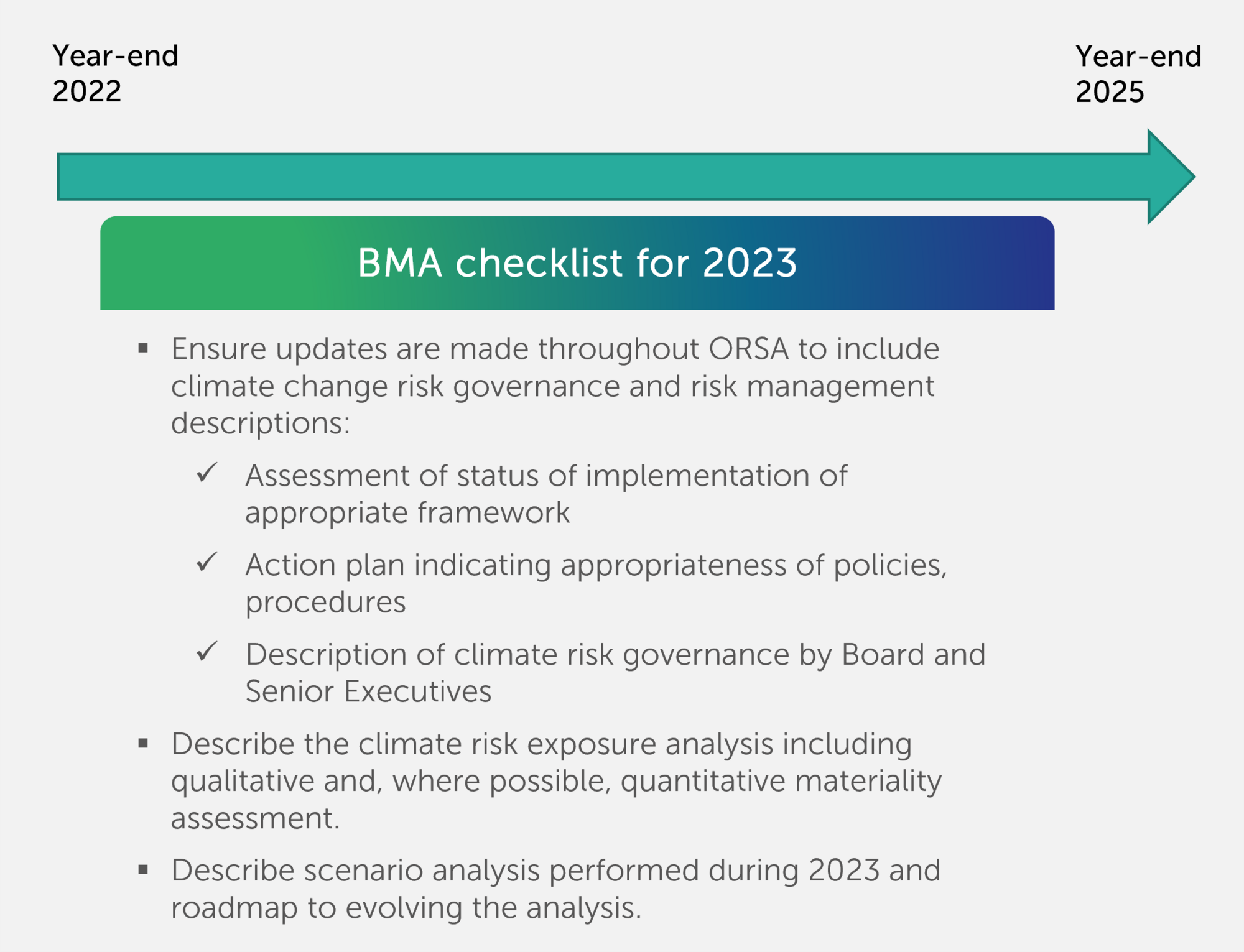

The BMA acknowledges that not all insurers have a comprehensive climate change risk management framework at present. However, insurers are expected to assess the appropriateness of their current policies and processes at year end 2022 and establish an action plan to progress towards a fully established framework by year end 2025. During this implementation phase, and beyond, insurers should regularly evaluate their approach and respond to the evolving climate change landscape. While the guidance targets a minimum standard, the BMA expects insurer’s application to be proportional to the nature, scale and complexity of their risk profile.

The BMA guidance presents a broad view of the expectations including Board responsibilities and governance, strategy, risk monitoring and escalation regimes, staff training requirements, as well as the ORSA and scenario analysis expectations.

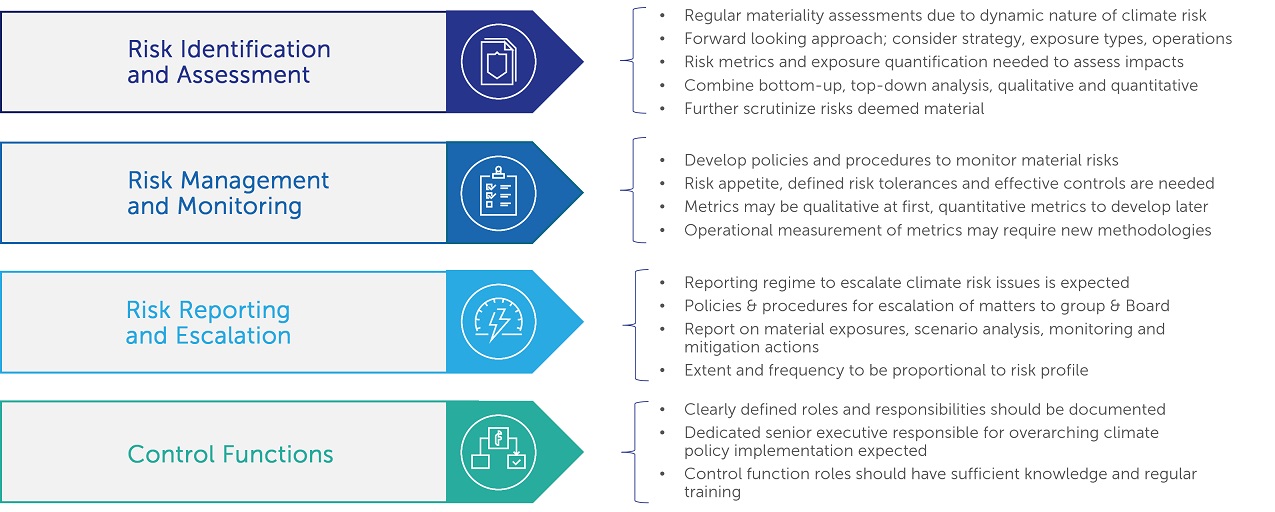

The guidance attributes the ultimate responsibility for governance and oversight to the Board which, together with senior executives and Board committees should have clearly documented roles and responsibilities for monitoring and addressing climate change risk. The Board should understand and assess the financial risks stemming from climate change that affect the insurer, taking a forward-looking approach.

Climate change considerations should be embedded in the strategy setting and governance processes accounting for the long-term and far-reaching nature of climate change risks. The BMA expects a climate change risk appetite to be established together with a reporting regime for escalating climate risk issues to senior executive and Board level.

The guidance states that insurers should have a consistent approach to climate change risk across the insurer and across the group, where relevant. There should be sufficient expertise present at senior management and Board level, proportional to the insurer’s risk profile. The BMA expect the insurer to embed a training requirement for the Board and relevant staff along with access to external resources, to enable the Board to fulfil their responsibilities. The BMA will review and monitor insurers’ governance frameworks and recommends that insurers regularly assess the effectiveness of key control functions, climate risk management and reporting frameworks.

Insurers must establish a sound and effective Enterprise Risk Management (“ERM”) framework that is proportional to the risk profile. The BMA suggests that an appetite statement specific to climate risk should be developed. This is in addition to incorporating climate change risks into each part of the existing framework. The responsibility for successful management for climate change risk is shared across all control and business functions; however, a dedicated senior executive responsible for ensuring consistent climate change policy implementation.

A typical ERM framework might include the following stages:

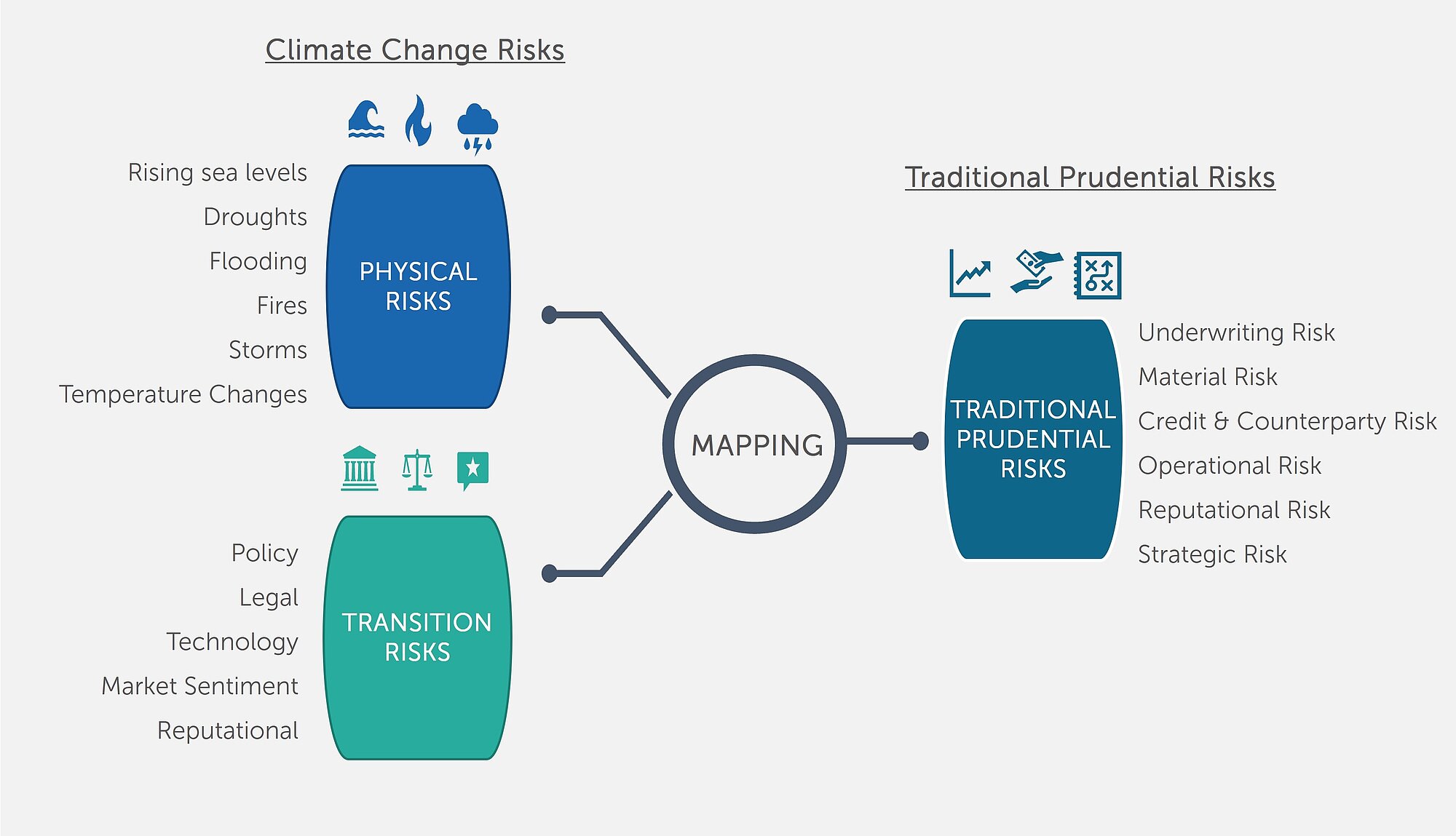

As part of the process to assess materiality and potential financial or strategic impacts, the climate related risks must be mapped to traditional prudential risks that insurers monitor. Climate change risk already presents itself through these risk channels. This mapping allows insurers to identify how their financial objectives, solvency and business plan might be impacted.

The guidance includes examples of climate change risk identification and monitoring in several of the traditional prudential risk categories. This is not an exhaustive list and insurers should consider the risks relevant to their own portfolio. Taking underwriting risks as an example, the following table summarises the information in the guidance:

| Underwriting risk example | |

|---|---|

Identification | This involves mapping of various physical and transition risks that are relevant to the insurer’s liability portfolio. Physical risks are, at times more obvious and may include more frequent and severe weather events causing increased claims, mortality or morbidity impacts, and secondary impacts from claims inflation. Transition risks mapped to underwriting risks may include underwriting changes, product development or strategy changes driven by reputational aspects, consume preferences or technology. |

Monitoring | This requires tools, systems and data flows be in place to assess exposures with a forward-looking approach. New methodologies and metrics will be needed to track the climate related exposures. Long-term trends need to be monitored as the climate situation evolves and monitoring metrics updated accordingly. Insurers may consider changing their policy conditions, pricing approach or updating underwriting procedures to capture climate exposures of their customers at point of sale or to screen customers, e.g., significant exposure to litigation liability cover in carbon industries. |

The guidance reminds us that the ORSA, which is also known as GSSA or CISSA under the BMA, is used by insurers to assess the adequacy of their capital position and to manage material risk exposures. The BMA expects insurers to consider climate change risk in the ORSA from year end 2022 onwards. Insurers should evaluate climate change risk and describe their risk management procedures and governance, proportionate to their risk profile.

The governance description should include how climate change considerations feed into strategy, identify key roles and the responsible personnel, and demonstrate how climate change risk management is implemented at each level of the organisation. Strategy should be evaluated at least annually, and a description of the review process and its frequency included in ORSA. The risk reporting and escalation regime from function units up to Board level and any group or third-party involvement in the process should also be included.

As part of the risk management description, the insurer should set out its climate change risk appetite, risk tolerances and limits and future management actions to mitigate the risk. Both risks and opportunities for the insurer should be described, and its alignment with its overall ambition with respect to climate change risk. The guidance states that the view taken on climate change should be continuously evaluated for appropriateness as the situation evolves. In practical terms, this might translate to regular dedicated climate change review points by control functions and business units, feeding regularly into the Board.

The climate change scenario analysis should include short, medium and long-term considerations. Short term scenarios that may have a more immediate impact on the insurer should be more robustly discussed. The use of longer-term scenarios may be more relevant to strategy planning, and their use may be proportionate to the risk profile and nature of the business, such as the duration of assets and liabilities. The ORSA should describe the information relied upon in the qualitative and quantitative analysis which should be sound and up to date.

The guidance suggests using a base future scenario and extreme scenarios, such as a hot house world or disorderly transition. The scenarios should cover the material physical and transition risks and should be assessed with and without management actions. There are publicly available tools and information to assist with this process which the guidance does not specify. Some of the of the better-known sources are the the Network for Greening the Financial System (“NGFS”), the 2-Degree Investment Initiative (“2DII”) and the UN’s Intergovernmental Panel on Climate Change (“IPCC”).

Scenarios combining different degrees of physical and transition impacts are preferred due to the interlinked nature of these risks. However, this requires more sophisticated modelling and the BMA acknowledges that insurers may use more simplified approaches initially and enhance the modelling as they gain experience. The quantification may take the form of

The guidance describes climate change risk as having a transversal nature and this view is reflected in the broad range of expectations described which span across the insurer’s risk management and governance framework. The BMA recognises that insurers are at different stages of incorporating climate change risk into their framework. The year-end 2022 ORSA should document the current status and the BMA expects gradual progress towards a fully operational framework by year-end 2025.

The guidance emphasises that the overall purpose of the ORSA is for insurers to assess the capital position and vulnerabilities, as well as risks material to their own portfolio with a forward-looking view. Climate change risk should be part of this. The BMA will consider proportionality and risk profile but given the outlook for climate change it is expected to be material to most insurers, at least in their strategy considerations.

The implementation phase up to year-end 2025 gives insurers time to build knowledge internally. The guidance specifies expectations for training of key staff and an action plan to address gaps in current risk management policies and procedures. External data sources and experts can be relied upon to achieve these requirements, and all resources used should be documented in ORSA.

The BMA’s expectations are aligned with EIOPA’s which is to be expected given the Solvency II equivalence status of the BMA regime. EIOPA’s 2021 ORSA Opinion and August 2022 application guidance gave significant focus to the processes of climate change scenario definition and exposure materiality assessment. The following Finalyse articles and the EIOPA guidance are a useful read when considering the BMA guidance.

EIOPA Application Guidance 2022

A practical guide for insurers to incorporate climate risk in their ORSA

Finalyse has extensive experience and expertise in risk management for insurers and can assist you in the development and implementation of a climate change risk management framework. Our team of talented insurance professionals can support you in the following areas:

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support