Written by Christophe Caers, Consultant

Milenko Petkovic, Senior Consultant

Armagan Demir, Senior Consultant

and Can Soypak, Principal Consultant

On 18th October, the ECB published the methodological outline for the 2022 climate stress test. The ECB approaches the stress test as a learning exercise for both themselves and the supervised institutions. While the proposed methodology remains far from all-encompassing and is rather prescriptive, the main goal is to get a clearer view on the climate-related vulnerabilities and improve data availability. The result of the stress test will be integrated into the Supervisory Review and Evaluation Process (SREP), with no direct capital impact through Pillar II Guidance.

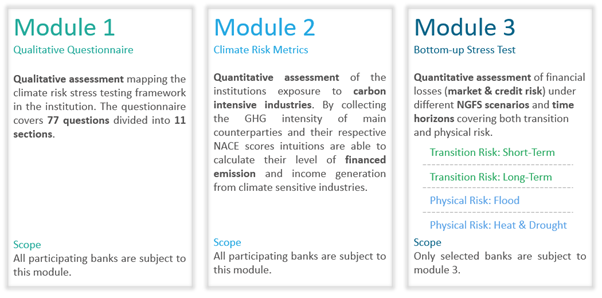

To address its goals, the climate stress test exercise contains 3 modules: a qualitative questionnaire, a reporting of climate risk metrics and the stress test for Pillar 1 risks. The following section provides an overview on these modules, therefore clarifying the ECB’s requirements and how institutions can address them.

The first module of the template is a qualitative questionnaire. The purpose of this questionnaire is to provide in-depth information related to the maturity level of climate risk stress testing frameworks within the institution in terms of modelling, assumptions, and governance. The template consists of 11 blocks, where the first 10 blocks refer to the generic internal stress testing framework of the institution, while block 11 digs deeper into the assumptions used for the 2022 climate risk stress test exercise.

More specifically, the institution is asked to detail to what extent ESG topics are already being considered in different processes throughout the bank, including pricing, credit approval and stress testing. Moreover, the bank is asked to provide some insight into the current or future governance framework and discuss which teams will oversee creating and validating the stress tests. This includes an explanation about the methodological choices with regards to climate risk such as the recognition of appropriate transmission channels through which the risk may materialise, and which portfolios will be subject to a material impact. Likewise, further details should be provided on the scenarios considered and whether they were internally developed or sourced from third parties or public institutions. The data section in the questionnaire, on the one hand, asks what kind of information is available within the bank, which data can be gathered from counterparties, and which can only be acquired from third parties. The questions also give insight into what type of data the ECB considers relevant drivers for the quantification of climate risk moving forward. This includes emission data, energy labels for real estate and location data, but also some disclosure of ESG targets and strategies from counterparties. On top of the questions related to the methodological choices, the questionnaire is gathering information on how the banks are treating the outcomes of the stress test in terms of distribution towards senior management and relevant committees, as well as the inclusion into the strategy and public disclosure.

Block 11 requests additional information regarding the different parts of the 2022 stress tests: Disorderly Transition (Short-Term), Transition Risk Strategy, Drought & Heat Risk and Flood Risk. The bank is expected to provide details on the scope and data coverage for the short-term stress test, the strategic decisions that will influence the portfolio composition and evolution for the long-term stress test and finally the impact of public and private insurance coverage on the physical risk impact scenarios.

Apart from the qualitative questionnaire laid out in Module 1, operational risk is also assessed in Module 3 with a second questionnaire. The ECB recognizes that climate events could impact institutions from both an operational and reputational standpoint. Controversies about negative environmental effects of products provided by the banks or their clients could damage their reputation. With the survey, the ECB expects the institutions to provide more details on whether operational risk in the scope of climate risk is considered within their current framework and what mitigating actions are proposed in case of an operational risk event.

To get a first indication on the transition risk exposure of the banks, banks are required to provide general climate risk metrics in module 2. The setup aims to determine the institution’s dependence on climate intensive industries in terms of income generation. Moreover, the exercise serves as a first step for many banks to start building their climate risk-related databases which will prove useful to meet future regulatory reporting requirements as well as modelling requirements.

In the first part of module 2, banks are asked to map their income and expenses coming from GHG intensive sectors based on the NACE classification. The exercise covers interest, fee and commission income from non-financial corporations in EU and non-EU countries. The definition of the income items should be aligned with the financial reporting framework (FINREP). The financial data and even sector level classification are already available within FINREP, simplifying the data collection process.

The second metric, Financed GHG Emissions, may be more challenging as banks have not been collecting emission data up to now. For the calculation of the counterparty level GHG intensity metric, financial institutions are expected to gather Scope 1, 2 and 3 emissions for the counterparties in annual reports, sustainability reports or from third party providers. The definition of the operational boundaries is aligned with the definitions set out in the GHG Protocol:

While Scope 1 and Scope 2 data is available, Scope 3 is more challenging for most corporations to calculate. Therefore, the stress test leaves room for the institutions to use a proxy approach based on the guidelines created by Partnership for Carbon Accounting Financials (PCAF) in ‘The Global GHG Accounting & Reporting Standard for the Financial Industry’. The PCAF distinguishes 3 different options to calculate the emissions:

Module 3 provides the structure for the first bottom-up stress test conducted by the ECB. Earlier exercises by the regulator were top-down without the involvement of the financial institutions. All the banks are subject to Modules 1 and 2, but the ECB identifies a subset of the institutions that are expected to conduct the scenario analysis covered in module 3. Module 3 includes both transitional and physical risks. Within transitional risk, the template covers the institution’s potential financial loss in the short- and long-term, while Drought and Heat Risk and Flood Risk are covered within the physical risk.

The short-term (ST) stress test assesses a bank’s vulnerability to a disorderly sharp increase in carbon prices taking only credit and market risks into account. The exercise emanates from the Network for Greening the Financial System (NGFS) a disorderly transition scenario (Delayed transition). This scenario assumes stable CO2 emissions until 2030, after which strong policies are needed to limit warming to below 2°C. One of the policies would include a sharp increase of the carbon price by 100 USD over a three-year period starting from 2030 until 2032. However, for the purpose of the short-term stress test, the institutions should conduct the analysis as if the sharp price increase took place in the period 22/24.

Institutions are encouraged to perform a counterparty-level analysis incorporating the carbon price increase impact on credit risk parameters. An Explanatory note should outline how the banks’ models capture the relevant scenario transmission channels. In the figure below, the transmission channels through which changes in carbon pricing can affect a company’s credit profile are displayed:

Based on the channels presented, the credit risk parameters will be affected by the cost increase (estimated using above presented GHG emission and carbon price increase). Two factors will have a role in the assessment of the direct carbon price impact:

GHG emissions: As GHG emissions increase, the impact of the carbon prices will be more significant. In December 2019, the European Environment Agency (EEA) published a data visualization on GHG emissions by aggregated sector. The energy supply sector is the most dominant in terms of emissions, followed by transportation and manufacturing industry (e.g. cement). These three industries are contributing to approximately 60% of the total emissions.

Cost pass-through rate: Represents the extent to which changes in marginal cost are reflected in the retail price. The literature mentions several factors that affect the CPT rate - market power, price elasticity, Armington elasticity (the level of substitutability between domestic and imported varieties of a good in a country), transportation costs, etc. (J. Sijm, K. Neuhoff and Y. Chen 2006). The CPT rate will differ across industries. Starting with the energy supply as the most carbon intensive industry, various studies are estimating a high percentage of the CPT rate, indicating resistance on a carbon price increase (J. Sijm, K. Neuhoff and Y. Chen 2006). This study incurs important policy implications, since the complete pass-through signifies that wholesale electricity prices will increase at least in the short run (A.S. Dagoumasa and M.L. Polemis 2020). The CPT rate of the manufacturing industry also varies, but, on average, the rate is slightly lower in comparison to the energy supply, due to the low CPT rates (between 30 and 50%) in cement, iron, steel and glass production according to the “Ex-post investigation of cost pass-through in the EU ETS” conducted in November 2015.

Banks are obliged to assess the overall impact of the adverse scenario accounting for the indirect impact through stressed macroeconomic factors (e.g. decreased aggregate demand, increased unemployment rate, etc.) besides the direct carbon price impact. Using information from the aforementioned exercise, banks are required to estimate credit impairments resulting from the materialisation of stressed scenarios, based in the IFRS 9 methodology (nGAAP if applicable). A list of the requested information is presented in the ECB stress-test methodology and Excel template file.

Banks are also asked to calculate how the fair value of market risk exposures in the scope of the exercise is affected by the carbon price shock – an assessment of the market risk. The starting point will be the fair value and notional value of the trading book positions on 31 December 2021. By assuming a full transmission of the carbon price shock on 1 January 2022, the impacts on the fair value of the equity/bond portfolios are investigated with a breakdown of several risk drivers such as equity, credit spread, interest rates, commodities, FX movements and others. These risk factors may not cover all market risk factors, so banks can also consider the risk factors included in the regulatory models. The ECB will provide banks with the information on GDP, the inflation rate, the unemployment rate, housing prices and details on stock price and bond price shocks for the stress scenario.

Besides the stressed (the disorderly transition) scenario, institutions are also asked to deliver a baseline scenario by applying macroeconomic factors projections from the “December 2021 Eurosystem Broad Macroeconomic Projection Exercise (BMPE)”, to the extent that their internal models require these variables as input.

The objectives of this part of the exercise are:

For this purpose, the long-term stress testing exercise should consider three long-term scenarios based on the high-level NGFS scenarios from now to 2050. The first scenario assumes an orderly transition with a smooth reduction in CO2 emissions to achieve the carbon emission goals. The second scenario assumes a disorderly transition in which CO2 emissions decrease slowly until 2030. The third scenario assumes a hot house world in which CO2 emissions are not reduced and the economy is confronted with a full materialisation of physical risks, resulting in GDP losses.

The ECB will provide the forecasts for a list of scenario variables (GDP growth, interest rates, carbon price, etc.) to perform the projections in each scenario. For each of these scenarios, banks will then assume a dynamic balance sheet for the long-term strategy. Unlike in short-term projections, in the long term, banks are given the flexibility to alter their balance sheet dynamics, thus portfolios can undergo adjustments. It should also be noted that the long-term stress testing should only consider credit risk, but not market risk, which is out of scope.

The other difference is that credit risk projections will be less detailed in the long-term stress testing exercise. The focus of the test is more on banks’ business model and how it reacts to different long-term transition scenarios (e.g. projection of mortgages disaggregated by EPC or corporate exposures disaggregated by industry for each reference date).

Banks are asked to project how their balance sheet will change in each of the three scenarios until 2050, considering bank-specific strategy, reputational risk and business risk as well as the macroeconomic shifts. Based on the credit risk exposure classification of the stress test[1], banks are expected to report their exposures as of 2030, 2040 and 2050. Additionally, a breakdown of exposures in terms of performing and non-performing is required.

Two bases verify the credibility of the balance sheet projections. The complementary bases can be given as the bank-specific strategy and bank’s business environment linked to the scenarios.

The credit risk exposures in scope are an institution’s mortgage and corporate exposures. The mortgage portfolio encompasses the IRB asset classes “Retail – Secured by real estate property”, “non-SME portfolio” and “the STA asset class Secured by mortgages on immovable property – non-SME”. Corporate exposures are split into:

corporate exposures not secured by real estate property,

corporate exposures secured by real estate where the collateral is within the scope of the Energy Performance Certificate (EPC)24, and

corporate exposures secured by real estate where the collateral is not within the scope of the EPC

For details see Climate risk stress test 2022, Section 3.1.1/Table 1

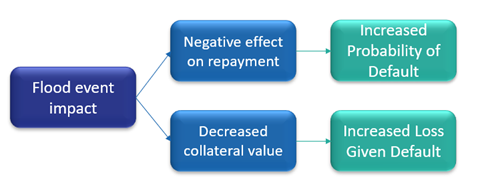

The final part of the 3rd module of the stress test is the assessment of physical risk. While many extreme weather events can affect firms and households, the ECB has limited the exercise to the following two climate risks of key relevance: severe flood and extreme drought/heatwave. The ECB has remained pragmatic in the physical risk assessment and only asks to consider the direct effect of the physical risk on credit risk. Second round effects such as losses borne by insurance companies and macro-economic implications are outside the scope of the physical risk assessment.

Severe flood events can cause significant harm to real estate property in the affected area. As a result, the value of the affected property is likely to diminish. Moreover, even property which has not incurred damage could lose value due to the increased risk of such an event re-occurring. Pistrika and Jonkman (2010) record a 43.3% decrease in property value due to the flooding because of the hurricane Katrina. Other studies indicate that the fall in value is often not permanent but rebounds in a decade or sooner (Atreya et al., 2013; Bin & Landry, 2013). Banks may face a vulnerability to a large flooding event due to abrupt changes in the property values underlying loan collaterals in the case of mortgage exposure by households or other exposures secured by real estate. Besides, a flood might also be followed by short-term costs required for the restoration of the property. If the repairs in addition to mortgage repayments exceed the borrower’s financial capacity, delinquency may occur.

Banks are expected to classify their exposures based on their vulnerability to the flood risk and to estimate the credit losses resulting from the flood event. To estimate the impact, the regulator will provide a flood stress test map which will indicate at the NUTS3 resolution whether the area is no risk, low risk, medium or high risk with respect to a flood event. Additionally, the map will contain the price shocks that need to be applied to the collateral values of the properties under stress. As a secondary impact through other macroeconomic risks (such as GDP decline, increase in unemployment, etc.) is out of scope, new lifetime credit risk parameters can be estimated by assuming the house price decrease is permanent and macroeconomic variables remain constant over the timeframe.

Another focus area for the ECB is a severe drought and heatwave, which reflects the increasing likelihood of long-lasting droughts impacting European countries economies and their agricultural, manufacturing and construction sectors. In this exercise, the banks will be affected mainly through credit risk. The scenario assumes that the entire EU is hit by a heatwave in 2022 which hampers the economic activity and results in output losses for vulnerable industries: the agricultural industry will face reduced crop yields, the tourism industry will also be negatively affected, commercial shipping will suffer due to the low water levels, etc. Besides the direct effects, banks will need to incorporate an indirect impact on other industries through the production chain.

As an input variable, the ECB will provide the value-added (VA) losses at the sectoral level for each EU country using the NACE sectors.

According to the working paper “Climate-Related Scenarios for Financial Stability Assessment: an Application to France” (T. Allen et all, Banque de France, July 2020, WP #774), Value-Added and PD are negatively corelated, which can be seen on the graph below:

")

Figure XX: Probabilities of default and value added by sector (T. Allen et all, Banque de France, July 2020, WP #774)

This working paper inspects the impact of decreased value-added on PD in two NGFS disorderly transition scenarios. The higher the VA loss is (provided by the ECB), the higher the PD of a company will be.

Under the assumption that the provided value-added loss values present an isolated impact of drought risk on an industry (negative value-added growth as it is stated in annex A.4 of the methodology), banks will be able to use GDP as a transmission channel to assess its impact on a PD value. For directly impacted industries, the value-added growth will be applied solely on the baseline GDP, whereas for indirectly impacted industries, the baseline GDP will be decreased by a weighted value-added growth. The weight of each industry value-added growth will be shared in the total GDP.

Banks should take into consideration the insurance and public natural disaster relief schemes with a clear link between the insurance coverage and the hazard outlined in the scenario. Only the insurance/guarantee granted between the moment of loan approval and 31st December 2021 will be relevant in the stress test exercise.

The analysis shows that while the methodological note provided by the ECB is quite clear on the expectations related to each of the modules, the theoretical framework to transform transition pathways into meaningful credit and market risk impacts remains challenging. Financial institutions will need to expand their risk management capacity into the climate risk dimension with the help of academic sources of third-party providers. Overall, the ECB has found an elegant approach to sidestep the overwhelming complexity of climate risk modelling by limiting the scope of the transmission channels considered. Furthermore, by providing the macro-economic indicators and physical risk impacts (expected end of Q1 2022), any ambiguity based on scenario decisions is removed and a comparison can be made from a purely methodological perspective. The ECB has successfully played their role as a door-opener in this developing topic by making the initial exercise digestible while laying the foundations for an increase in complexity in the future.

[1] https://www.bankingsupervision.europa.eu/ecb/pub/pdf/ssm.climateriskstresstest2021~a4de107198.en.pdf

[2] https://www.dnb.nl/media/a4gdcovq/consultation-document-good-practice-integration-of-climate-related-risk-considerations-into-banks-risk-management-nov-2019.pdf

[3] https://www.ngfs.net/sites/default/files/medias/documents/scenarios-in-action-a-progress-report-on-global-supervisory-and-central-bank-climate-scenario-exercises.pdf

[4] 2021 EU-wide stress test - Methodological Note

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support