Francis is a Principal Consultant in charge of our insurance practice in Dublin. He has 15 years of experience within the life and non-life (re)insurance industry. His expertise covers the areas of financial reporting, prudential regulation, and actuarial modelling. Francis has worked in both industry and consulting with extensive exposure to Solvency II and BMA-regulated clients and a keen eye on new regulatory developments.

In the complex world of insurance, effective liquidity risk management is crucial to ensuring that a company can meet its financial obligations as they come due, even in adverse conditions. For (re)insurance companies, maintaining a robust liquidity risk management framework is fundamental to operational stability and long-term success.

The amendments to the Solvency II Directive[1], which were finalised in January 2024, establish comprehensive requirements for managing and monitoring liquidity risk, and ensuring the fulfilment of obligations to policyholders. (Re)insurers will be required to develop and maintain a current liquidity risk management plan that includes short-term liquidity analysis and projecting cash inflows and outflows relative to their assets and liabilities. This liquidity risk management plan will need to be submitted to the local regulator at least yearly. The Bermudian regulator has also published similar high-level guidance on liquidity planning following the release of two consultation papers.

This blog post delves into the intricacies of liquidity risk management planning, offering insights into key principles, methodologies, and governance structures that underpin a resilient liquidity strategy.

Liquidity risk is the uncertainty surrounding a company’s ability to meet its payment obligations in a full and timely manner. For a (re)insurance company, this encompasses the interplay between its assets and liabilities. Effective liquidity management ensures that cash outflows over the next 12 months can be met under both normal and stressed conditions, thereby safeguarding the company from potential liquidity crises.

Principle | Description |

Alignment with Group Standards | Align liquidity risk management policies with broader group standards such as a parent group’s ERM Framework. |

Regulatory Compliance | Align policies with regulatory frameworks, including EU directives and EIOPA guidelines. |

Stakeholder Notification | Ensure effective communication of the liquidity risk management policy to all relevant stakeholders. |

A structured governance framework is essential for effective liquidity risk management. This involves multiple levels of oversight and responsibility:

The liquidity risk management process involves several critical steps:

To project the liquidity position, the Risk Management Function could use the following approach, using these time buckets: 1 week, 1 month, 3 months, and 12 months. For each period, they calculate:

Time Buckets | Liquidity Resources (LR) | Liquidity Needs (LN) | Excess Liquidity (EL) |

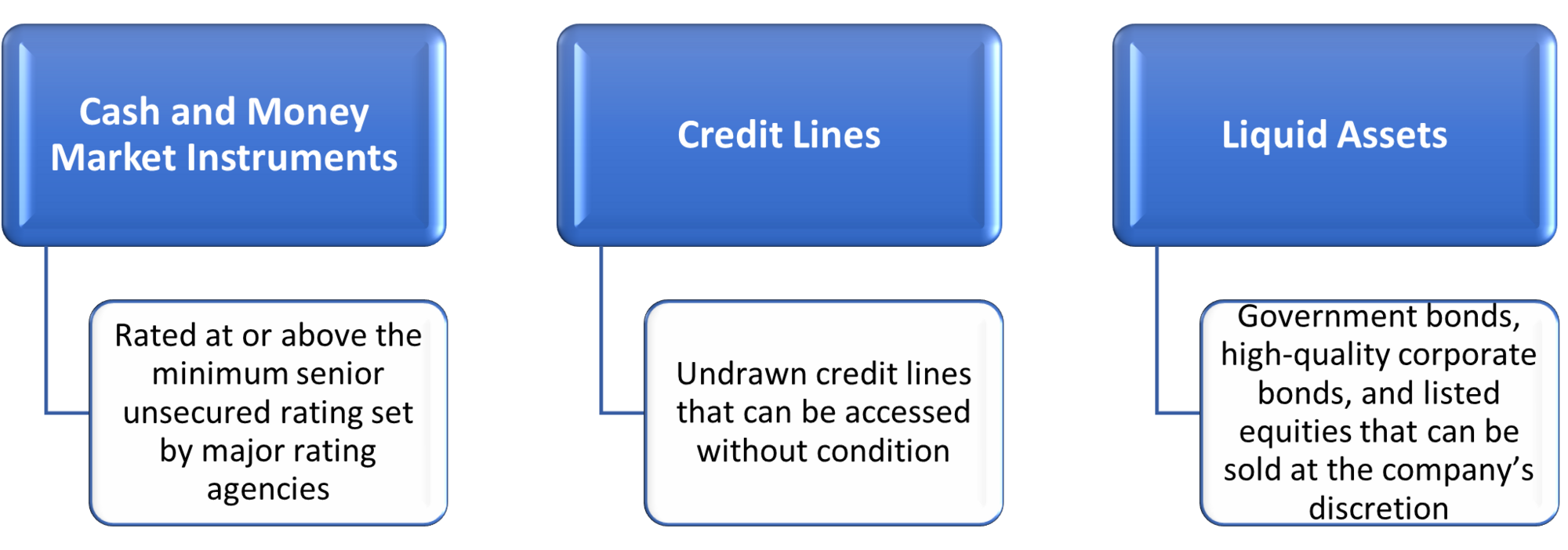

1 Week | Cash, Money Market Instruments | Net Outflows (Outflows - Inflows) | LR - LN |

1 Month | Liquid Assets | Net Outflows | LR - LN |

3 Months | Government Bonds, High-Quality Bonds | Net Outflows | LR - LN |

12 Months | Listed Equities | Net Outflows | LR - LN |

In stressed scenarios, the Risk Management Function applies various shocks to simulate extreme market conditions, such as distressed financial markets, natural catastrophes, and confidence crises. The worst-case scenario helps the company prepare for potential liquidity crises.

Eligible liquidity resources include:

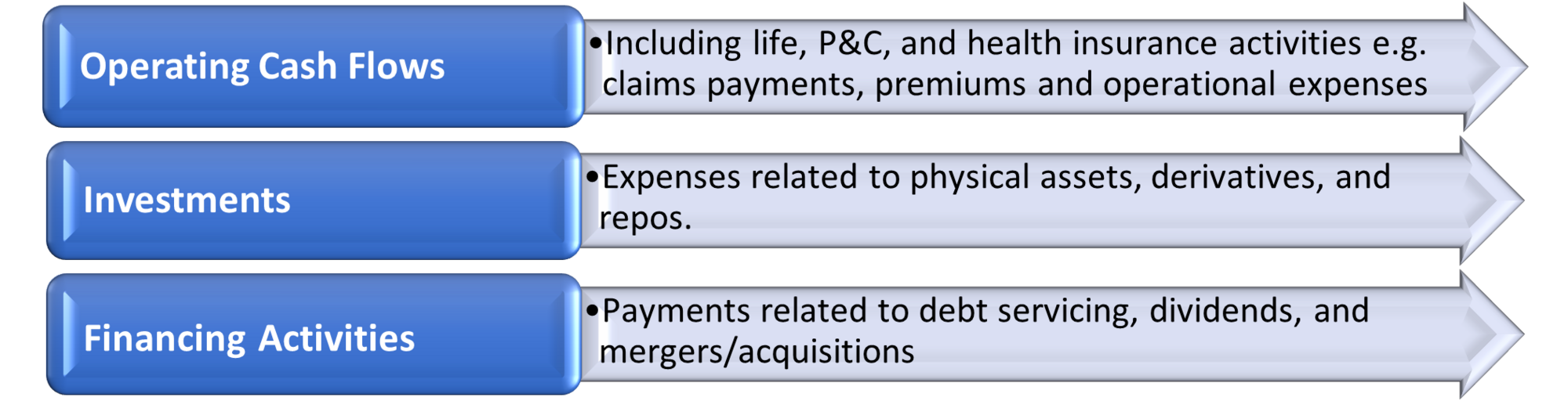

Liquidity needs are determined by summing the outflows and subtracting inflows over the projection period. These needs arise from various sources:

Stress scenarios help (re)insurance companies prepare for extreme conditions by applying shocks to liquidity resources and needs. These scenarios include:

Scenario Type | Example |

Market Shocks | Changes in asset prices, liquidity, and funding access. |

FX Shocks | Currency fluctuations affecting liquidity positions. |

CAT Scenarios | Catastrophic events like earthquakes impacting cash flows and insurance claims. |

A well-defined liquidity contingency plan is crucial for managing potential liquidity crises. This plan involves:

The Chief Risk Officer (CRO) is responsible for developing and reviewing the liquidity risk management policy annually or following any major changes. The policy must be approved by the Board and communicated to relevant internal functions, ensuring everyone is aligned with the company’s liquidity management strategy.

Liquidity risk management is a critical aspect of a(n) (re)insurance company's overall risk management strategy. By implementing a robust framework, aligning with group and regulatory standards, and preparing for potential crises, companies can ensure they remain financially stable and capable of meeting their obligations under any conditions. Through diligent governance, regular assessment, and comprehensive planning, (re)insurance companies can navigate the complexities of liquidity risk and safeguard their operations for the future.

(Re)insurers should anticipate that liquidity risk management will be a significant topic in the coming months. The new Solvency II requirement to produce a liquidity risk management plan for submission to the local regulator will become clearer once the Technical Standards are released by EIOPA. In the meantime, clients can enhance their current processes and begin documentation if they have not already done so.

Navigating the evolving landscape of liquidity risk management, Finalyse offers tailored support for insurance and reinsurance undertakings:

Partner with Finalyse to enhance your liquidity risk management, ensuring resilience and compliance.

[1] The proposal issued by the Council of the European Union on 19 January 2024 -https://data.consilium.europa.eu/doc/document/ST-5481-2024-INIT/en/pdf

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support