Market and Liquidity Risk Management for Insurers

The effective management of market and liquidity risks is critical for any insurance company operating in today's constantly evolving financial landscape. Failure to manage these risks has the potential for devastating consequences, including massive financial losses and reputational damage that can be difficult to recover from.

At Finalyse, our market risk service offering is designed to help our clients navigate these challenges with expert guidance and principled, innovative solutions. Our team leverages our interdisciplinary experience in ALM, Market Risk Management, and Solvency II to deliver value and address your challenges.

Finalyse will support you in identifying, measuring, managing, mitigating, and reporting your market and liquidity risks, ensuring your business’s long-term success and sustainability.

How does Finalyse address your challenges?

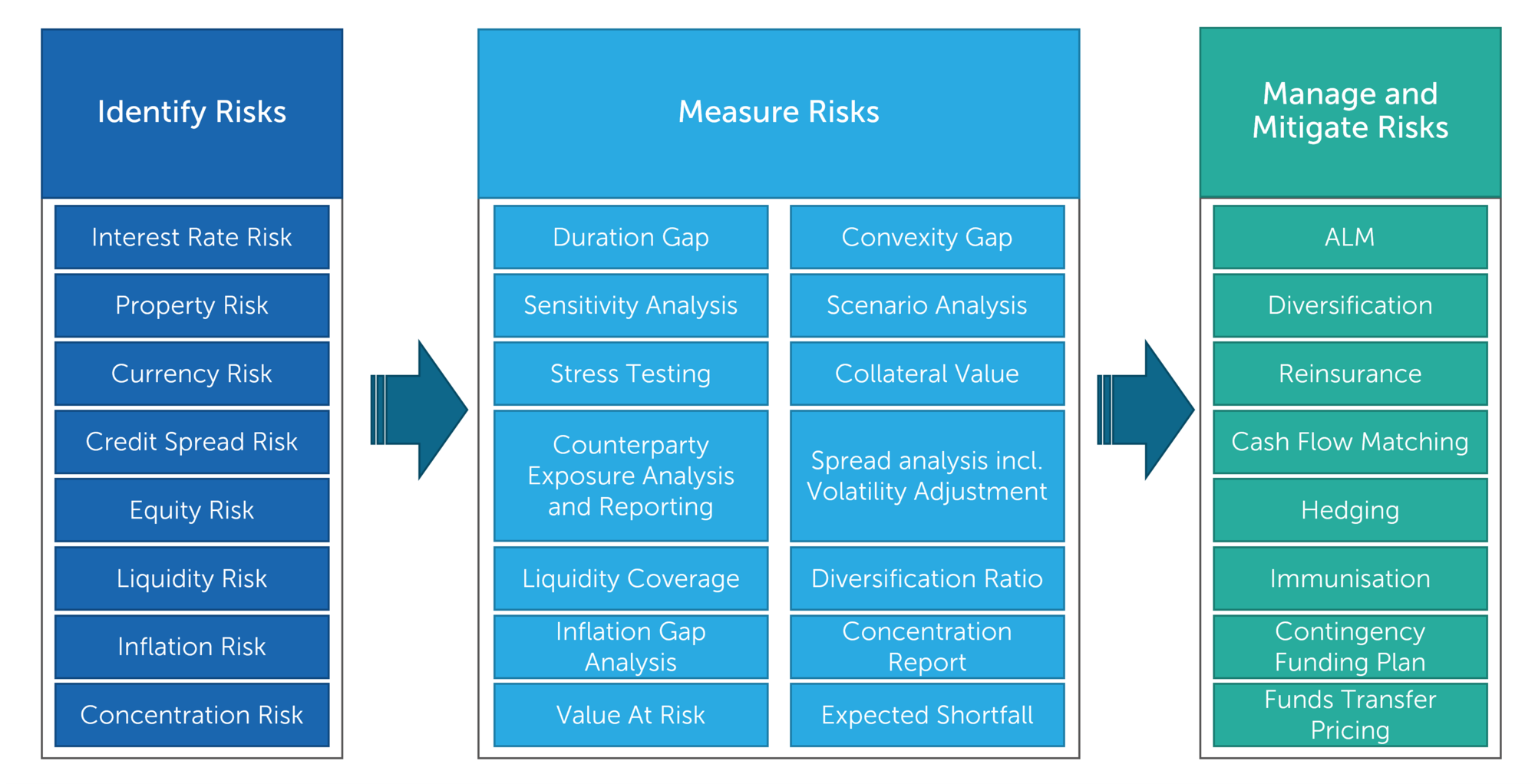

Identify Market Risks

Comprehensive identification of all relevant market risks on your balance sheet and integration into your risk register.

Measure Market Risk

Centralize market risks and ensure that nothing is unaccounted for.

Create or optimise risk measurement calculations for market risks such as DV01 and CS01 (incl. volatility adjustment).

Mitigate, Manage, and Report Market Risk

Implement strategies to mitigate or manage market risk (e.g., duration matching, hedging strategies, liability-driven investing), and ensure risks are within limits through regular risk monitoring and reporting.

Capital Measurement and Optimisation

Measure market risk impacts on SCR and Economic Capital, and reduce the capital required through ALM optimization.

Manage and Optimise Liquidity Risks

Optimise liquidity through Fund Transfer Pricing and Minimising Cash Drag.

Ensure sufficient liquidity is held for collateral or margin calls by managing, monitoring, and reporting on liquidity ratios.

Implement software, solutions, and tools

Support with the implementation of tools and software solutions such as SAS, FIS, and AXIS to manage and report on market and liquidity risks.

How does it work in practice?

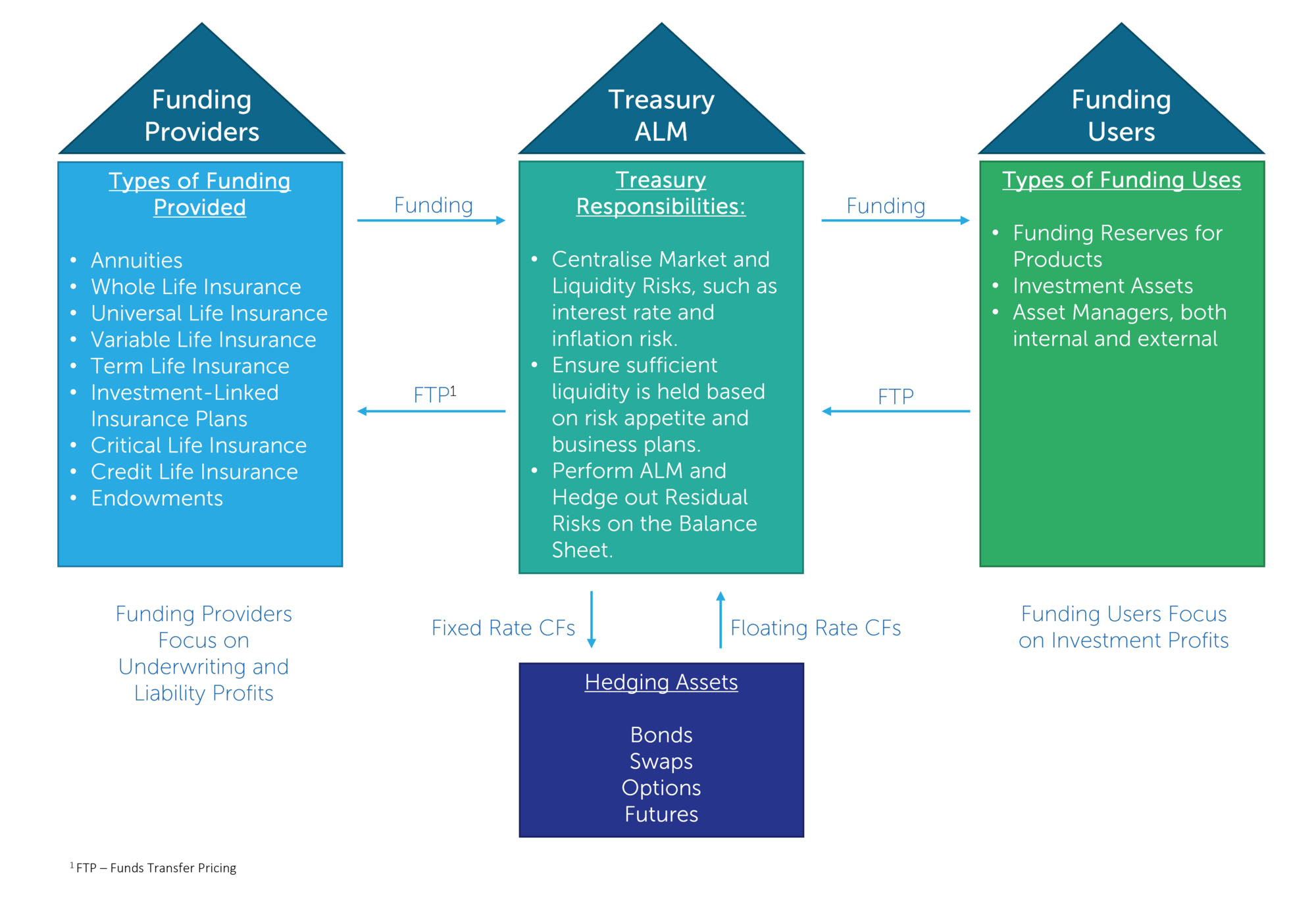

RISK MANAGEMENT FRAMEWORK FOR MARKET AND LIQUIDITY RISK

MARKET AND LIQUIDITY RISK MANAGEMENT FOR CENTRALISED TREASURY

Key Features

- Finalyse provides a comprehensive solution for market and liquidity risk management, including identification, measurement, management, mitigation, and forecasting.

- Finalyse provides expertise in the following areas:

- Capital measurement and optimization

- Identification, measurement, and management of market risks

- Management and optimization of liquidity and liquidity risks

- Operationalising funds transfer pricing

- Establishment and optimisation of funding plans

- Finalyse will leverage its interdisciplinary expertise in ALM, market, liquidity and credit risks, as well as its experience consulting to banks and insurers and reinsurers, to deliver world-class solutions.

- Finalyse can support you in specific areas or throughout the entire market risk management life cycle.

Frans is an actuary and Financial Risk Manager with international experience in the pensions and insurance sectors. He has been specialising in actuarial valuations (AXIS), financial and regulatory reporting (IAS19, US GAAP, IFRS2, IFRS17), regulatory reporting (IORP II, Solvency II, ICS, BMA), market risk management (ALM, SAA), climate change risk management and investment consulting.

François-Xavier is a Principal Consultant with advanced expertise in Financial Markets, ALM and Risk Management, covering both banks and insurance companies. On the banking side, François-Xavier is a practice leader on Valuation, IRRBB, FRTB, VaR, Initial Margin and Counterparty Risk, well acquainted with the regulatory requirements and the market practices surrounding market risks. On the insurance side, François-Xavier has extended experience in the regulatory treatment of financial instruments, ORSA, and hedging balance sheets against interest rate, credit spread and inflation risks.

Yoyo is a Qualified FASSA and AAG Actuary, and Chartered Enterprise Risk Actuary (CERA) with close to 10 years of experience. His experience is in ALM, Market and Liquidity Risk, and automation. With Power BI, R, SQL and Python, he works on developing Finalyse ‘s internal SCR calculation, and automates roughly 7000 Finalyse Valuation Services (FVS) structured product calculations.

Sankesh Jain is a nearly qualified actuary with expertise in actuarial reporting and actuarial model modernization within life insurance along with diverse experience in pensions, and regulatory reporting. He specializes in Solvency II and IFRS 17 modelling, reserving, and capital calculations. Skilled in tools such as Excel, VBA, SQL and Python, he supports actuarial valuations, stress testing, and risk reporting. His experience spans actuarial controls, governance, and pension advisory, supported by a strong academic background in quantitative finance and statistics.

Client Cases

Finalyse did a fantastic job validating our scorecards and developing our master scales—exactly what we expected from them. The collaboration with Nemanja and Prashant was excellent throughout the entire process, and the knowledge transfer was particularly valuable, enabling our teams to carry out future analyses independently. Finalyse’s contribution was crucial in helping BIO take its risk management to the next level.

Denis Pomikala,

Head of Risk Management

-

Review of the market risk stress testing framework for a major Belgian bank

The Middle Office department wanted to investigate a method to enrich the stress testing canvas, through a more robust identification and quantification of the risk factors of interest; and by adding a reverse stress testing component to the existing framework. Finally, Finalyse provided the client with an in-depth "Stress Test Review" document including:

- A definition of the risk factor sensitivities which had to be consistent with the reverse stress-testing protocol

- An analysis of the dependencies between risk factors in order to establish a stress-testing protocol with a gradually increasing level of complexity.

-

This project enabled the client to have a clear and comprehensive analysis of the pre-existing and new "Stress Test" frameworks, to close the gap between those two in accordance with the audit and regulator's recommendations.

Moreover, the institution now has a well-documented process and prototype, which constitute a solid but flexible basis for further work, improvement, or adjustments regarding anything related to Stress Tests and Reverse Stress Tests.