How Finalyse can help

Agile and comprehensive assessment, measurement and management of your market and liquidity risks

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Helping you comply with the Solvency II regulations as well as optimising your Solvency II balance sheet

Contents of a Recovery Plan: What European Insurers Can Learn From the Irish Experience (Part 2 of 2)

Gary is a Principal Consultant within our insurance practice in Dublin. He has 16 years of experience within the life and non-life (re)insurance sectors covering industry, audit and consultancy roles. His expertise covers financial reporting, prudential and conduct risk management, and assurance activities. Gary has provided outsourced actuarial, risk, compliance, and internal audit function services for a wider range of insurers, reinsurers and captives.

In April 2025, the European Insurance and Occupational Pensions Authority (EIOPA) (‘EIOPA’) presented its draft regulatory technical standards (‘RTS’), in the form of a consultation paper (EIOPA-BoS-25-097), to specify its expectations for contents of pre-emptive recovery plans. This consultation comes in advance of the introduction of the Insurance Recovery & Resolution Directive (‘IRRD’). Recovery planning is not a new concept for all (re)insurers in Europe, however. In 2021, the Central Bank of Ireland (‘CBI’) marked the introduction of recovery planning regulations for Irish domiciled (re)insurers by publishing their document 'Recovery Plan Guidelines for (Re)Insurers'.

This is the second article in a two-part series which compares the EIOPA and CBI regimes, highlighting how European insurers can learn from the Irish experience while also examining differences between the two frameworks. Part 1 of the article can be found here.

In Part 2, we consider:

- The Range and Severity of Remedial Actions

- Impact, Credibility and Feasibility of Remedial Actions

- Scenario Analysis

- Compatibility of Remedial Actions

- Communications

- Past SCR Breaches.

Range and Severity of Remedial Actions

Both papers include extensive requirements around remedial actions, or 'recovery options' as they are referred to by the CBI.

Article 6(1) of the RTS and Section 5.8 of the CBI document outline common objectives. Recovery plans shall set out a range of actions designed to respond to severe macroeconomic and financial stress scenarios. The impact, credibility and feasibility of each remedial action should be considered.

The RTS explicitly states that the recovery plan document shall follow a uniform structure when presenting the information for each remedial action.

RTS Article 6(2) and CBI Section 5.8 contain near identical wording stating that remedial actions shall include both measures extraordinary in nature as well as those that could also be taken in the course of the normal business.

Article 6(3) of the RTS calls for inclusion of a range of actions that could:

- restore recapitalisation;

- ensure adequate access to liquidity;

- reduce the insurance or reinsurance risk profile and related Solvency Capital Requirement; or

- achieve a voluntary restructuring of liabilities, without triggering default or downgrade.

Section 5.8(4) of the CBI paper includes similar wording while also obliging insurers to consider alternative actions if group support is not forthcoming in each scenario.

Remedial Actions: Impact, Credibility and Feasibility

Both regimes require that each remedial action is individually listed and assessed.

Article 6(3) of the RTS and Section 5.8 of the CBI Guidelines overlap in several respects:

- A description of the financial and operational impacts on solvency, liquidity, capital composition, and operations are required.

- There is also a requirement to assess the impact on other stakeholders such as shareholders, policyholders, and counterparties.

- The feasibility assessment should consider all risks associated with implementing remedial measures, including impacts on policyholder behaviour. It should also reference any past experience the insurer has in implementing similar measures.

- The analysis of material impediments to the effective and timely execution should include legal, regulatory, operational, business, financial, macroeconomic and reputational risks.

- Where material impediments are identified, potential solutions are also expected to be discussed.

- Continuity of operations must be analysed in respect of each remedial action.

- The expected time frame for the implementation and effectiveness of each action should be documented.

While both regimes bear a high degree of similarity, the CBI guidance makes more explicit reference to considering both short- and long-term implications for each option. It also specifically mentions justification of any valuation assumptions made for the purpose of the impact assessment.

Scenario Analysis

EIOPA’s RTS requires consideration as to what remedial actions may be appropriate in a specific scenario. Similar to the CBI Guidance, it also refers to systemic and idiosyncratic events. Both regimes call for consideration of the effectiveness of remedial actions, and appropriateness of recovery indicators, under a range of severe macroeconomic and financial stresses, relevant to the insurer’s specific risk profile.

Section 5.9 of the CBI document however, offers far more detailed guidance on the scenario analysis expected:

- Scenarios should be calibrated to simulate events that would threaten failure of the insurer.

- Scenarios considered should include both slow-moving and fast-moving events.

- Reverse stress tests from the ORSA could be considered as a starting point for developing scenarios that are ‘near-default’.

- The analysis of each scenario should consider which recovery indicators would be triggered and when.

- The insurer should seek to identify the point at which entering solvent run-off is the most appropriate option.

- The overall recovery capacity under each scenario should be analysed (see next section).

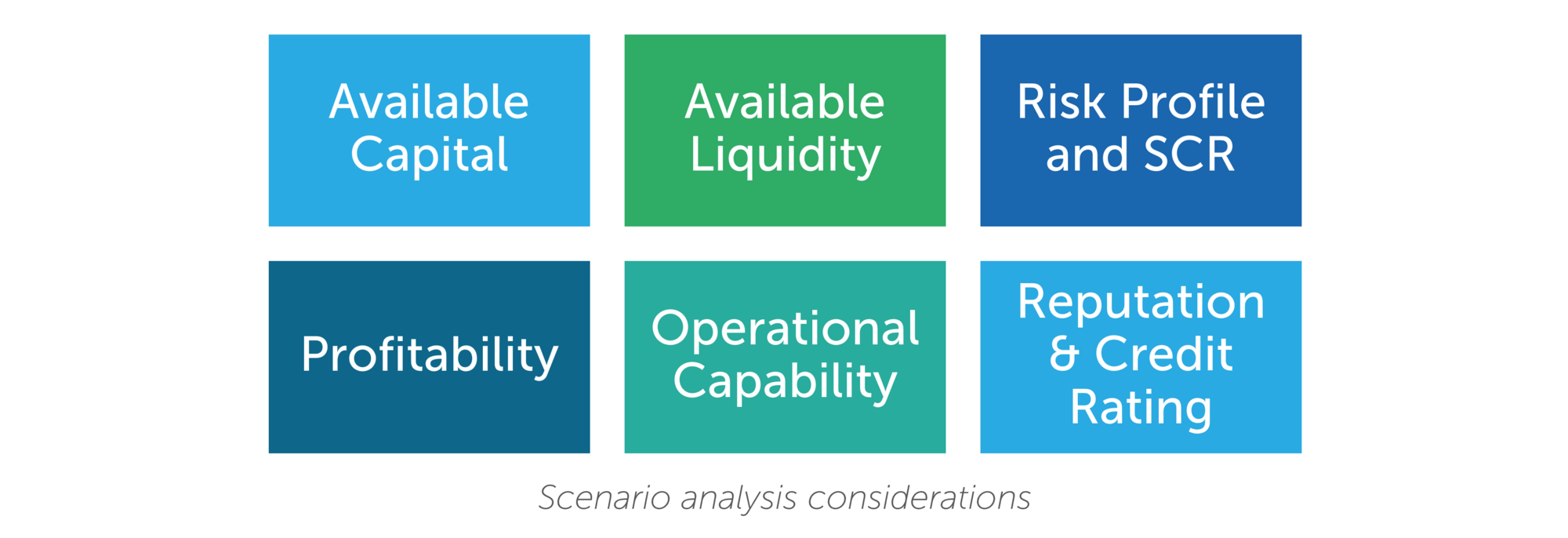

The CBI guidance also sets out that analysis of each scenario should include the impact of the following:

- available capital;

- available liquidity;

- risk profile and SCR;

- profitability;

- operational capability (including claims payment, policy administration and investment settlement operations); and

- reputation and credit rating.

The proposed European requirements, in contrast, are more prescriptive with respect to the explicit requirement to consider availability of management information under stressed conditions. Insurers must ensure that information necessary for the implementation of remedial actions remains available for decision-making in a reliable and timely way.

Compatibility of Remedial Actions (Overall Recovery Capacity)

Article 6(4) of the RTS requires an assessment of compatibility of remedial actions that could be implemented in the same period of time. The CBI’s paper has coined the term ‘Overall Recovery Capacity’ which explores the aggregate impact of multiple remedial actions being deployed simultaneously, taking into account mutual exclusivity or compatibility of actions in each scenario.

Communications

Both regimes require similar information regarding communication and disclosures as outlined in Article 7 of the RTS and Section 5.10 of the CBI Guidance. The communication strategy shall cover both internal and external communications.

The RTS prescribes the requirements for a tailored communication strategy that recognises different communication needs depending on the stress scenario and the remedial actions being implemented.

The CBI document again includes more specific points for consideration, including:

- timing of communications;

- frequency of communications;

- contact details;

- roles and responsibilities of specific people for communications;

- legal responsibilities in relation to disclosure and confidentiality;

- proposals for managing any potential negative market reactions; and

- any specific communication needs for individual recovery options.

In contrast, IRRD is more prescriptive than the CBI document regarding the obligation to establish adequate procedures for keeping supervisory authorities notified of an emerging stress scenario and for sharing plans on the remedial actions contemplated.

Past SCR Breaches

Article 8 of IRRD includes a unique obligation not explicitly required under the CBI’s regime: If SCR has been breached at some point in the last ten years, the recovery plan shall include an assessment of the measures taken to restore the undertaking’s compliance.

Summary and Next Steps

While different terminologies may be used, both European and Irish regulations bear great similarities around recovery planning expectations. The Irish requirements are more prescriptive in some places, though such prescription can offer useful guidance for those drawing up recovery plans for the first time.

In scope European insurers, that do not yet have recovery plans in place, can draw valuable lessons from the Irish experience ahead of the 2027 effective date of IRRD. Meanwhile, those who already have existing recovery plans shall be required to conduct a gap analysis, ensuring they can adapt to become compliant with new regulations.

How Finalyse Can Help

- Recovery Plan Workshops – Suitable for insurers new to recovery planning, our experienced team provides comprehensive training and a roadmap for recovery planning success.

- IRRD Gap Analysis – Ideal for insurers already operating under a recovery planning regime, our experts support on closing the gap to achieving compliance with the upcoming implementation of IRRD across Europe.

- Industry Benchmarking – Assessing the quality of insurers’ recovery plans relative to their peer groups, plus analysis of lessons learned from regulatory feedback in existing regimes.

- Recovery Indicator Calibration – Support in selection and quantitative calibration of a suite of recovery indicators that are appropriate relative to the insurer's specific risk profile and risk management framework.

- Scenario and Stress Testing – Designing severe but plausible stress scenarios, leveraging upon the firm’s existing ORSA framework, where appropriate.

- Remedial Action Evaluation – Analysing the impact, credibility and feasibility of a range of remedial actions, benchmarking against peer groups and regulatory expectations.

Please reach out to one of our experienced Finalyse consultants at insurance@finalyse.com for more information.

Frequently Asked Questions

A pre-emptive recovery plan is designed to help insurers prepare for severe financial stress by outlining actionable steps to restore financial stability while remaining solvent. Both the IRRD (via EIOPA) and the Central Bank of Ireland (CBI) frameworks aim to ensure that insurers can respond promptly to emerging risks through predefined indicators, governance procedures, and recovery options. These plans are not only regulatory obligations but also serve as practical tools for strengthening operational resilience.

While both EIOPA and the CBI require broadly similar elements - such as recovery indicators, governance frameworks, and summary sections - the CBI guidelines are generally more prescriptive. For instance, the CBI specifies categories of indicators (e.g., solvency, liquidity, profitability) and requires detailed rationales for indicator selection. EIOPA, by contrast, adopts a more principles-based approach, allowing for flexibility but also placing more onus on insurers to justify their methodologies.

Ireland’s earlier implementation of recovery planning regulations has provided valuable clarity and precedent for what robust plans look like in practice. The CBI’s prescriptive approach offers insurers concrete examples and expectations - especially helpful for firms preparing recovery plans for the first time under the upcoming IRRD. By studying the Irish framework, insurers can better understand regulatory expectations, avoid common pitfalls, and build plans that are both compliant and operationally effective.

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Trending Services

Risk Data Analyser

#Regtech

#DigitalTransformation

Risk Appetite Framework for Insurance

#RiskAppetite

#InsuranceRisk

IFRS 17 implementation

#IFRS17

#InsuranceAccounting

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Trending Services

AI Fairness Assessment

#ResponsibleAI

#AIFairnessAssessment

CRR3 Validation Toolkit

#CRR3Validation

#RWAStandardizedApproach

FRTB

#FRTBCompliance

#MarketRiskManagement

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Trending Services

Independent valuation of OTC and structured products

#IndependentValuation

#StructuredProductsValuation

Value at Risk (VaR) Calculation Service

#VaRCalculation

#RiskManagementOutsourcing

EMIR and SFTR Reporting Services

#EMIRSFTRReporting

#SecuritiesFinancingRegulation

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Blog

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

Regulatory Brief

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Materials

Read Finalyse whitepapers and research materials on trending subjects

Latest Blog Articles

Contents of a Recovery Plan: What European Insurers Can Learn From the Irish Experience (Part 2 of 2)

Contents of a Recovery Plan: What European Insurers Can Learn From the Irish Experience (Part 1 of 2)

Rethinking 'Risk-Free': Managing the Hidden Risks in Long- and Short-Term Insurance Liabilities

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Our Team

Get to know our diverse and multicultural teams, committed to bring new ideas

Why Finalyse

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Career Path

Discover our three business lines and the expert teams delivering smart, reliable support