Maël Kerbaul is a Senior Consultant with over 15 years of experience in the banking and financial industry, especially in risk management. His main area of expertise lies in the credit risk management and regulatory capital calculation. He has developed a broad knowledge of Basel IV/CRR3 while he played a major role in the impact assessment of this new regulation at a large financial institution in Belgium. Maël has also a wide experience in data analysis for credit risk and has a good command of SAS EG and SQL.

Although overall securitisation volumes in the European Union remain relatively modest and well below their 2008 peak, one segment has experienced notable growth in recent years: transactions designed to achieve Significant Risk Transfer (SRT) and risk-weighted asset (RWA) reduction. In 2024, approximately 70 banks issued SRT securitisations in Europe, representing a total exposure of more than €200 billion.

The scope of asset classes included in SRT structures has also expanded. While these transactions were historically concentrated in corporate and SME loan portfolios, SRTs now increasingly involve residential mortgage loans, auto loans, and even green or ESG-linked assets.

This growth has been supported by recent regulatory developments, notably the 2021 extension of the Simple, Transparent and Standardised (STS) framework to synthetic securitisations — which account for the vast majority of SRT activity. Moreover, the rise in RWAs resulting from the implementation of CRR3 has strengthened banks’ incentives to use securitisation to ease capital constraints.

SRT securitisation is a powerful instrument for banks to free up capital and increase their lending capacity. EU policymakers clearly recognize the benefits of securitisation in enhancing the funding of the real economy and, in the context of growing investment needs for defence and green transition, have recently acknowledged the need to reform the 2019 EU Securitisation framework towards more attractive, less burdensome rules to revitalize the securitisation market (as underlined, e.g., in the 2024 Draghi Report on EU Competitiveness).

SRT securitisation efficiency might increase further with the upcoming recalibration of capital requirements planned by the European Commission, which is expected to include a reduction of the p-factor and of the risk-weight floors. While awaiting these reforms, this article will describe how SRT securitisation allows risk transfers and provides regulatory capital relieves from the perspective of an originating bank.

Similar to other forms of securitisation, SRT transactions involve pooling financial assets and structuring the resulting portfolio into several tranches with varying levels of seniority and risk. Some or all of these tranches are then placed with investors such as insurance companies, asset managers, or other banks seeking new sources of yield and greater portfolio diversification across asset classes or geographies that would otherwise be difficult to access.

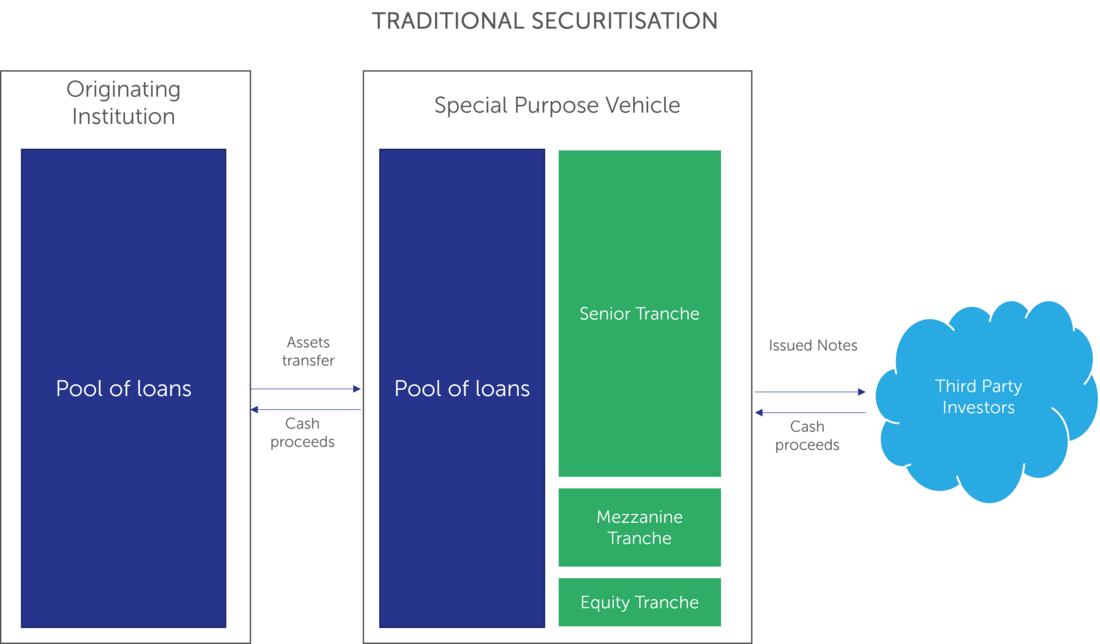

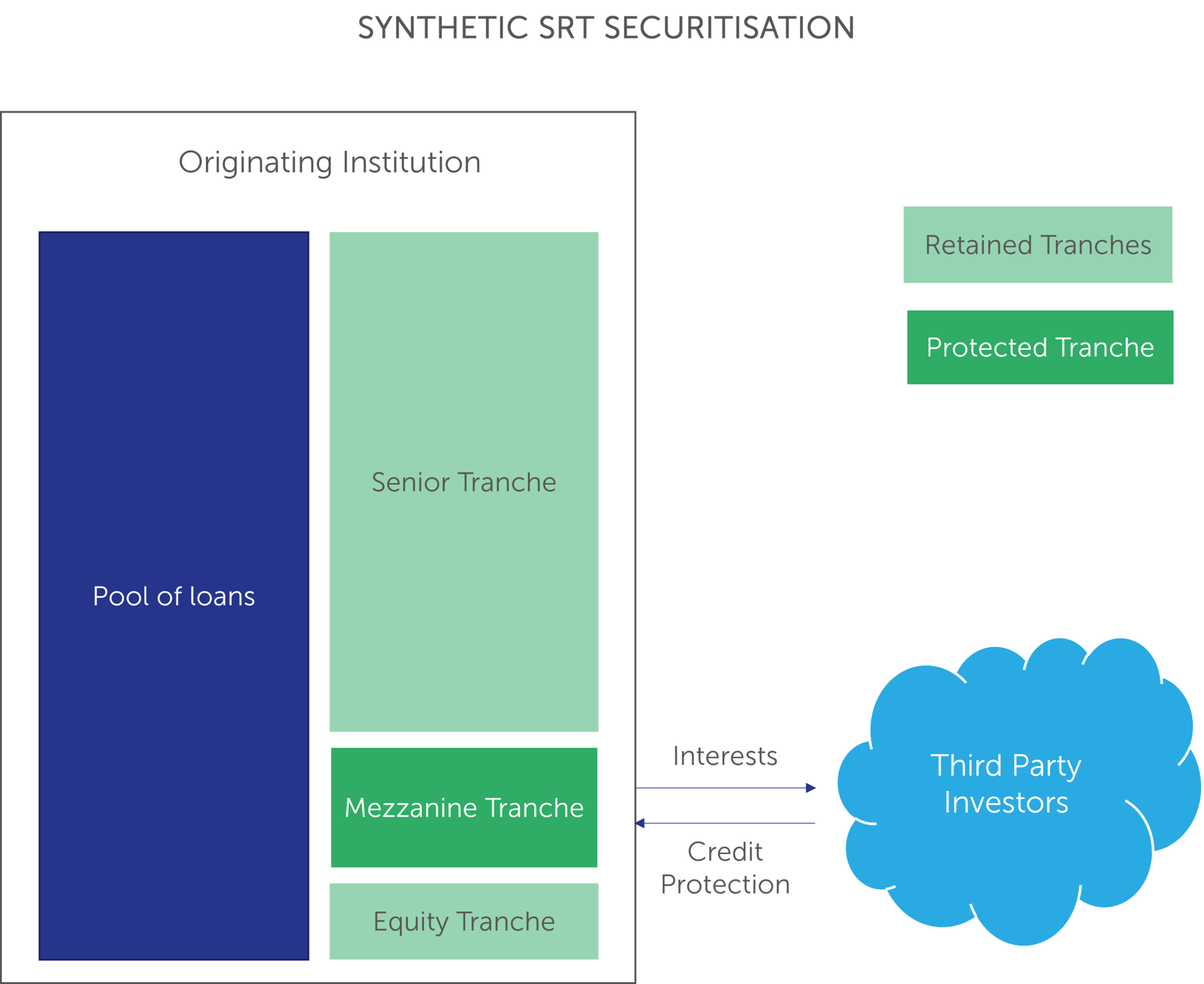

In a traditional securitisation, risk transfer is achieved through the sale of the underlying exposures to a Special Purpose Vehicle (SPV), which issues notes to investors. By contrast, more than 90% of SRT transactions are structured as synthetic securitisations - also referred to as on-balance-sheet securitisations. These are generally easier and more cost-effective to arrange, as they do not require the creation of an SPV. The underlying assets remain on the balance sheet of the originating institution, while credit protection - typically provided through a credit derivative or a financial guarantee - is purchased from investors to cover losses on the transferred tranche(s).

The figure below illustrates a standard SRT structure in which a mezzanine tranche is protected, while the senior tranche is retained by the originating bank. An equity tranche covering the expected loss of the underlying portfolio is also typically retained by the originator in order to reduce the overall cost of protection.

In order to obtain RWA relief, a securitisation transaction must comply with the requirements set out in articles 244 (traditional securitisation) and 245 (synthetic securitisation) of Regulation EU 575/2013 (the Capital Requirement Regulation, CRR). These provisions establish quantitative tests for assessing the significance of the risk transfer, as well as specific constraints on the structural features of the transaction and, in the case of synthetic securitisation, of the nature of the credit protection.

A risk transfer is deemed significant when it meets either of the following conditions:

For traditional securitisations, the transfer of the underlying exposures to an SPV must be genuine, with no material clawback provisions and no retained control by the originator.

In the event of credit deterioration, the originator must have no obligation to improve the quality of the underlying pool or to increase the yield payable to investors.

A clean-up call option may be exercised solely at the discretion of the originator, and only when 10% or less of the original value of the underlying exposures remains unamortised. The call must not be structured in a way to avoid allocating losses to the investors.

In synthetic transactions, the credit protection must qualify as an eligible credit risk mitigant for securitisation positions under Article 249 of the CRR. Funded credit protection is limited to financial collateral. The protection agreement must not include materiality thresholds or termination clauses that could allow cancellation due to credit quality deterioration.

When the conditions outlined above are met, the originating institution may apply the specific RWA calculation methodology set out in Article 247 of the CRR. In this case, the underlying exposures are excluded from the calculation of RWAs and expected losses. Instead, RWAs are determined at the level of the tranches retained by the originator. Where the bank retains different tranches, either fully or partially, each retained tranche is treated as a distinct exposure, and the corresponding RWA is calculated separately.

The originating institution may also opt to deduct its securitisation positions from its own funds, which is often advantageous for first-loss tranches otherwise subject to a 1.250% risk weight. Tranches whose credit risk has been transferred to third-party investors are excluded from the RWA calculation of the originator.

As a result of the SRT, the originating institution benefits from a significant reduction in its total RWAs. The RWA relief can be measured as the difference between the RWAs of the underlying portfolio prior to securitisation and those of the retained tranches. The capital cost associated with deducted positions may also be considered when determining the overall capital relief achieved.

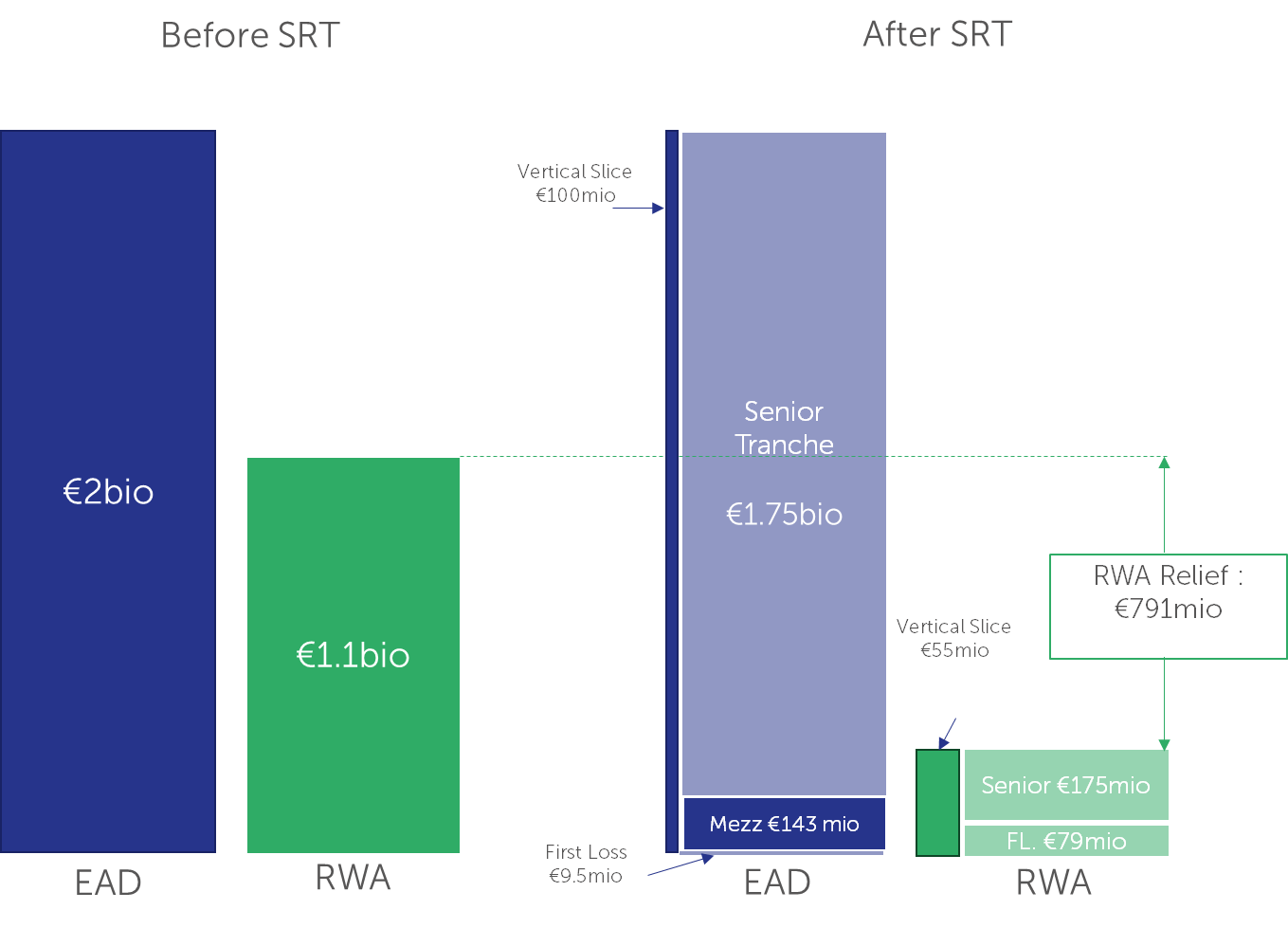

Let’s consider an example in which Bank A issues an SRT transaction backed by a €2 billion pool of SME loans. The bank applies IRBA to this portfolio, with its internal models producing an average risk weight of 55%. Accordingly, the portfolio generates €1.1 billion in RWAs before securitisation.

As part of the securitisation, the bank divides the portfolio risk into three tranches: a senior tranche representing 92% of the securitised exposure, a mezzanine tranche representing 7.5%, and a first-loss tranche representing 0.5%. The bank also retains a vertical slice of 5% of the underlying portfolio in order to comply with the retention requirement.

After securitisation, the RWA are no longer calculated at the level of the underlying loans – except for the 5% vertical slice, but instead at the level of each tranche.

For the senior tranche, considering that the securitisation meets the STS criteria, the minimum 10% risk-weight floor must be achieved through appropriate structural optimisation.

The mezzanine tranche is fully protected by a credit protection via third-party investors, consequently, no RWAs are borne by the originating institution.

The first-loss tranche exposure of 0.5% (€9.5 million) is deducted from regulatory capital. To estimate the RWA equivalent, this amount may be divided by the bank’s capital-to-RWA ratio — assuming 12% for a G-SIB, this yields approximately €79 million. This example illustrates that capital deduction may be more beneficial than applying a 1,250% risk weight, which would result in €119 million of RWAs.

The retained part of loans within the 5% vertical slice is still risk-weighted as if it was not securitised, that is subject to a 55% risk-weight.

Thanks to this SRT transaction Bank A benefits from a €791 million RWA relief.

Finalyse specialises in guiding financial institutions through the complex landscape of SRT transactions, offering end-to-end support from feasibility assessments to operational implementation. Whether you're pursuing synthetic securitisations, credit risk mitigation, or regulatory capital relief, our team brings the technical knowledge and market insight necessary to deliver successful outcomes.

At Finalyse, we have engaged with bulge-bracket banks in Europe to support their SRT journey with our proprietary solutions. We have also worked with leading vendors for regulatory capital calculations for SRT.

Our consultants bring hands-on experience across regulatory, risk, and operational dimensions of SRT, enabling institutions to move from concept to execution with confidence.

Reach out to Finalyse at banking@finalyse.com for a demo or initial consultation.

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support