Securitisation & SRT Support

In a tightening regulatory environment, Significant Risk Transfer (SRT) transactions are an essential tool for European banks to optimize capital, manage risk, and increase lending capacity. Our specialized services help you originate, structure, and execute SRT transactions that comply fully with the EU Capital Requirements Regulation (CRR) and align with your strategic goals for balance sheet and capital optimisation.

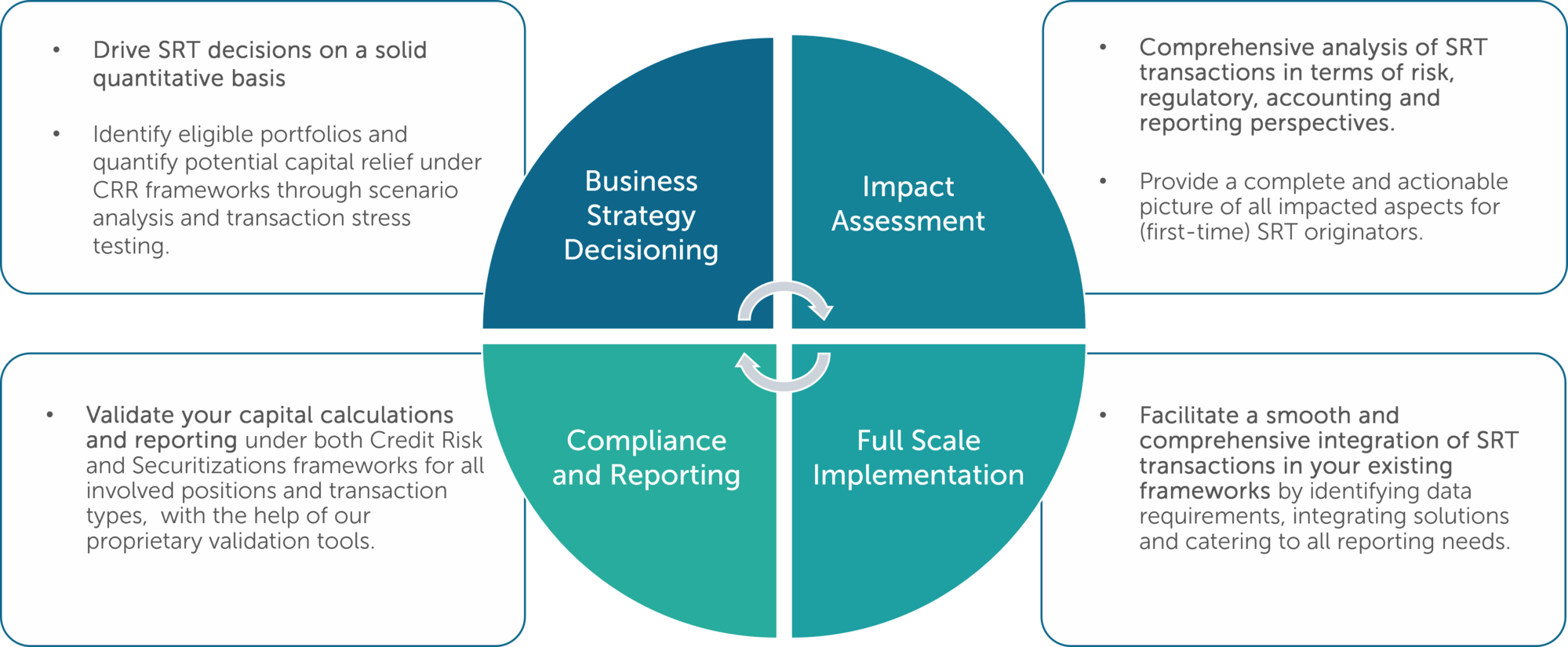

How does Finalyse address your challenges?

Feasibility Analysis

Identify eligible portfolios and assess SRT viability based on regulatory and economic factors.

Transaction Structuring

Quantitative support for synthetic securitisation structuring that aligns with your capital, risk, and strategic objectives.

Regulatory & Supervisory Support

Navigate EBA Guidelines, ECB requirements, and local supervisory reviews with confidence and clarity.

End to End SRT Implementation

From data gap analysis to reporting requirements. Process Tranche and Deal level information and translate retention policies to correct RWA treatments.

Capital calculations validation

Validate pre- and post-SRT RWA calculations of all related positions by leveraging Finalyse’s internal toolkit.

Cover Reporting needs

Both regulatory reporting (COREP) as well as internal dashboarding of the SRT performance: Tranche evolution, Cost and Capital Relief, Amortisation and Losses.

How does it work in practice?

We specialise in guiding financial institutions through the complex landscape of SRT transactions, offering end-to-end support from feasibility assessments to operational implementation. Whether you're pursuing synthetic securitisations, credit risk mitigation, or regulatory capital relief, our team brings the technical knowledge and market insight necessary to deliver successful outcomes.

Prior Experiences

Our team has successfully supported a range of European banking clients with their impactful SRT transactions, including:

Major bank in EU:

Ongoing structural implementation of the bank’s originated SRTs and investor securitisation portfolio in its regulatory capital solution. Involved in the setup of complex structured products applying exposure-level vertical slicing to underlying portfolio. Addressing several complex regulatory topics for Securitisations pertaining to CRR Articles 244 to 270 and setup of securitisation deals via SPVs with irrevocable credit facilities.

European MDB:

Performed a full validation of RWA calculation engine (Moody’s RAY) pertaining to Securitisations framework among other topics such as equity investment in funds (CIUs) and SA-CCR calculations. Focus on multiple regulatory intricacies linked to the investment bank’s highly specialized portfolio entailing structured products and exotic derivatives.

Development of a client tailored simulation/validation tool for the Securitisations Framework to assist internal validation team for testing RAY upgrades.

Retail bank in Benelux region:

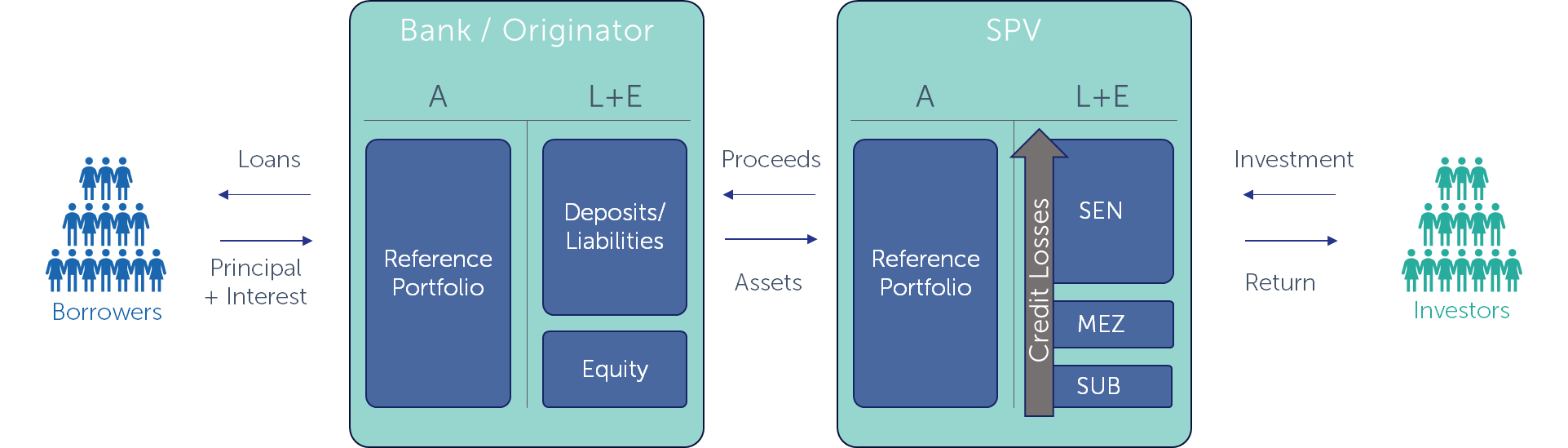

Quantitative modelling of the bank’s first SRT transaction, focusing on both the asset side (i.e., the underlying mortgage pool) and the liability side (i.e., the issued CLNs and retained synthetic tranches). Providing a comprehensive analysis of the transaction structure from a risk, regulatory and reporting perspective, highlighting the expected impacts on the bank.

Key Features

- Expert support on transaction setups for:

- Any role of involvement as Originator, Sponsor, Original Lender or Investor.

- Any type of transaction: Traditional or Synthetic, STS or non-STS, ABCP or NPE transactions.

- Any type of underlying portfolio: Retail or non-Retail, revolving facilities, Performing or NPE, Re-securitisations.

- Facilitating implementation every step of the way:

- Sourcing – ETL mapping, data quality etc.

- Calculations – RWA calculation implementation & validation

- Reporting – COREP reporting (C13, C14) and other downstream applications

Abishek Chopra is a seasoned Risk Management professional with over 12 years of experience in multiple areas of credit risk, especially on CRR and Basel guidelines. He has expertise in addressing complex regulatory topics such as credit risk mitigation for RWA optimization of different asset classes, Basel IV application of Whole Loan/Split Loan approaches for mortgages, SA-CCR and Securitisation.

Nathan Desmidt is a Managing Consultant with more than 8 years of experience in risk management. Nathan’s area of expertise lies within regulatory capital calculations, specifically in the context of CRR2/CRD5 and upcoming Basel 4/CRR3 regulations. Recently Nathan has been involved in the implementation of a new RWA calculator at a large financial institution aiming to enable Basel 4 compliancy, focusing on validation of RWA calculations in light of the new framework’s developments.