David Boavida is a senior consultant with extensive experience in modelling and managing Market and Liquidity Risk and a solid foundation in Asset and Liability Management (ALM). In particular, his main areas of expertise lie within IRRBB & CSRBB. His technical skills cover a range of multi-purpose programming languages, including Python, R and MATLAB. David also has comprehensive knowledge and experience in Basel III Regulatory Reporting, Liquidity and Funding Risks and Stress Testing.

The revised Capital Requirements Directive (CRD V) and Regulation (CRR 2) make up the second phase of the implementation of the Basel Committee on Banking Supervision (BCBS) Standards published in April 2016 (BCBS 368) within the EU.

19th July 2018, well ahead of the application of CRD V and CRR2 on 28th June 2021, the European Banking Authority (EBA) published its Guidelines of the Management of Interest Rate Risk Arising from non-Trading Book Activities (EBA/GL/2018/02). These followed the BCBS 368 and provided the initiative for the first phase of its implementation within the EU. However, the EBA acknowledged that these guidelines would be updated in the following years to reflect the revisions of the CRD and CRR.

More specifically, Article 84 of the CRD V mandates EBA to issue guidelines to specify the criteria for the identification, management and mitigation by institutions of the interest rate risks in the banking book (IRRBB), as well as the criteria for the evaluation by an institution’s internal system of the IRRBB and to determine if those internal systems are not satisfactory. Additionally, the EBA was requested to issue guidelines to specify the criteria for the assessment and monitoring of the credit spread risk in the banking book (CSRBB). Finally, the CRD V also mandates EBA to complement the guidelines with regulatory technical standards (RTS) specifying a standardised methodology for evaluating IRRBB.

To that effect the EBA published three consultation papers early December 2021. These include the guidelines on IRRBB and CSRBB, the regulatory technical standards (RTS) on the supervisory outlier test (SOT) and the RTS on the standardised approach (SA) and the simplified standardised approach (S-SA) for the economic value of equity (EVE) and the net interest income (NII). The consultation period lasted for four months and finished on the 4th of April 2022.

Figure 1: The 3 consultation papers together with the ITS on IRRBB Disclosure (EBA/ITS/2021/07) published in November 2021 represent the conclusion of the implementation of the BCBS 368 within the EU.

The guidelines on IRRBB - generally maintain continuity to the EBA/GL/2018/02 but introduce new elements. The EBA proposes a five-year cap to the repricing maturity of non-maturing deposits (NMDs) from non-financial customers and introduces criteria to identify non-satisfactory IRRBB internal management systems (IMS). Also, there is a proposal for a consistent determination of NII, including interest income, interest expenses and market value changes.

IRRBB SOT – The RTS give continuation to the provisions embodied on the EBA/GL/2018/02 regarding the SOT on EVE by including additional specifications and introduces the SOT on NII. Hence, taking into account its mandate in the Article 98(5a) of the CRD, the EBA provides a definition and calibration of the large decline for the SOT on EVE and on NII.

IRRBB SA & S-SA – The RTS specify the standardised and simplified standardised approaches/ methodologies for the EVE and NII, where the S-SA focus on small and non-complex institutions (SNCI).

The crucial innovation present in the latest consultation is the considerable expansion of the requirements for the management of the CSRBB. Until recently, the regulatory framework and banks have given noticeably more emphasis to the IRRBB management. The BCBS 368 explicitly focused on IRRBB and only defined CSRBB. The EBA/GL/2018/02 also presented a definition of the CSRBB and stated that institutions “should monitor and assess their CSRBB-affected exposures” whilst weighting -in its materiality for their risk profile. This vague definition of requirements has been a contributing factor for the management of CSRBB being somewhat overlooked by the banks.

However, the Article 84(5) of the CRD V, mandates EBA to issue guidelines to specify the criteria for the assessment and monitoring by institutions of the risks referred to in paragraph 2, which addresses “risks arising from potential changes in credit spreads that affect both the economic value of equity and the net interest income of an institution’s non-trading book activities”.

Thus, there clearly is a regulatory pressure for the assessment and monitoring of CSRBB. Also, due to the low-interest rate environment of the past few years, some institutions have turned to securities and bonds to generate higher levels of income.

In the following chapters we present an overview of the guidelines on CSRBB and develop on the topic of the methodology for the monitoring and assessment of CSRBB.

As regards IRRBB, the draft guidelines represent a mere expansion to the previous regulatory framework. However, they greatly contribute towards CSRBB requirements, which have been significantly expanded.

Overall, the requirements on CSRBB follow those on IRRBB. There is a high degree of alignment with respect to governance and strategy aspects, where general expectations regarding the risk assessment framework and responsibilities, as well as the features on the risk policies, processes and controls are outlined. Even though there are still some differences in the latter aspects, the most significant distinction concerns the fewer requirements regarding methodology as well as the absence of any setting of specific internal limits.

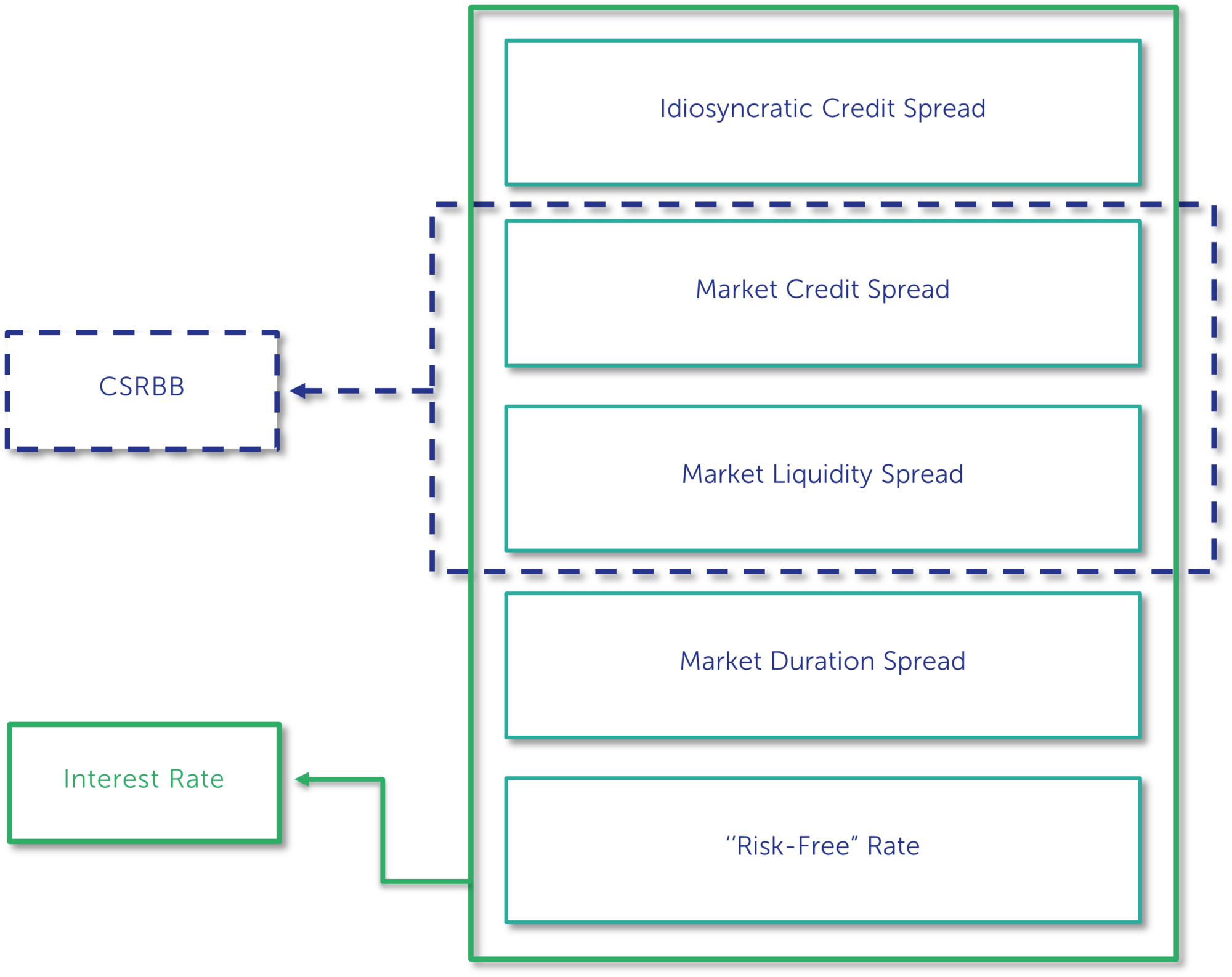

CSRBB relates to the changes of the market credit spread and of the market liquidity spread. The former represents the credit risk premium required by market participants for a given credit quality i.e., the market price of risk under the same level of creditworthiness. Thus, it should be noted that idiosyncratic (1) elements are not included. On the other hand, market liquidity spread is the premium that reflects the funding liquidity risk of lenders in the market. Also, CSRBB excludes any effect stemming from credit quality variation.

Figure 2: Components of Interest Rates

Whereas in the context of IRRBB, all interest rate sensitive instruments should be included, for CSRBB no instrument in the banking book should be excluded ex ante, except for instruments under default. This includes assets, liabilities and off-balance sheet items, regardless of their accounting treatment. Moreover, EBA adopts a pragmatic approach by stating that the exclusion of any instrument should be in the absence of sensitivity to credit spread risk. Also, EBA examined the feedback received from the 2018 Guidelines and the Quantitative Impact Study (QIS) and requires all non-trading book assets at fair value to be considered.

Contrary to IRRBB, there are no specifications on the identification, calculation and allocation of capital for the purpose of CSRBB. Thus, there are no provisions regarding the computation of the contribution of CSRBB to the internal capital assessment of the institution, and likewise, no guidelines on methodologies for capital allocation and the consideration of internal capital buffer adjustments.

The former is also in line with the governance and strategy requirements, where, despite the similarities (e.g.: in implementing procedures for the analysis of CSRBB when proposing new products) there is no clear specification for including the risk appetite for CSRBB mitigation on the overall strategy and for it to be expressed in terms of acceptable impacts/ limits. This is also reflected in CSRBB not having a dedicated chapter on risk appetite and policy limits. Conversely, the risk appetite for CSRBB should be part of the overall strategy and expressed in terms of the impact of fluctuating credit spreads on both EVE and NII.

As stated, the requirements for the risk management framework and responsibilities under CSRBB are aligned with IRRBB. The list of responsibilities of the management body are detailed because it should bear the ultimate responsibility for the oversight of the CSRBB management framework and the institution’s risk appetite framework. Analogous to previous matters, the differences are related to capital adequacy and limits setting, which are exclusively of IRRBB.

In the risk policies, processes and controls chapter, the same line of reasoning is maintained, i.e., apart from the specificities and a more expanded set of requirements for IRRBB, the striking difference is again related with the allocation of internal capital and exposure limits. However, this chapter is particularly interesting because it sheds a light on the CSRBB identification, measurement, monitoring and control processes by noting, for example, the need of procedures for updating scenarios and the need of documenting of the size and form of the spread shocks to be used.

The latter examples are listed under the risk policies and processes sub-chapter, which also includes the need for:

Similarly, the sub-chapters dedicated to IT system and internal reporting are more differentiated and likewise, it is possible to catch a glimpse of the CSRBB assessment and monitoring process. Specifically, the systems should:

Furthermore, the reports should include:

The sub-chapters concerning internal controls and model governance are similar but less concrete than the requirements for IRRBB.

Finally, the regulatory framework regarding the measurement of IRRBB is extensive. However, for CSRBB it is vague. This can be particularly noted by the regulation usually referring to “measurement of IRRBB” on one hand, and “monitoring of CSRBB” on the other. This conveys a lack of concretisation. Additionally, this is also illustrated by the absence of a limits’ system and a clear methodology.

The Guidelines do not specify how the CSRBB should be assessed and monitored. They require institutions to implement “robust internal measurement systems (IMSs) that capture all components and sources of CSRBB which are relevant for the institution’s business model” and to “monitor their exposure to CSRBB in terms of potential changes to both the economic value and net interest income’’. Also, they expect institutions to capture CSRBB over the short- and long-term and to evaluate the impact of key modelling assumptions for the EVE and NII and the CSRBB of their banking book derivatives. Finally, it is stated that institutions should develop their own methodology and assumptions for the assessment of the CSRBB.

Thus, contrary to IRRBB, the guidelines define the methodology for the monitoring of CSRBB quite loosely. However, it is important to note that the greater part of the guidelines for CSRBB mimic the ones for IRRBB and while this is particularly true for governance related aspects, the same should prevail, in principle, for the methodology.

With this in mind, it is of particular interest, especially in practical terms, to develop an approach that builds on the IRRBB methodology to tackle the quantification of CSRBB and monitor its exposure to the EVE and the NII. A proportionality principle should be used here: the methodology used for CSRBB quantification should not be more complex than the methodology used for IRRBB. And for instance, a Bank already relying on the standardised shocks for IRRBB may want to replicate a similar approach to CSRBB. To achieve that, the first step is to design “credit spread standardised shocks”, analogous to the specific interest rate shocks prescribed in the IRRBB sphere.

The construction of such credit spread standardised shocks has been illustrated in this document for interest rate on loans from banks in the Euro area.

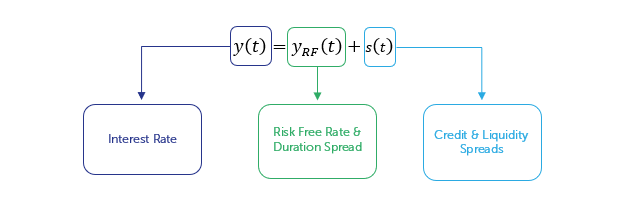

To begin with, it is imperative to identify the credit spread component \(s(t)\) in the general interest rate. Thus, time series of Euro area bank’s average interest rate on loans \(y(t)\);were retrieved from the European Central Bank (ECB) statistical data warehouse. The credit spread was calculated as the difference with a time series of Euro area triple-A rated bonds’ (risk-free) yield curves \(y_{RF}(t)\).

Figure 3: Interest Rate Formula

It should be noted that, given the fact that we are considering a pool of Euro area bank loans, the idiosyncratic credit spread components, such as geography and/or sector, have been removed.

The second step to identify the standardised shocks consists of applying a principal component analysis (PCA) to the credit spread time series. This dimensionality reduction technique transforms a set of correlated observations into uncorrelated variables, solving the critical issue of autocorrelation between the different tenors. If \(s_T(t)\) denotes the tenor \(T\) of the credit spread curve at time \(t\), then the curve can be decomposed as a sum of basic curves \(v_{i,T}\) called principal components:

$$ s_T(t) = \sum_{i=1}^{N} a_i(t)\, v_{i,T} \approx \sum_{i=1}^{2} a_i(t)\, v_{i,T} $$

The weights \(a_i(t)\);applied to each principal component are the factor loadings. There are as many principal components as there are variables. These uncorrelated variables are then classified by the amount of the explained variance, where usually, only a few principal components are sufficient to explain most of the observed variance.

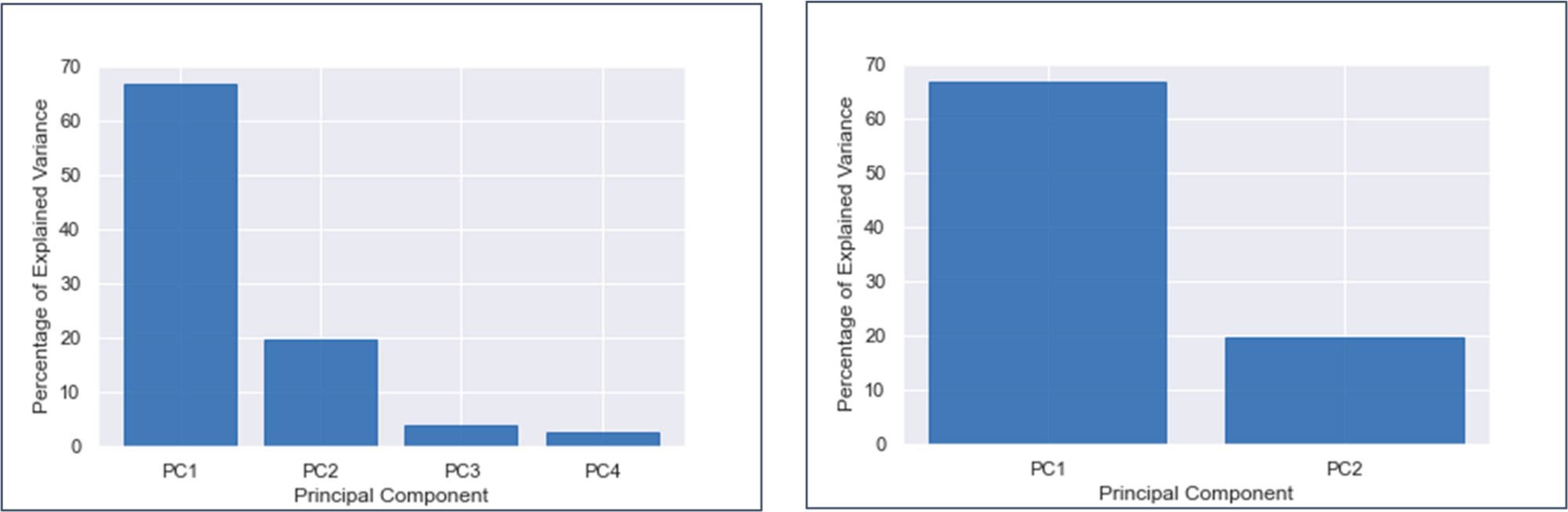

Figure 4: Scree Plots of the first 4 and 2 Principal Components

In the case of the credit spread curve, the first 2 components capture 86.4% of the variance. The first principal component explains 66.7% of the variance and the second 19.7%, as shown in the scree plots of Figure 4.

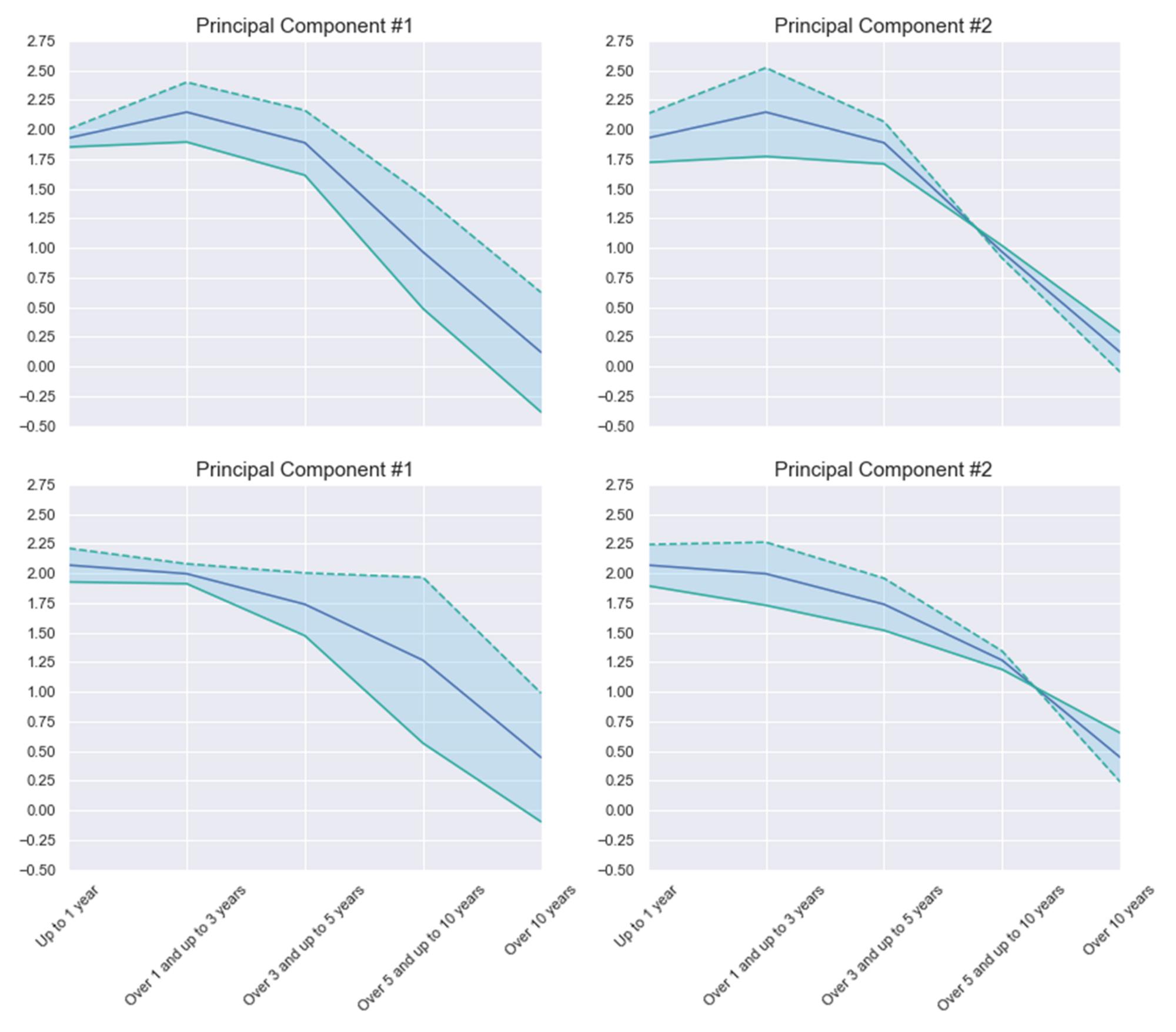

We are particularly interested in the financial interpretation of the first 2 principal components in terms of the form of the credit spread curve. The first can be interpreted as a change in the level of the credit spread curve, whereas the second as a change in its slope. This is illustrated in Figure 5, where 1 standard deviation shocks are applied to each principal component. These resemble the paralell and non-paralell interest rate shocks applied in the IRRBB scope.

Figure 5: Effects of 1 s.d. shocks on each principal component. The first component can be interpreted as a change in level and the second as a change in slope. The upper and lower graphs concern different data sets on Euro area bank loans (with and without collateral and/or guarantees).

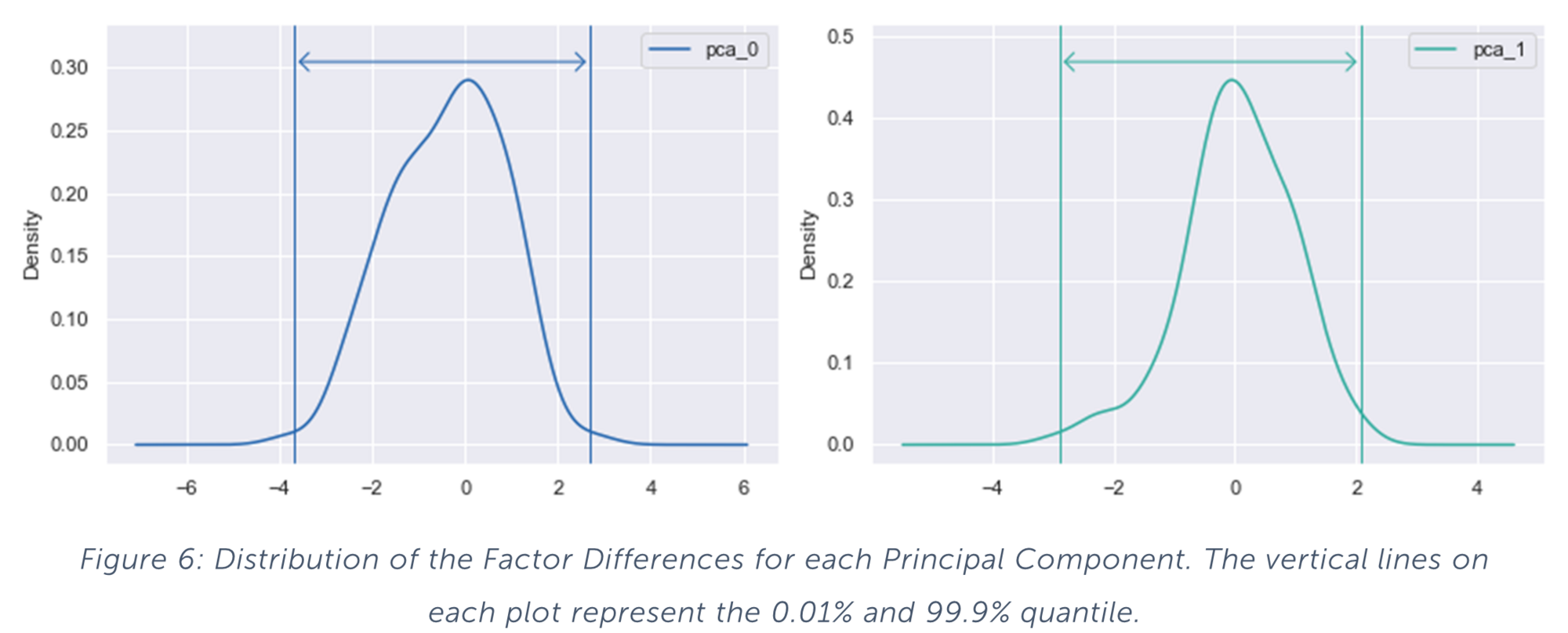

Finally, the PCA only provides the shape of the credit spread shock, but we also need the magnitude of these shocks. To estimate the latter it is necessary to calculate the 12-month difference of each factor loading ait . Next, by looking at the distribution of those differences and estimating, for example, the 0.1% and 99.9% quantile we are determining the “worst case” size of these shocks.

The latest consultation papers, particularly the guidelines on CSRBB, increase the regulatory pressure to include the assessment and monitoring of this type of risk in the risk management strategy of banks. However, the EBA guidelines do not specify a standard methodology for the evaluation of CSRBB and thus, rely on institutions to implement IMSs that capture all relevant components and sources of CSRBB.

After the public hearing on the consultation, the draft guidelines will still need to be finalised, endorsed by the EBA Board of Supervisors and translated into the official EU languages before publication. The RTS needs to be submitted to the EU Commission. However, the application dates of the GL and the RTS may be postponed to match which would grant additional time to comply with CSRBB requirements. Also, based on our experience, the substance of the consultation papers should not change significantly.

This whitepaper has not only highlighted the latest features of the implementation of the BCBS Standards within the EU focusing on the CSRBB, but also demonstrated how Finalyse can be a key player in implementing a model that builds on the existent IRRBB methodology to tackle the quantification of CSRBB.

With its demonstrated experience in Asset & Liability and Interest Rate Risk Modelling, the Finalyse Risk Advisory team can provide seasoned consultants to develop the approach highlighted in this whitepaper, and tailor them to the needs and specificities of your institution.

(1) Although the definition does not include idiosyncratic credit spread elements, the guidelines allow the inclusion of these components for the monitoring of CSRBB, on the assumption that the measures yield more conservative results. This grants an easier implementation and is motivated by proportionality reasons.

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support