Written by Paramjeet Singh, Consultant

Reviewed by Evelyn McNulty, Senior Consultant and Frans Kuys, Principal Consultant

On 27 January 2022, the European Insurance and Occupational Pensions Authority (EIOPA) published a consultation paper on the methodological principles involved in developing bottom-up stress tests for climate change risks. This is the third paper in EIOPA’s series on enhancing its methodology for stress testing, initiated in 2019.

Climate change risks have rapidly become a priority for insurers and regulators despite their relatively recent emergence. The scope of the January paper is the design and calibration of stress tests for climate change risks as part of the future supervisory testing framework. The main objectives are to assess resilience and vulnerabilities, and to enhance the understanding of these risks by individual insurers and the (re)insurance sector. The information in the paper is also useful to insurers when designing their ORSA climate risk scenarios, which was the subject of EIOPA’s April 2021 Opinion.

At this stage, EIOPA has not defined a timeline for the supervisory stress testing requirement. We expect to see further iterations of the bottom-up stress testing principles in the future, as EIOPA refines its work. The January paper includes an annex with examples of past stress testing exercises carried out by some national supervisors.

Climate change risks can be split into two main categories:

Physical Risks | Transition Risks |

|

|

In line with the objectives stated in EIOPA’s first paper on the Methodological Principles of Insurance Stress Testing in 2019, the main objective of climate change stress testing is to assess the impact on both micro (insurer specific) and macroprudential (sector-wide) purposes.

Given that climate change risks have a long-term and forward-looking nature, these stress tests are at this stage considered to be more of an explorative exercise to better understand the potential impact of climate change risks, rather than a conclusive quantitative assessment. Furthermore, these tests will also help in assessing and modifying existing risk mitigation techniques for climate change risks. It is important to assess these risk mitigation techniques, and insurers might need to prepare for a scenario where these risks might become uninsurable in the future.

Given the complex, uncertain and long-term nature of climate change risks, the paper defines the following five general principles to consider when designing the stress scenarios:

P1 | Both physical and transition risks should be jointly assessed. |

P2 | Multiple climate change scenarios and future pathways should be considered, that capture different combinations of physical and transition risks. |

P3 | Scenarios should focus on both central path climate projection as well as the adverse tail events. |

P4 | Sufficient granularity should be maintained for information about climate pathways and the associated financial impacts, and the scenarios should allow the identification of key variables and assumptions. |

P5 | Appropriate time horizons should be considered to reflect the long-term nature of these risks as well as allowing enough flexibility to derive short-term stress periods from long-term scenarios. |

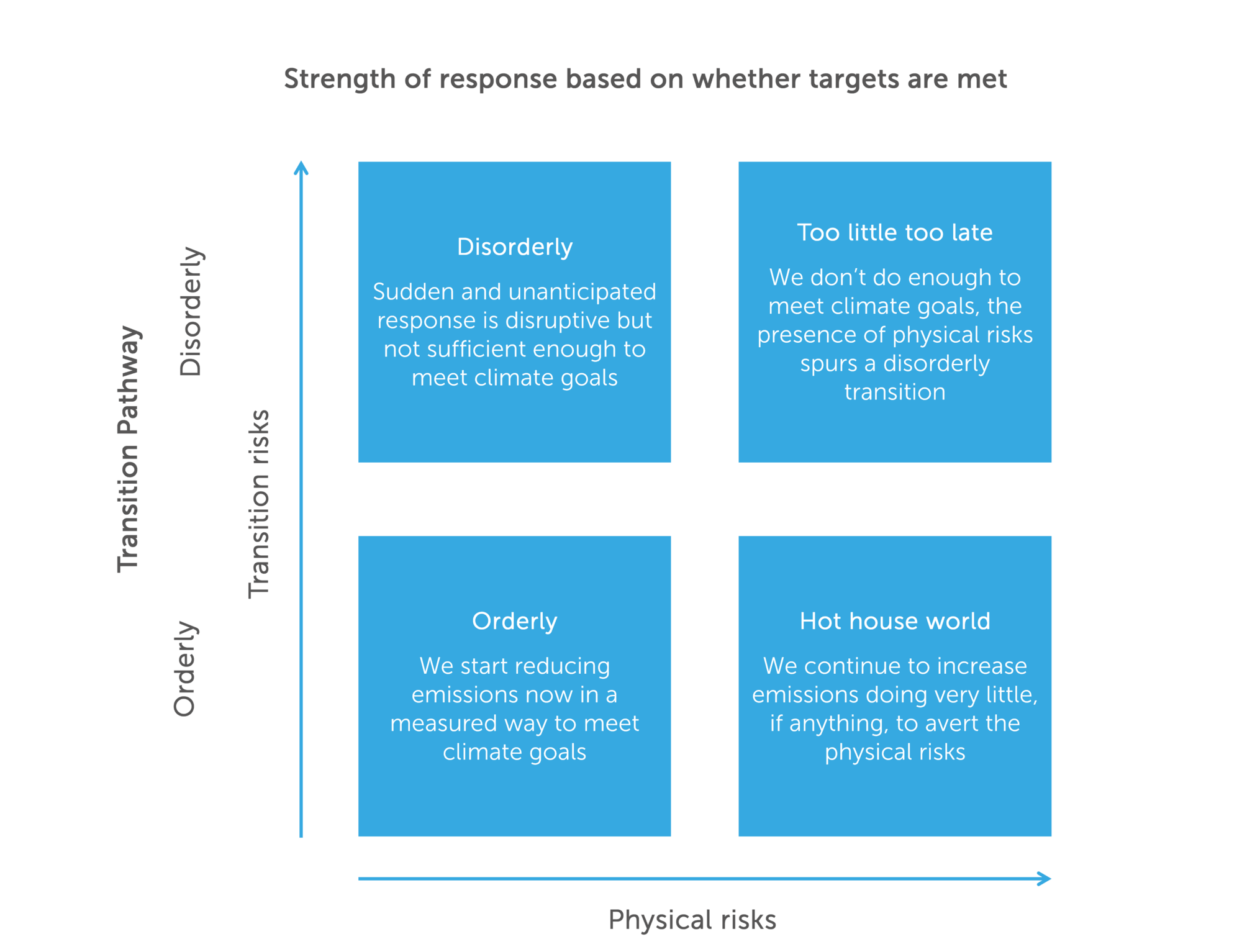

When designing the scenarios, adverse outcomes can be considered along the dimensions proposed by the Network for Greening the Financial System (NGFS), as outlined below:

Source: NGFS Comprehensive report: "A call for action: Climate change as a source of financial risk."

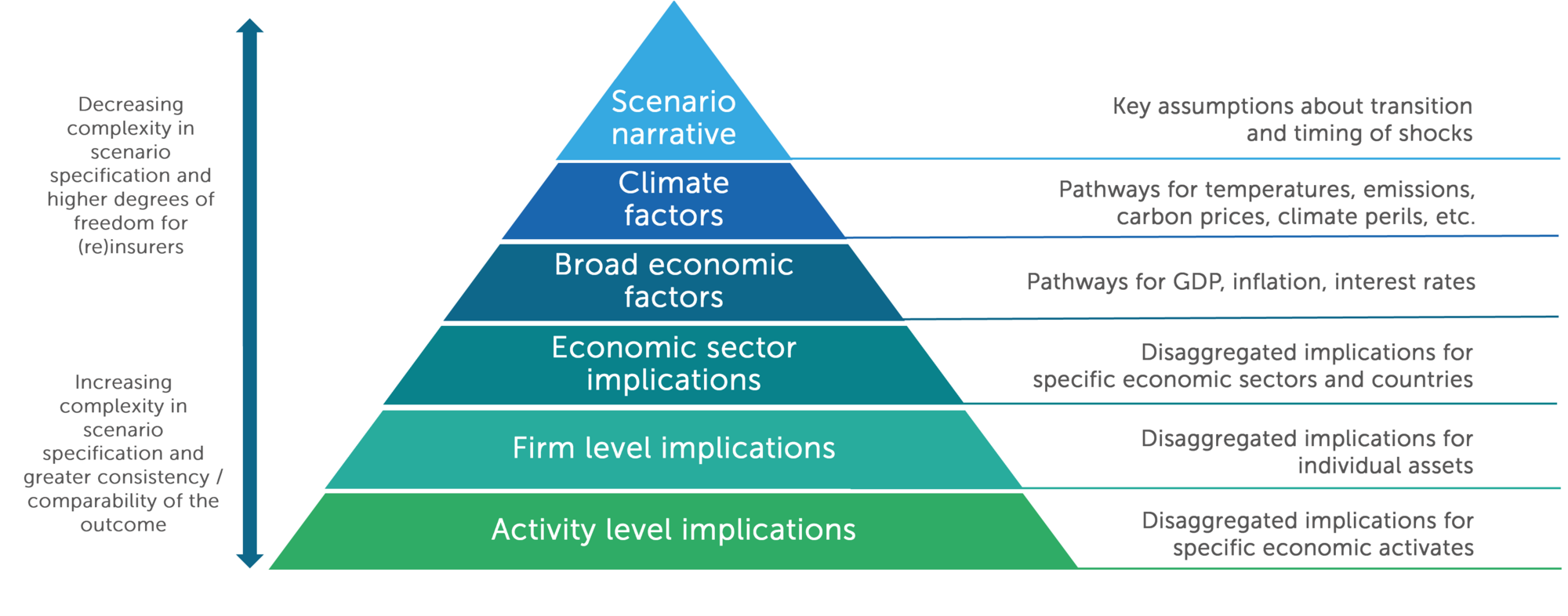

A specific climate risk scenario can be defined at different levels of detail, and the level of granularity chosen will be a key consideration. EIOPA will need to decide on the level of granularity for the supervisory stress test definition.

A high-level stress test definition with modelled future pathways of climate-related factors (e.g. temperature change, carbon price) is one option. This would allow flexibility for insurers to translate these to financial and underwriting impacts using their own modelling and judgement.

Another option is that EIOPA could specify the scenarios in greater detail. For example, by specifying granular stress impacts on different sectors, countries or regions. This would take some of the flexibility away from insurers but would result in more comparable results.

The paper outlines EIOPA’s views on the advantages and disadvantages of the various levels of granularity and states that they currently consider the definition of scenarios at economic sector level to be most appropriate, with shocks calibrated at country or regional level where appropriate. This view may be updated in future, in light of feedback on the paper or modelling developments.

The different levels of scenario granularity are summarised in the pyramid below:

Source: EIOPA adopted from Bank of England

The time horizon is another key consideration in designing the stress scenarios for climate change risks. Climate change risks are expected to fully manifest over the medium to long term, and hence need to be assessed over a longer period than typically used in stress tests.

Type of Risk | Time horizon | Financial impact | |

Physical Risk | Acute / extreme climate events e.g. floods | Short to medium term | Assess the immediate impact of the unexpected shock on the physical assets and liabilities. |

Chronic / gradual worming events e.g. rising sea levels | Medium to long term | Assess the impact of anticipated shocks to physical, financial and non-financial assets | |

Transition Risk |

| Short to medium term | Assess the immediate impact of the unexpected shock on the financial and potential stranded assets |

EIOPA also recommends that a separate forward-looking assessment should be in place to assess the impact of any reactive management action taken by insurers and stakeholders as a part of risk their mitigation strategy. This will help insurers better understand the implications of risk mitigation strategies on their business and any potential spill over effects to other financial sectors or the economy.

The impact of physical and transition risks will need to be considered on both sides of the balance sheet. The paper discusses possible modelling approaches to derive and calibrate both physical and transition risks. It states that due to the high level of uncertainty of future developments, the assumptions and limitations of climate modelling, any of the methodologies discussed will have to be complemented with expert judgement to validate the severity and plausibility of modelled shocks.

In line with EIOPA’s Principle 2, both the physical and transition risks will need to be assessed under multiple scenarios, including scenarios with a combination of the risks; it is not recommended that they be assessed in isolation.

There are some publicly available tools and scenarios which can be used to assist with the model process. The paper goes into detail on the tools that EIOPA considers useful for various risk types. The following table summarises some of these:

Transition impacts on assets | Physical impacts on assets | Physical impacts on underwriting activities |

|

|

|

The list of methodologies and tools available are not exhaustive and EIOPA expects the results of the modelling scenarios to change over a period of time as models will start overcoming limitations of data, assumptions and parameters.

EIOPA anticipates that the following key variables will need to be specified in any climate change related stress test scenario:

Variable | Variable type | |

Global/Regional temperature pathways | Physical | Climate |

Frequency, severity and correlation of climate change events | Physical | Climate |

Mortality/Morbidity parameters | Physical | Climate |

Regional/Sectoral emission pathways | Transition | Climate |

Carbon price pathways | Transition | Climate |

Commodity prices and the energy mix | Transition | Climate |

GDP, interest rates, inflation, real estate prices | Macroeconomic | Financial |

Bond yields (Government/Corporate), Equity indices/shocks | Market | Financial |

The paper states that the impacts of the stress tests will need to be evaluated using a variety of metrics, which are split into three categories:

| Type of Risk | Indicators |

Balance Sheet Indicators | Physical and transition risk |

|

Transition risk |

| |

Physical risk |

| |

Profitability Indicators

(split into Main and Ancillary, based on significance and availability)

| Physical risk | Main indicator:

|

Physical and transition risk | Ancillary indicator:

| |

Technical Indicators | Indicators such as aggregated losses (both gross and net), Sum Assured, Asset values subject to transition, Maximum loss (Similar to 1-in-200 losses under Solvency II), Probability of a climate change event etc. can be used to assess impacts at a technical level.

It is recommended that the assessment includes different loss metrics such as expected average losses and tail losses (losses under an extreme event) based on the purpose of the analysis. | |

The paper discussed in this article outlines EIOPA’s methodological considerations for integrating climate-related risk into their future supervisory testing framework. This valuable information can be leveraged by insurers as they work towards integrating climate risk scenarios into their ORSA, which EIOPA will begin to monitor from April 2023.

Finalyse has extensive experience in risk management for insurance companies and can help you make sense of the climate risk puzzle. We have several services on offer to help with integrating climate-related risks into your Risk Management Framework and ORSA, including:

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support