VALUE AT RISK (VAR) CALCULATION

If you are subject to risk monitoring regulation (UCITS, AIFMD, FRTB, Basel), you may be interested in benefiting from outsourcing VaR computation. We offer VaR calculation as a managed service allowing our clients to save time and money. Our risk advisory and valuation specialists are able to onboard any type of portfolio.

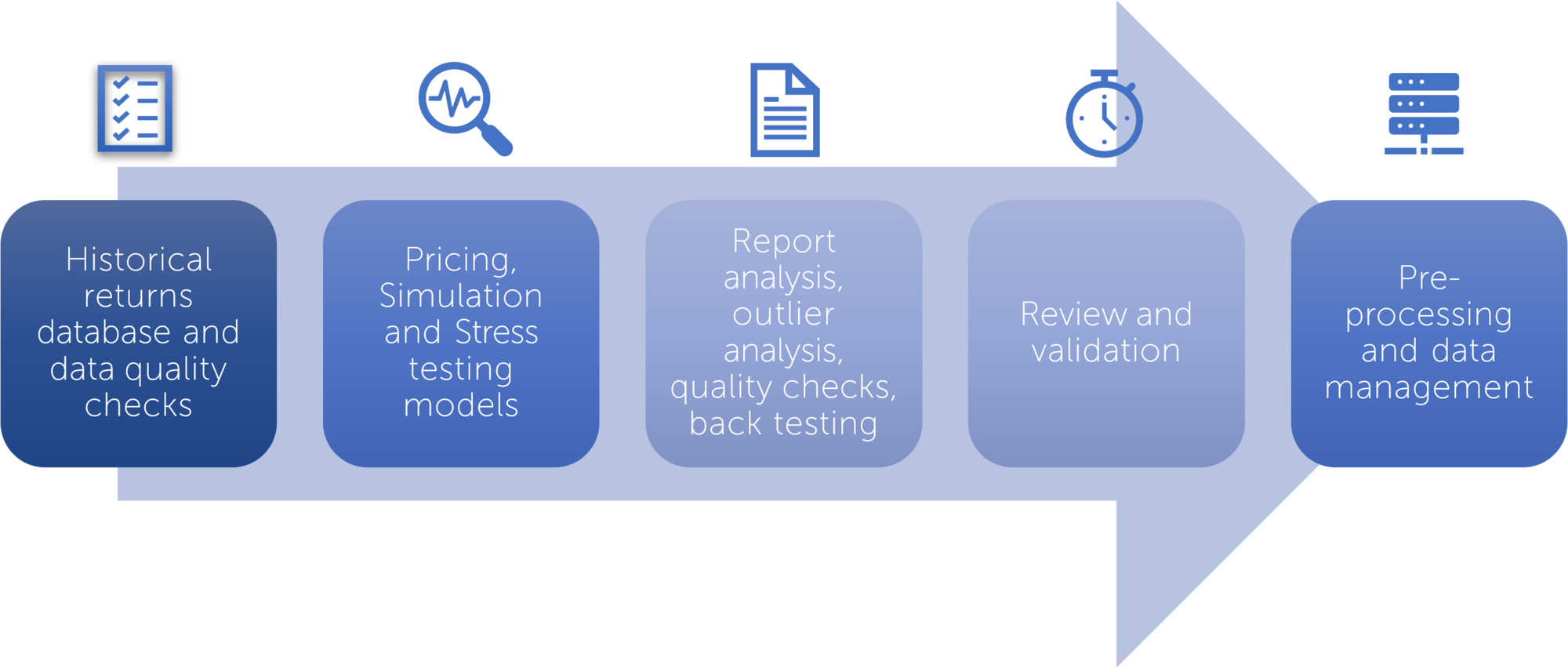

We propose a holistic service starting from portfolio template to risk report. An expert will accompany you on the entire journey.

We apply several methodologies of VaR calculation: Monte Carlo normal or Variance Gamma as well as historical VaR.

How does Finalyse address your challenges?

Client support

A team of consultants is available every day to follow up on requests from clients. We have developed our own methodology and databases, which allows us to propose solutions for any type of portfolio.

Daily VaR calculation

Several types of VaR (Montecarlo, Variance Gamma Montecarlo, Historical), together with all related indicators: CVaR, IVaR, expected shortfall.

Valuation

Thanks to our experience in valuation, you can benefit from a joined service of valuation and risk measurement for portfolios invested in complex products.

Personalised services

We provide customised delivery formats and affordable pricing.

Regulatory Compliance

UCITS and AIFMD compliant model.

Daily stress tests computation

Stress tests are complementary to VaR.

Key Features

- Monte Carlo and historical VaR report daily with all related indicators (CVaR, IVaR, Expected shortfall).

- Backtesting monitoring and follow up in case outlier.

- Tailor-made stress tests framework elaboration and daily reporting.

- Full dedicated report design.

- Daily support.

Marc-Louis Schmitz, Partner at Finalyse and member of the executive committee, is the founder of the independent valuation services business line.

He oversees operations, team management, and strategic development.

Known for fostering an inclusive, growth-oriented work environment, he supports a skilled team dedicated to mastering complex valuation processes, models, and best practices.

With a strong background in valuation, risk modeling, and regulatory compliance, Marc-Louis has expanded Finalyse's managed services to meet evolving regulatory and client needs.

Régis, Principal Consultant experienced in risk management within the banking and fund industries, has significant expertise in heading asset management companies. He is well acquainted with Basel 3, AIFMD, UCITS and MiFID regulations. Thanks to his experience, Régis has developed Finalyse’s specific offer in the independent valuation and risk management process set up for the fast-growing private equity funds industry sector. Before joining Finalyse, Régis was a Vice President / Head of Risk Management in a mutual investment fund. He was in charge of developing the risk management process and was a contact person for regulators concerning all Risk Management related issues.

Client Cases

A Luxembourgish Management Company has under its responsibility a set of UCITS and AIFs sub-funds that needs to have a daily computation of VaR and corresponding stress tests. VaR is normally required for complex strategies (involving extensive use of derivatives for example) but the Management Company has chosen to compute the VaR for all sub-funds regardless of the obligation towards the regulator. This provides a global unity among sub-funds’ risk management process and gives an additional tool for the risk management department to monitor and compare the market risk of each portfolio. The VaR computation is coupled with a specially dedicated stress testing framework meant to complete the global risk picture of each portfolio.