Written by Alvin Mehmeti, Senior Consultant.

The revised reporting requirements for derivatives under EMIR as of April 2024 are outlined below.

A set of requirements known as European Market Infrastructure Regulation (EMIR) took effect on August 16, 2012, with the intention of enhancing the transparency and reducing the risks in the OTC derivatives markets. Any organization that is a counterparty to a derivative contract is subject to this regulation. Examples include but are not limited to: forward contracts for foreign exchange, interest rate swaps (IRS), other swaps, futures and options on securities and commodities, regardless of whether they are traded bilaterally or on trading exchanges, and regardless of the volume.

The EMIR has subsequently been several times amended to improve data quality and align EU legislation with IOSCO standards.

There are two categories of counterparties in EMIR:

In accordance with the EMIR framework, CCPs that have been authorized (for European CCPs) or recognized (for non-EU CCPs) must clear specific classes of OTC derivatives.

EMIR envisions two potential methods for determining the pertinent types of OTC derivatives:

EMIR allows one party to report the details of the trades on behalf of both counterparties, or, alternatively, a third party is permitted to report on behalf of one or both counterparties.

EMIR requires FCs to report OTC derivative contracts on behalf of NFC-. However, the NFC- is required to disclose all the necessary information with the reporting counterparty and bears the ultimate responsibility for the reporting. NFC-s are not required to report data on collateral, mark-to-market, or mark-to-model valuations of the contracts.

Furthermore, Intragroup derivative transactions are typically conducted to aggregate certain market risks at the group level or to protect against such risks. All other EMIR criteria apply to intragroup trades in the same manner as they do to all other transactions, except for a few risk mitigation strategies from which intragroup transactions are excluded under specific circumstances. There are two intragroup-transactions exemptions under the EMIR legal framework available: one relating to the clearing obligation, and the second regarding collateralisation requirement. Additionally, except for risk-reducing transactions, intragroup transactions must be taken into account when determining whether a non-financial counterparty exceeds the clearing threshold.

The EMIR will be enhanced by new technical standards that will be in effect as of April 29, 2024, as well as guidelines regarding the reporting of derivatives as required by Article 9 of EMIR that was made available on ESMA’s website.

These guidelines consist of:

The following documents, collectively referred to as the "Technical Standards," were published in the Official Journal of the European Union on October 7, 2022, and will be applicable as of April 29, 2024:

To ensure consistency of the language and format throughout the whole reporting chain, XML schemas will now be necessary for communication between reporting entities, trade repositories, and authorities. This corresponds to the SFTR reporting requirement. XML ISO 20022's end-to-end reporting is anticipated to significantly improve data quality and uniformity by decreasing the requirement for data cleansing and normalization and facilitating their use for both authorities and reporting entities. To comply with this new criterion, report-submitting entities that utilize formats other than ISO 20022 XML will need to redesign their reporting process.

In addition to the format changes, the report's content has also been altered. In particular, the global guidance created by CPMI-IOSCO on the definition, format, and usage of key OTC derivatives data elements reported to trade repositories, including the Unique Transaction Identifier (UTI), the Unique Product Identifier (UPI), and other crucial data elements, is what has led to most of the changes. The validation rules and the annexes to the RTS 2022/1855 and ITS 2022/1860 provide for:

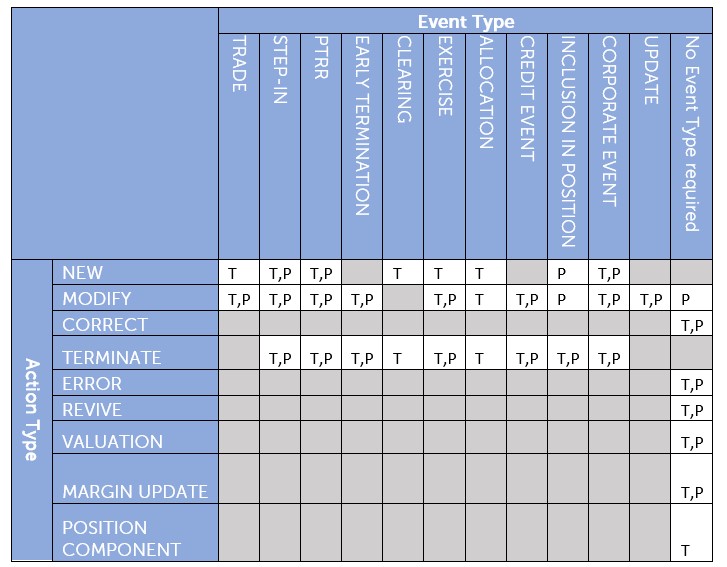

To provide more detail about the sort of business event that is triggering a particular report, ESMA included Event Type because the Action Type column by itself is insufficient to describe the business event. Here is how action types and event types are combined:

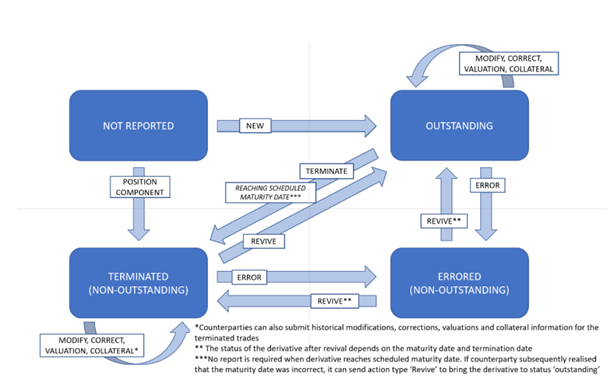

Introduction of action type ‘Revive’, that can be used to reopen derivatives that have been accidentally terminated (with action type "Terminate"), cancelled (with action type "Error"), or have achieved their maturity date (but have been wrongly reported).

Moreover, if the action type "Position component" was accidentally reported, "Revive" can be used after it. In this situation, the revived derivative will be regarded as outstanding at the trade level, subject to the expiration date. It would need to be reversed individually (by erroring or changing such position, respectively) if the counterparty reported a new position or a modification of a position.

Due to the considerable modifications made as well as the effort required to synchronize the IT infrastructure, the revised Technical Standards will be in force as of 29 April 2024. All reports that counterparties submit to trade repositories after that date must therefore adhere to the modified standards. This is applicable to any changes and terminations reported on existing derivatives after the new reporting start date, regardless of when the modified or terminated derivative was concluded. It also applies to reports on derivatives concluded after that date.

However, outstanding contracts that were submitted to the trade repositories before April 29, 2024, and which do not call for any modifications or termination reports, will be given an extended transition period of 180 calendar days. It's not necessary to update derivative contracts that mature during this transition period.

In accordance with ITS 2022/1860's Article 9(1), enterprises in charge of reporting are now required to alert the appropriate authorities in the event of notable reporting problems. The rules specify the conditions under which a problem is regarded significant and is required to be reported to the NCAs.

Moreover, ESMA has made available a template for NCAs that have chosen to use it for filing these notices part of the validation rules excel that is provided in ESMA’s website.

All involved stakeholders are expected to make sure that they are prepared to:

The Unique Product Identifies (UPI) is a new field that will be in effect starting from 29 April 2024.

Several requirements, including uniqueness, persistence, consistency, neutrality, dependability, open source, scalability, accessibility, availability at a fair cost basis, and adequate governance framework, are met by the product identity (UPI) used in derivatives reporting.

The necessary jurisdictions must implement a global UPI for OTC data to be aggregated globally. ESMA is adhering to the IOSCO UPI technical guidance's guiding principles.

Moreover, ESMA continues to take the following stance: Any derivatives admitted to trading or transacted on a trading venue or a systematic internalizer will only need to be identified with an ISIN, while all other derivatives will need to be identified with a UPI only.

At a first glance, EMIR Refit appears to be a full year away. Nonetheless, anecdotal data reveals that most of the institutions affected are not aware of the difficulties that lie ahead of them. In fact, they need to start getting ready right away by performing the necessary impact evaluations. As part of that preparation, a trade and transaction reporting solution is needed that is independent of jurisdictions, natively supports ISO 20022, and has capabilities for managing, resolving, and simulating UPI transactions. Institutions in charge of new trade-state, transaction activity, and reconciliation reports will also require a high level of expertise and specialized instruments to manage reconciliation. To comply with the Refit standards, they will also need to update their control frameworks.

For ESMA to fulfill its oversight duties and advance stability and transparency in the securities markets, high-quality data is a requirement. It therefore establishes quality and harmonization standards to guarantee the consistency, accuracy, and completeness of data utilized for regulatory purposes.

Finalyse’s goal is to provide our customers with the opportunity to be EMIR compliant with the least amount of expense and effort while still utilizing our knowledge of reporting under European regulatory standards. We have a lot of previous experience assisting institutions with meeting reporting-related standards.

For more information about our services please visit Finalyse Reporting Services.

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support