Written by Jean-Pascal Kretz , Managing Consultant

In our previous article, we examined the risk components constituting the backbone of the risk appetite definition – Risk Profile, Risk Capacity, Risk Tolerance, and Risk Limits. With these in place, it is possible to establish a strong risk appetite framework that we will now endeavour to express in the risk appetite statement.

The Statement issues the high-level strategy applicable throughout the institution and simultaneously acts as an internal and external communication tool. The company’s approach to risk as seen from the Board of Directors and actual operational reality could differ significantly without a company-wide communication on corporate strategy, risk typology and clearly defined monitoring metrics and limits.

A strong framework thus enables management to:

We will now be detailing the mechanisms governing risk decisions and the underlying complexity of using risk appetite as a component of the strategic decision.

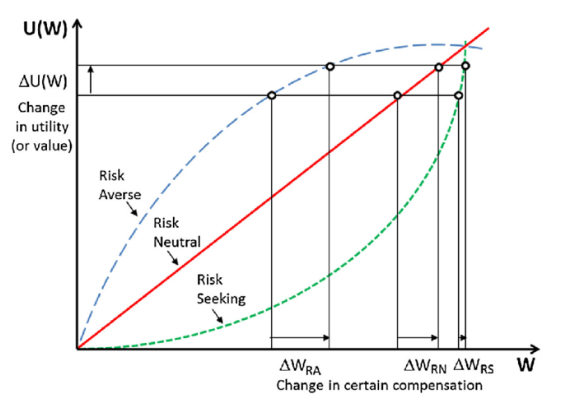

This graph from Christopher Harris shows the possible shapes of the utility function, depending on the attitude towards risk of an individual:

Transposition of risk preferences from persons to institutions is conceptually simple. It must be a conscious process for corporates, widely expressed and communicated to ensure alignment throughout the organisation. Risk preference of an organisation will depend on its deciding level (Board of Directors, along with C-level executives) and will range from risk adverse to risk seeking.

Because a rational business decision must be taken with risk preferences in mind, the organisation has to ensure that the overall strategy and risk preferences are aligned in their risk and reward perspectives.

There is a link between risk preference and preferred risk response. The more risk adverse the Board of an institution is, the higher the chances the organisation will resort to risk avoidance, risk mitigation or risk transfer.

Risk avoidance is the most straightforward concept: “should we accept this risk?” is answered with “Yes” or “No”.

This decision does not have to be quantitatively justified. Indeed, as expressed by FSB, this part of the Risk Appetite Statement involves “(…) qualitative statements that articulate clearly the motivations for taking on or avoiding certain types of risk”. This makes it an obvious candidate for easy definition and clear communication within the company.

However, avoiding risk is not neutral from a business perspective; in fact, systematic risk avoidance will ultimately lead to a form of loss (e.g. market share, profitability or reputation). Avoidance of risks, despite apparent simplicity, should be the last resort option, when all mitigation options are ruled out. Cases where the decision would have an immediate negative impact on the company’s image (e.g. politically exposed individuals, recourse to short sales or investment in embargoed products or markets) are exceptions.

The more risk-adverse company can opt for risk mitigation or risk transfer.

Either as a requirement for the institution to accept additional risky exposure, or a consequence of sudden changes in the macroeconomic environment or the portfolio / business risk profile.

In a Risk Appetite Framework perspective, this becomes a balancing act: in search for additional revenues (or any other reward for the risk taken), the institution aware of its risk profile can estimate its risk capacity and tolerance, with all exposures outside of the tolerance range having to be neutralised, through risk mitigation or transfer.

Application of risk mitigation measures usually requires an existing organised market and open interests. Mitigation (bringing the risk down to a residual level that is within tolerance) through e.g. guarantees or swaps, or transfer (passing ownership and reward of the risk on to another player) through e.g. securitisation or (re)insurance requires access to an active market. Additionally, regulatory bodies scrutinise quite intensely risk mitigation procedures, no matter what form they take. Therefore, defining the mitigation measures prior to building up the risky exposure is a best practice.

Preparing the mitigation strategies also ensures that costs for mitigation - or the decrease in expected return in the case of a risk transfer, are lower than the gains from accepting the risk at origination. Otherwise, the unsuspecting institution could end up subsidising other market players to the detriment of its own survivability.

Conversely, risk-seeking institutions will accept that certain risks will be quantified, maintained at low materiality, but not actively managed (acceptance / contingency).

Risk acceptance and contingency require extensive analysis of the risks at hand; risk acceptance needs backing by measurements and monitoring to ensure the risk-reward relationship of a new risk is sufficient, while risk capacity and tolerance allow the additional risk to be taken on a standalone basis. Contingency ensures that, for risks deemed non-material, potential costs of the realisation of the risk are properly estimated and provisioned.

Eventually, risk taking decision and its operational requirements remain driven by the strategy, perceived net gain, risk tolerance, profile, capacity and limits. An organization must consider its risk appetite at all time, as it decides which goals or tactics it pursues.

This is where a risk appetite that is developed and formalised, communicated and monitored closely comes into play.

As an example of the complexities of establishing formal, unified views on risk appetite, the interested reader should turn to the Willis Towers Watson article “The surprising inconsistency of risk appetite and risk tolerance statements” based on Willis Re’s research from 2016.

Therein, the 10 main concepts expressed in risk appetite and risk tolerance statements of 48 US based insurance companies are provided. Not only are common concepts not so frequent, with the notion of “Surplus – Risk Limit”, the most widespread of the 10 representative concepts, reaching only 57% representation, but firms using similar concepts are sometimes implementing or defining these very differently.

In a public address in 2018, Danièle Nouy made it quite clear that European banks still had room for improvement on their Risk Appetite Frameworks on four main topics:

The parting words were quite clear:

“Risk is at the heart of banking. Banks need to find ways to deal with it. It seems however that, prior to the crisis, some banks were too busy taking on risks to be able to properly manage them. As a consequence, they took on more risks than they could cope with.

Risk appetite frameworks play a key role here; we take them seriously and so should the banks. After all, the frameworks help banks to define the level of risk they are willing to take on. This in turn helps them to keep their risks under control and manage them properly. My impression is that many banks have made good progress. However, there is still room for improvement. It’s in the banks’ own interest.”

Let us consider a bank looking to tap into a niche market or enter a given lending space to gain new revenues.

We assume the decision is driven by a bottom-up feedback from business and operations that there is an opportunity to be seized, which is in line with the risk preferences of the firm and with its current strategy.

One way to reach the goal is to take an aggressive stance and relax its lending criteria relative to its peers’, thus on-boarding riskier prospects. Alternatively, charging lower interest rates than the competition on a comparable risk level, slashing its margin in the process, could be successful.

We regard the choice as mutually exclusive, due to the high-risk level of pursuing both approaches concurrently.

The first approach will affect the cost of risk - and further down the road the regulatory capital requirements, when the second will be impacting the bank’s overall profitability.

Risk tolerance and risk limits are set up, respectively in terms of new score limit for automatic acceptance of a file or minimal commercial rate to apply. In very limited cases, for specific customer profiles, exceptions can be allowed under strict conditions and monitoring.

A limit is set on the maximum envelope available for the campaign, with plan to securitise all standard loans if the portfolio goes above a certain threshold or if interest rates indices remain low or keep on decreasing; due to their nature, “exceptions” mentioned above will be kept on the bank’s balance sheet and not be securitised.

Note that the same business case could be drafted for an insurance company actively looking at gaining market shares or cash in on premiums from an untapped market space in non-life products. To ensure mitigation of the risk, the company could opt for re-insurance or syndication of the risk across players. By adding life / non-life product mix considerations, risks to manage would differ further - liquidity risk for non-life activities and interest rates for life insurance, therefore adding complexity.

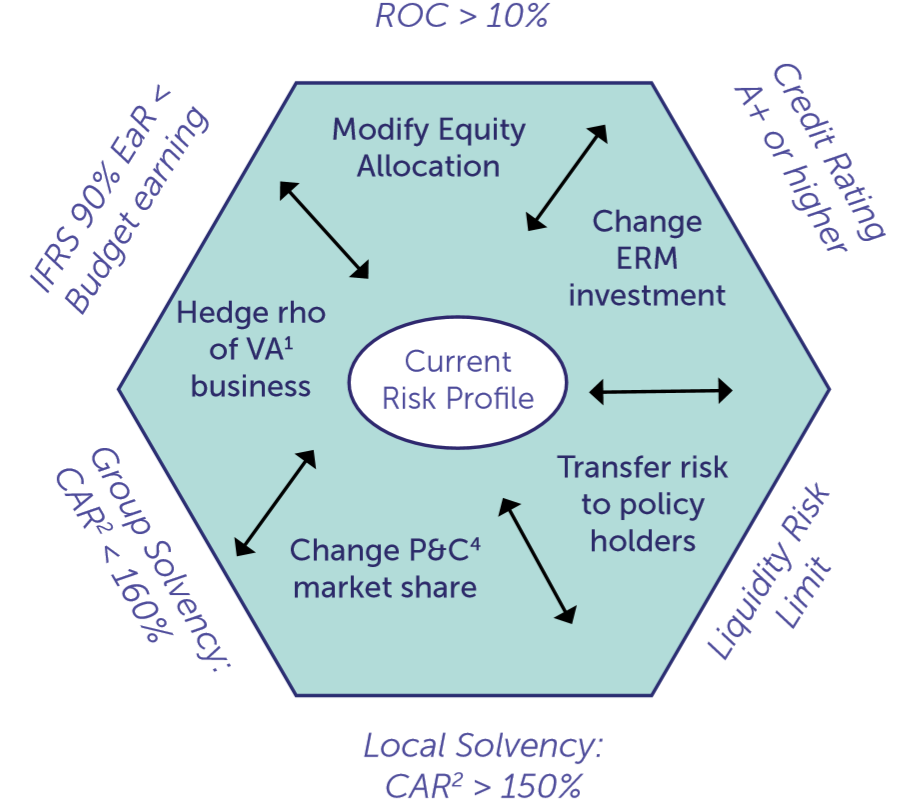

The following graph, adapted from a Society of Actuaries research document, will help visualise the puzzle under another format, by showing the range of strategic plans (emerald green background) constrained by the limits (red lines) defining the risk tolerance surface (blue background), depending on the current risk profile (white oval) of a fictional insurance company:

In this graph, limit selection is for illustration and happens at a very high level; in reality, limits need to be actionable at much more granular levels, making the exercise quite more complex.

Additionally, with organisations integrating multiple business units and multiple products on offer, we have numerous entry points for new risks, creating new sources of uncertainty or modifying their relative weight and position in the overall risk profile of the company.

This dynamic risk profile has an impact on the levels of tolerance and resulting limits at play on an ongoing basis, reinforcing the need for an articulated Risk Appetite Framework based on an appropriate level of sophistication.

This will be the topic of our next article.

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support