Written by Frans Kuys, Consultant

The new IORP directive aims to harmonise the supervision of pension funds across the Europe. It focuses on reinforcing the governance through the introduction of three key functions that funds must implement: risk management, actuarial and internal audit. However, it also introduces additional requirements for funds in other areas such as communication, remuneration and environmental, social and governance – related factors.

The additional requirements of IORP II aim to increase transparency, especially in the way that funds communicate with their members. Funds are required to provide an annual pension benefit statement (PBS) to their members - past, current and prospective - with a separate list of requirements for each of these categories.

In order to provide more clarity and guidance regarding these communication requirements, EIOPA released two model PBS’s and a guidance document on the model PBS design earlier this year. These documents build on the previously released Guidance and Principles Based on Current Practices, and focus on the PBS that has to be provided to members. The guidance also covers the communication required at the date of joining or leaving the fund, specifications around the setting of assumptions and the presentation of the information.

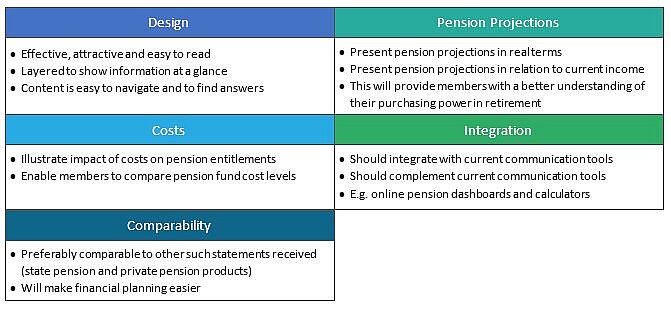

Pension providers are required to send their members a PBS at least once a year. The main principles to consider in preparing the PBS are shown below:

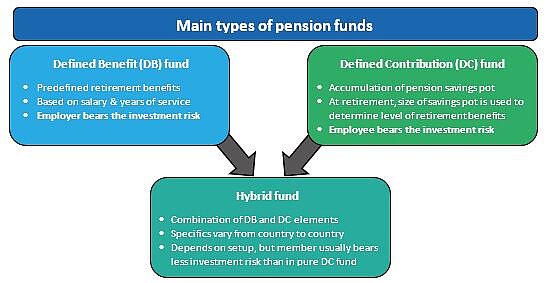

To understand the different communication needs of members, we will first look at the main types of pension available to members.

Since members bear the investment risk in a DC fund, they face significant uncertainty regarding the pension benefit they can expect to receive at retirement. Clear and adequate communication to these members is therefore vital so that they can better understand their expected benefits as well as risks.

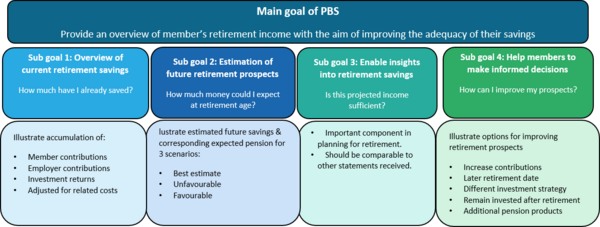

The PBS was introduced to provide members with the necessary information to help them understand their pensions and to make well-informed decisions.

The two model PBS’s were developed to guide pension funds in implementing the communication requirements under IORP II. Both model statements published were for DC funds – this could be due to the increasing trend that we see in Europe towards DC funds, as well as the higher level of uncertainty associated with the benefits expected in these funds. We expect that EIOPA will also release additional guidance on a model PBS for DB funds.

The model PBS’s are voluntary and only serve to provide funds with a base from which they can develop their own benefit statements by showing the minimum required information. Funds could adapt these by incorporating any fund specific characteristics and country specific elements, as well as applying their own design elements.

Although both model PBS’s contain the same information, they use different styles of communication in terms of the colour, visuals and the illustrations. The different model PBS’s demonstrate how a PBS can be designed differently and still communicate the same message.

The model PBS’s align with the principles published by EIOPA, with the following features:

The standardised PBS ensures that the information provided to members is consistent so that members in different funds and countries get comparable information. It also serves as a tool that could potentially result in members being more active and involved with their retirement planning.

The fund members may find their pension schemes complicated, and it is vital that communication to members includes the relevant information that they need to better understand their current and potential future benefits. This information should be presented in a way that is easily understandable to them.

The new requirements contribute to more consistent pension benefit statements across different types of pension funds and countries and ensure that members receive clear and consistent information. The model PBS’s provide funds with the necessary tools to develop their own statements for DC members, although additional guidance would be required for communication with DB members.

The requirement of pensions funds to provide annual PBS’s to their members is a step in the right direction in improving transparency and reinforcing members’ understanding of pension benefits, which in turn will help members make well-informed decisions. As an added bonus, it has the potential to result in members being more interested and actively involved in their retirement planning.

Finalyse has extensive experience in helping its clients navigate the unfamiliar territories that come with new regulations. With Finalyse as your partner, you can rest assured that your fund’s compliance with the IORP II Directive will be taken care of through a scalable set of managed services and technical solutions.

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support