Sheta Goswami is an experienced Risk Management Consultant with seven years of expertise in model validation, spanning stress testing (CCAR), CECL, Basel III IRB, IFRS 9, credit scorecards, marketing propensity, and fraud risk models. She also specializes in climate risk management, playing a key role in developing Finalyse’s climate risk practice and conducting extensive research on regulatory developments and modelling methodologies

The EBA’s Draft Guidelines on the ESG Risk Management, published on 18 January 2024, provide detailed guidance for financial institutions on handling ESG risks within short (under 3 years), medium (3-5 years) and long term (over 10 years) frameworks, aiming for completion by the end of 2024. These guidelines advocate for the incorporation of ESG risk considerations into the standard risk management practices of financial institutions, detailing specific metrics and standards, such as their inclusion in ICAAP and ILAAP, affecting the pricing, gathering and analysis of ESG data. Highlighting the complexity and potential cost, especially for smaller institutions, the guidelines also emphasize the opportunity for institutions to enhance their ESG risk assessment and data insight capabilities.

Subsequently, we will outline the key compliance requirements for banks regarding ESG risk management and offer strategies for institutions struggling to prioritize and effectively manage ESG risks.

In the evolving landscape of finance, Environmental, Social, and Governance (ESG) risks have emerged as pivotal factors influencing the financial performance and operational resilience of institutions. This guide delves into the intricacies of ESG risk management, offering a pathway for institutions to navigate these challenges while aligning with regulatory standards and societal expectations.

ESG risks, encompassing environmental, social, and governance factors, increasingly bear significant implications for financial institutions. From climate change and resource depletion to human rights and corporate ethics, these factors affect long-term sustainability and can lead to considerable financial losses if not managed. Understanding and integrating ESG risks into strategic frameworks is crucial for sustainable growth and regulatory compliance.

The European Banking Authority (EBA) plays a pivotal role in setting guidelines for managing ESG risks within the EU's banking sector, aiming to enhance its resilience and integrate ESG factors into business strategies. The forthcoming guidelines, expected by the end of 2024, will establish a comprehensive framework for financial institutions, promoting a uniform approach across member states.

Given the comprehensive detail that the new guidelines provide on ESG data and monitoring, our discussion will primarily focus on these aspects. While we will also touch on critical areas including proportionality, materiality, principles of ESG risk management, ICAAP, ILAAP, strategies and business models, internal culture and controls, these topics will be covered in a more concise manner.

The principle of proportionality applies to how institutions manage and govern ESG risk internally. All institutions are expected to adopt ESG risk management practices that align with the significance of ESG risks to their specific business models. For smaller and less complex institutions (SNCIs), it is acceptable to employ simpler risk management strategies. This might include using methodologies that are less detailed, or leaning more heavily on qualitative assessments, estimates, and proxies, provided these approaches do not compromise their capacity to manage ESG risks effectively and prudently, to remain consistent with their evaluation of risk materiality.

Materiality Assessment of ESG Risks

| Identification and Measurement of ESG Risks

|

Institutions are required to gather and assess necessary data and information, aiming to enhance the quality of ESG data progressively. This entails collecting both current and forward-looking data points, including data at the client level for instance through questionnaires completed at the initiation of credit and during periodic credit reviews, as well as publicly available data specific to clients and, where applicable, data related to assets.

For engagements with large corporate entities, a minimum of nine specific data types concerning environmental risks should be considered. These include both current and projected greenhouse gas emissions, along with energy and water usage, among others. Regarding social and governance risks, institutions should account for at least five types of data, covering aspects like adverse effects on local communities and governance practices.

ESG Risks Management Principles |

|

Strategies and Business Models |

|

Risk Appetite |

|

Internal culture & capabilities |

|

ICAAP and ILAAP |

|

Monitoring ESG risks |

|

ESG risks require ongoing monitoring – both at the portfolio level and down to individual counterparty and exposure levels. The integration of ESG risk considerations into the routine credit assessments for mid-sized and larger counterparties should be standard, possibly by enhancing the depth and frequency of these assessments with a focus on ESG risk.

Institutions ought to establish early warning signals, define limits/thresholds and prepare action plans for remediation if the limits are breached.

Given the comprehensive nature of requirements, institutions are advised to employ at least the following indicators for tackling ESG risks, with Small and Non-complex institutions (SNIs) being encouraged to consider their application:

ESG risks necessitate consideration across all aspects of business and risk strategies, requiring institutions to adopt a robust approach that includes engagement with counterparties, financial adjustments based on ESG considerations, and diversification strategies. Setting ESG-related KRIs, monitoring risk appetite, and continuously developing ESG risk assessment capabilities are essential for managing these risks effectively.

The guidelines emphasize the importance of aligning ESG plans with business strategies, public communications, and ensuring coherence across all planning horizons, with a clear focus on environmental aspects while gradually including social and governance risks. The guidelines aim to standardize the approach to ESG risk management, reflecting the sector's impacts on climate change and the broader push towards sustainability.

By adhering to these guidelines, institutions can not only mitigate the risks associated with ESG factors but also capitalize on the opportunities they present, paving the way for a more resilient and sustainable financial sector.

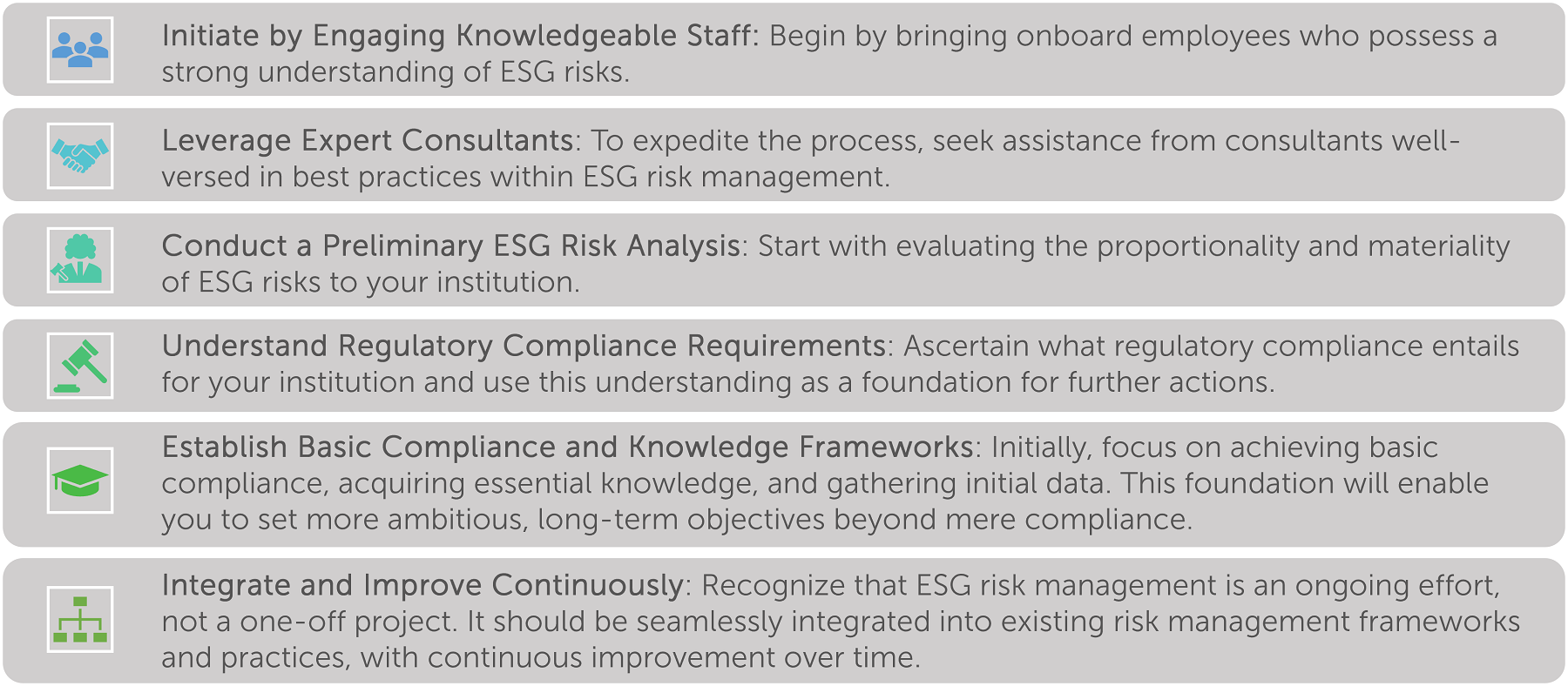

Navigating the complex landscape of ESG risk management and data collection can be daunting, especially when immediate action is required alongside a deep understanding of relevant risks and data points. A structured approach to tackling this challenge could involve the following steps:

This phased approach ensures a solid foundation in ESG risk management, from which more advanced strategies and goals can be developed as part of a continuous improvement process.

In a few words, the EBA’s CRD VI guidelines mark as a pivotal shift towards embedding ESG risks within the risk management strategies of financial institutions. By standardizing ESG risk management, these guidelines align with global sustainability goals and equip the banking sector for a sustainable future. For financial institutions, this presents both challenges and opportunities to innovate and contribute significantly to the global transition towards sustainability. As consultants, we view these guidelines as essential for helping our clients navigate these rapidly evolving regulatory and market landscapes.

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support