In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Designed to meet CRR amd CRD regulatory requirements for banks

Simulation-driven capital floor optimisation

François-Xavier is a Principal Consultant with advanced expertise in Financial Markets, ALM and Risk Management, covering both banks and insurance companies. On the banking side, François-Xavier is a practice leader on Valuation, IRRBB, FRTB, VaR, Initial Margin and Counterparty Risk, well acquainted with the regulatory requirements and the market practices surrounding market risks. On the insurance side, François-Xavier has extended experience in the regulatory treatment of financial instruments, ORSA, and hedging balance sheets against interest rate, credit spread and inflation risks.

Makram Merdas is a consultant with 4 years of experience in modelling and management of both Market & Liquidity Risk, with strong focus on ALM, IRRBB and FRTB complemented by technical expertise in Python and SQL. He also has a comprehensive knowledge and experience in regulatory requirements, model validation and Stress Testing. Makram is a certified Financial Risk Manager (FRM).

On 11th January 2024, the European banking authority (EBA) finalized the Implementing Technical Standards (ITS) expanding the Pillar I market risk reporting requirements under the Fundamental Review of the Trading Book (FRTB) framework. The ITS introduce new templates to capture detailed information on the instruments and positions covered in the alternative standardized approach (ASA) and alternative internal model approach (AIMA). The new reporting standards are expected to apply starting 31st March 2025. This article delves into the key components of the recent updates with a focus on the ASA reporting, analyzing their potential implication on financial institutions.

Back in January 2016, the Basel Committee on Banking Supervision (BCBS) released a new standard to determine the Pillar I capital requirement for market risk, which is known as the Fundamental Review of the Trading Book (FRTB). The FRTB was developed as a response to the shortcomings in the regulatory framework following the global financial crisis of 2007-2008. The framework underwent further amendments in 2019 to provide more clarity to the boundaries between books and the treatment of internally transferred instruments for hedging purposes, alongside modifications to the methodology. The primary objective of the FRTB framework is to enhance the comparability and transparency of capital requirements for trading activities across banks and to improve the resiliency of the banking system.

In Europe, the FRTB was first integrated in the prudential framework of the EU in 2019 as part of the Revised Capital Requirements Regulation (CRR II), accounting for specific features of the European banks. Several items (as back-testing, profit and loss attribution, and risk factor modellability) were incorporated in EU law in the following years by means of Regulatory technical standards (RTS) developed by the EBA.

Despite these legislative acts, the FRTB is not binding yet in terms of own funds requirements, as the full implementation is awaiting a political agreement on the CRR3/CDR6-package. Nevertheless, the FRTB has been in force for roughly two years by means of a reporting requirement.

The current reporting requirement are in force since September 2021 and apply only to institutions whose trading book business is above a threshold of EUR 500 million or 10% of total assets. It consists of two templates:

Both templates must be reported on a quarterly basis.

The current summary template provides a high-level breakdown of the ASA own Funds Requirement under the sensitivities-based method (SBM). The decomposition is requested along the seven risk classes (general interest rate risk, equity risk, foreign exchange risk, credit spread risk for non-securitization, ACPT and non-ACPT portfolios), across the three sensitivities used as inputs (delta, Vega, and curvature), and across the three regulatory scenarios (low, medium, and high correlation). Furthermore, the summary provides an overview of the default risk charge (DRC), which aims to measure the jump-to-default risk that may not be estimated through credit spread shocks under the SBM. Lastly, the summary template displays the residual risk add-on (RRAO), which must be computed for all instruments with exotic underlying assets (as longevity or weather) or those with other residual risk (as exotic option payoffs or multi-underlying options subject to correlation risk).

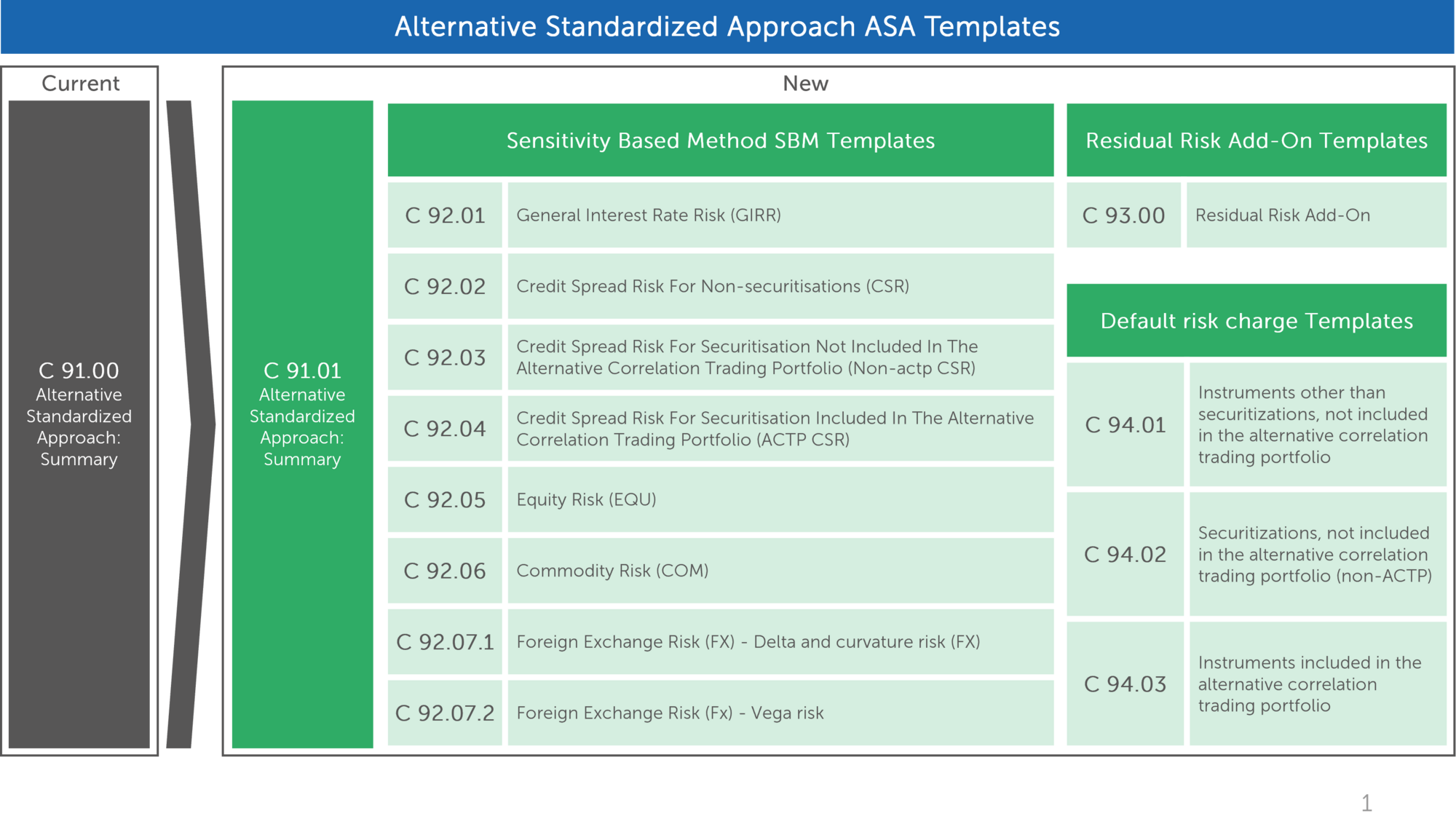

The ITS introduce several changes to the existing ASA summary template, new detailed ASA templates - to be filled by all banks - as well as new AIMA templates for the desks with permission to use to the internal model approach. In addition, the ITS introduce a template capturing information on the reclassification of instruments between the banking and trading books. The trading book thresholds, above which the reporting requirements exist, and the thresholds template (TBT) remain unchanged.

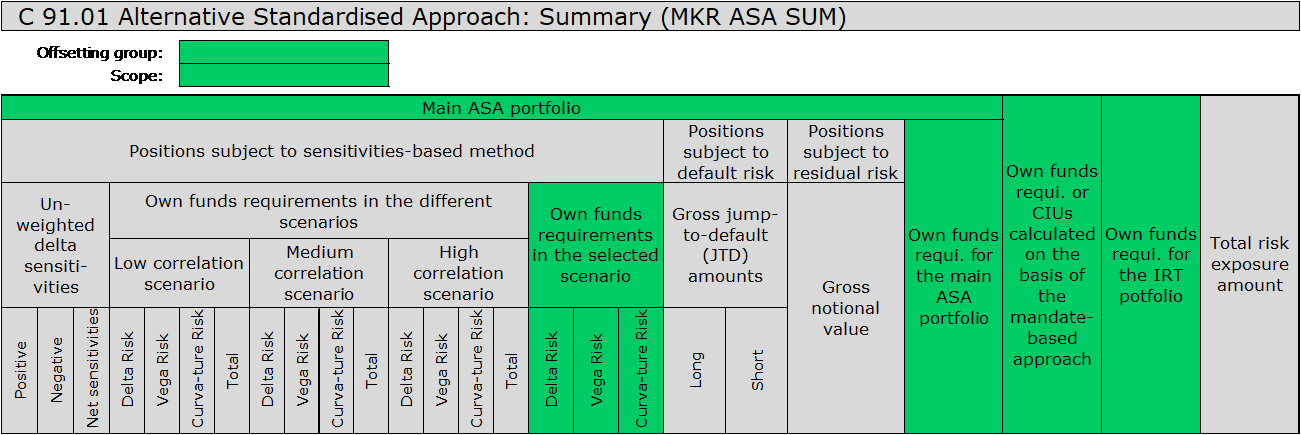

The summary template (“MKR ASA SUM”) sees some limited evolutions. Firstly, columns have been added to input the own fund requirements in the selected correlation scenario. Secondly, the own fund requirements for the “main” ASA portfolio are separated from, firstly, the internal risk transfer portfolio (IRT) used to hedge interest rate risk and, secondly, positions in collective investment undertakings (CIU’s) calculated using mandate-based approach. IRT and mandate based CIU portfolios are treated as standalone positions. Lastly, fields have been added to breakdown the reporting by “offsetting group” and by “scope”, as explained below.

Figure 1: Headers of the ASA Summary templates – new items in green.

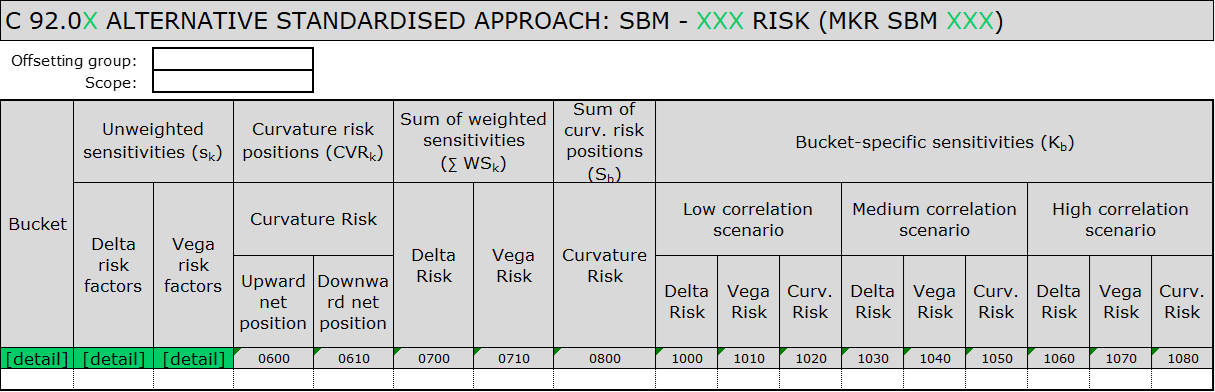

The ITS also introduce twelve new templates providing details regarding the sensitivity-based method (SBM), the residual risk add-on (RRAO) and the default risk charge (DRC). These templates only cover the “main” ASA portfolio: the IRT and mandate based CIU portfolios are exempt from the more granular reporting.

Detailed SBM templates have been added for each of seven risk classes. They have a common structure illustrated in figure 2 below. Financial institutions are requested to provide the detail of the sensitivity to a level that allows the replication of the final calculation, as well as the interim results (weighted sensitivities). The bucketing and the level of detail requested for the (unweighted) sensitivities depends on the risk class and mirrors closely the calculation steps in accordance with the regulation. For example, for the general interest rate risk class (GIRR), for every currency (bucket), delta amounts are broken down per regulatory tenor, except for inflation and cross-currency basis risk positions, which are reported separately as totals. Similarly, for every currency (bucket), GIRR Vega amounts are broken down per option maturity and per underlying residual maturity, and as separate totals for inflation and cross-currency basis.

Figure 2: Headers of the new detailed ASA Summary templates (details in green depend on the risk class)

In the new residual risk add-on template (MKR ASA RRAO), financial institutions are asked to allocate the notional amount of positions subject to residual risk according to the most relevant asset class and the type of residual risk (type of exotic underlying or exotic payoff). A breakdown of the exempted positions (listed, centrally cleared or back-to-back instruments) is also requested according to the type of residual risk).

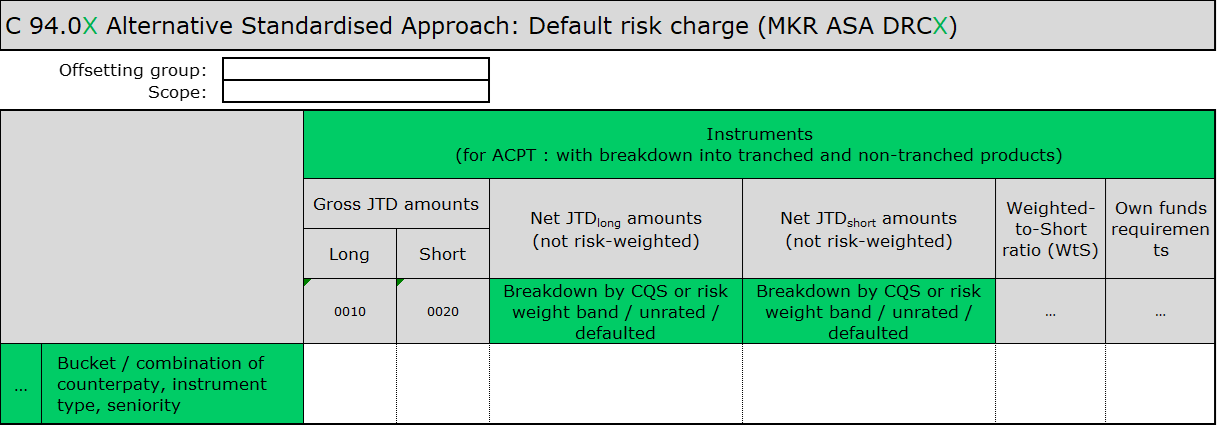

Finally, in the three default risk charge templates (MKR ASA DRC1 to DRC3), financial institutions are requested to break down gross and net jump-to-default amounts by type of instrument and by assumption regarding the LGD as illustrated in figure 3.

Figure 3: Headers of the new detailed ASA DRC templates (details in green depend on whether instrument is securitization, non-ACPT or ACPT)

Note that banks subject to the simplified standard approach that voluntarily apply the ASA have the possibility to only report the ASA summary template, without the remaining more detailed new ASA templates.

Institutions with an AIMA permission must fill the AIMA specific templates listed below, on top of the ASA templates, allowing a comparison between both approaches.

Template root | Description |

MKR AIMA SUM | Summary template giving the expected shortfall (ES) measure and stress scenario (SS) risk measure for modellable and non-modellable risk factors respectively |

MKR AIMA DRC | Two templates breaking down the default risk charge per issuer type according to the PD and the LGD |

MKR AIMA CORR | Two templates zooming on positions in and correlations between the 25 most significant issuers |

MKR AIMA RFET | Result of the risk factor eligibility test |

MKR AIMA SP | Information on stress periods used in the calculation of the stress scenario risk measures (SSRM) |

MKR AIMA DRM | Daily risk measures of ES, SS and DRC |

MKR AIMA PES | Partial expected shortfalls used as an input to the ES measure |

MKR AIMA BTI | Results of the daily back-testing at institution level |

MKR AIMA BTTD | Results of the daily back-testing at trading desk level and P&L attribution test |

MKR AIMA SSRM | Two templates with a breakdown of the stress scenario risk measures and information on the number of risk measures |

MKR AIMA TDS | Information regarding the trading desk structure |

MKR AIMA PL | Daily profit and loss, allocated by risk class |

Most templates contain header fields allowing the breakdown of the reporting by “offsetting group” or by “scope”.

When institutions are authorized to offset positions across entities, these entities are referred to as an 'offsetting group' (OG). The templates must always be filled for the entire banking group, in which case the Offsetting Group field is set to “sum of offsetting group” or simply “single offsetting group” where there is only one offsetting group. The ITS describe conditions under which the templates must additionally be filled at offsetting group level, in which case the field is set to “offsetting group 1”, “offsetting group 2”, etc. This is the case, for example, for any offsetting group consisting of more than one legal entity. Conversely, single entity offsetting groups are exempt from reporting when they contribute for less than 5% of the group own funds requirements, when the offsetting group has an AIMA permission, or when reporting to EU supervisors is already done locally.

The scope field is present on ASA templates only. When institutions have an AIMA permission, the scope field allows them to fill in the ASA templates separately for ASA portfolios and AIMA portfolios (recall that ASA templates must always be filled in for all portfolios for comparison purposes, even those authorized under AIMA). In such cases, the ASA templates are typically filled for 3 different scopes: for the ASA portfolios, the AIMA portfolios, and the consolidated portfolio. Note that when only one offsetting group has an AIMA permission, the AIMA scope is reported only at the consolidated level for the “sum of offsetting group” to avoid repetitions.

Annex VII to the ITS provides practical examples of how these two fields should be used.

CRR2 introduced a revised framework for allocating position to the trading book and the banking book, including documentation and monitoring requirements. The ITS introduce a template (MOV) capturing information regarding the reclassification of instruments between books, including those from preceding reporting periods to the extent the instruments are still “alive”. The requested information includes the date of reclassification, the origin and destination regulatory books, the reason for reclassification, and the impact of the reclassification on own fund requirements. Annexe VI contains several examples of inputs in the MOV template with explanations.

Own funds requirements under ASA must be calculated at least monthly, while calculations in the context of AIMA must be performed more frequently. Reporting on own funds and own funds requirements continues to be reported quarterly, specifically on 31st March 30th June 30th September, and 31st December.

While the changes in the reporting requirements do not alter the main objectives of the regulatory framework, they present a challenge for banks by increasing reporting granularity. The reporting amendments may require further data analysis potentially impacting the data infrastructure, which involves adjustments to the calculation engines to achieve the required level of granularity. At Finalyse we have fine-tuned our excel-based SBM calculation engine to adapt to the latest changes and ensure that our clients meet the regulatory requirements.

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support