Gary is a Principal Consultant within our insurance practice in Dublin. He has 16 years of experience within the life and non-life (re)insurance sectors covering industry, audit and consultancy roles. His expertise covers financial reporting, prudential and conduct risk management, and assurance activities. Gary has provided outsourced actuarial, risk, compliance, and internal audit function services for a wider range of insurers, reinsurers and captives.

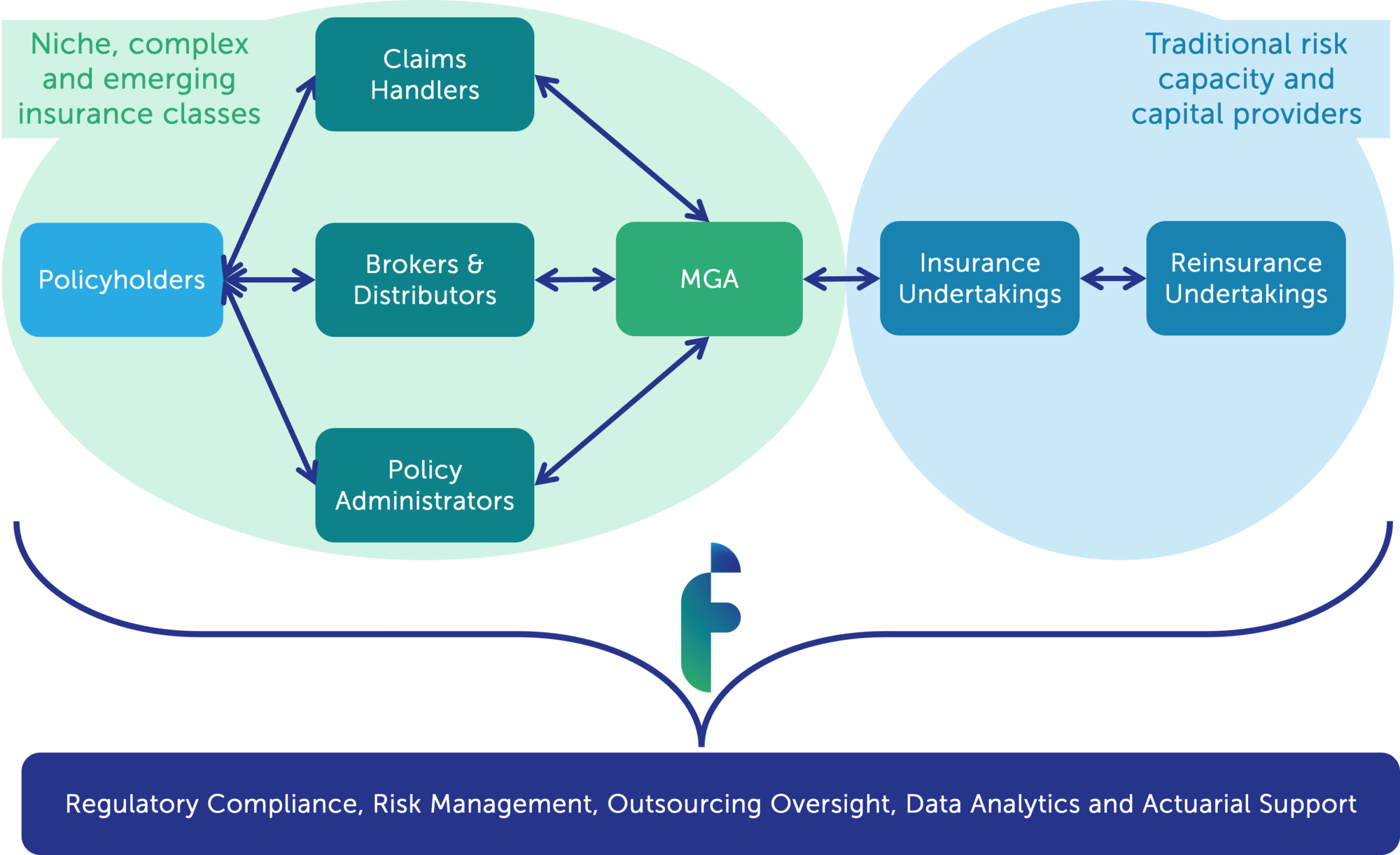

Managing General Agents (MGAs) are specialised intermediaries operating with delegated authority from insurance undertakings. They can underwrite policies, price risks, issue documentation, and sometimes handle claims—all without carrying insurance risk themselves. Instead, they act on behalf of capital providers who supply the underwriting capacity.

Lean, tech-driven, and highly focused, MGAs are reshaping how insurance is underwritten, distributed, and delivered. What began as a workaround for geographic expansion has become a structural shift—particularly in niche, underserved, or fast-evolving markets. For traditional insurers hampered by legacy systems and slow processes, MGAs offer speed, expertise, and relevance.

This article explores the rise of MGAs: their historical roots, what makes the model so attractive today, the risks they face, and their outlook in a transforming insurance landscape.

While the surge in MGA activity is recent, the model itself—partly inspired by the Lloyd’s market—has roots stretching back over a century.

In the U.S., MGA-style entities emerged in the early 1900s as a solution for geographic expansion. Insurers based in the Northeast appointed trusted local agents in the South and West, granting them underwriting and claims-handling authority to bypass licensing and operational challenges of opening full branches.

By the mid-20th century, MGAs had found new purpose in specialist areas like marine, aviation, energy, and high-risk property. By the 2000s, formal delegated authority arrangements became more widespread, bolstered by the global expansion of the Lloyd’s coverholder programme.

In the past 10 to 15 years, technology has been the key accelerant. The rise of InsurTech and growing demand for niche risk transfer solutions has fueled a new wave of MGA activity.

Today, MGAs are no longer just distribution extensions for carriers. They are agile, tech-enabled businesses focused on delivering tailored products and superior service in specific risk segments.

Insurance has traditionally been dominated by large, established players—backed by deep capital reserves, national broker networks, and strong brands. But the 2020s have ushered in an era of specialisation, speed, and software. Large, long-established insurers have suddenly found themselves hampered by structural rigidity and skill misalignment.

Traditional insurers—or risk carriers—operate under layered governance. Launching a new product, even in a familiar space, can take months. MGAs, by contrast, can develop and launch tailored solutions in weeks.

This slow pace leaves incumbents lagging behind fast-evolving risks like cyber, embedded insurance, renewable energy, and tech liability—where the landscape shifts faster than legacy teams can respond.

Most traditional insurers are built for scale, offering broad, standardised products across home, motor, commercial, and liability lines. As a result, solutions are generic and lack the depth needed for niche or emerging risks.

Demand is growing for specialist covers. Drone liability, parametric climate triggers, and digital asset theft are all examples of emerging products that barely existed a few years ago. Building the expertise to underwrite them in-house remains a major challenge for legacy insurers.

Many large insurers still rely on decades-old core systems, creating major roadblocks to innovation and efficiency. Fragmented claims platforms, manual pricing processes, and poor data integration all contribute to weak user experiences and operational drag.

Large carriers tend to be conservative—shaped by heavy regulation, risk aversion, and legacy governance. While this ensures stability, it stifles innovation. MGAs, with lean teams and delegated authority, are freer to experiment, move fast, and iterate their way to market fit.

MGAs thrive where traditional insurers struggle: in complexity, speed, and niche markets.

Recent market and macroeconomic shifts have created ideal conditions for MGAs. First, new capital from private investors and pension funds has flowed into insurance, seeking diversification from traditional equities. This has expanded insurers’ capital capacity.

Second, globalisation, technological advancement, and climate change have widened the global insurance protection gap. Traditional carriers have struggled to keep pace with the growing demand for innovative risk transfer solutions.

MGAs have stepped in to bridge this gap, developing specialised underwriting solutions that connect capital capacity with insurable opportunities. Entrepreneurial founders are building capital-light MGA models using their specialist underwriting knowledge.

MGAs also maintain strong ties to broker networks. Many are spun out of brokerages, giving them built-in distribution, market trust, and access to end customers. This proximity has helped MGAs capitalise on the embedded insurance trend—integrating products into e-commerce, gig economy platforms, and consumer fintech.

Many MGAs resemble tech start-ups more than traditional insurers—operating cloud-native systems that are API-first, broker-integrated, and powered by real-time data. Lean teams and automation-first cultures help drive efficiency. When executed well, MGA models can command high valuation multiples and attractive exits.

In recent years, MGAs have shifted from the margins to the core of the insurance value chain.

The U.S. continues to dominate the global MGA landscape, with the majority of global premium volume concentrated there—estimated at around three-quarters of the market. Sustained double-digit premium growth has pushed annual written volumes past €100 billion.

Europe is smaller but growing. An estimated 650 MGAs operate across the continent, generating a combined €18 billion in annual premiums, according to studies conducted by Howden. The UK leads the region—home to roughly half of all European MGAs and 40% of premiums.

Beyond the UK, the EEA is less mature but gaining ground. Greater regulatory harmonisation is making cross-border operations more attractive.

Italy and the Benelux countries lead the EEA in premium volumes, while Germany, France, Ireland, and the Nordics are seeing strong—if still early-stage—growth.

Outside the U.S. and Europe, global MGA premiums remain modest, at roughly €30 million per year. But emerging markets like China and Brazil are showing real potential.

MGAs have experienced double digit growth across multiple territories

The MGA model is compelling—but not without challenges. Governance concerns, regulatory scrutiny, and limited oversight of claims handling have made some carriers hesitant to provide capacity. MGAs are also vulnerable to underwriting cycles and the difficulty of building long-term relationships with capital providers.

A recent study by the Managing General Agents Association found that nearly half of MGAs—and over a third of carriers—view regulation as the biggest hurdle for new entrants. Most expect scrutiny to increase in the years ahead.

In the UK, many MGAs have struggled with the cost and complexity of complying with the FCA’s Consumer Duty rules, which demand clear evidence of fair value and customer-centric outcomes. In the EU, the Insurance Distribution Directive (IDD) adds further regulatory pressure.

For a sector that prides itself on agility, this move toward more prescriptive oversight has forced both cultural and operational shifts.

As MGAs grow in scale and influence, regulators are sharpening their focus on governance, risk controls, and transparency—especially when MGAs resemble full-stack carriers or InsurTechs.

Claims handling is a persistent pain point. MGAs often outsource it, resulting in chain-outsourcing arrangements that reduce visibility and can compromise service quality for the end customer.

With regulators pushing for better outcomes, both MGAs and carriers are under pressure. According to the Managing General Agents' Association, 77% of MGAs and 91% of carriers cite claims handling as the top area in need of improvement.

Claims remains a key source of tension: MGAs want operational control, while carriers are demanding greater oversight.

MGAs don’t hold their own risk capital. They rely entirely on capacity providers—fronting carriers or reinsurers. If those providers shift strategy, incur losses, or exit the market, MGAs can suddenly lose the ability to write new business.

While longer contracts and stronger relationships are emerging among established players, many smaller MGAs still operate under 90-day termination clauses. During recent hard market conditions, this left some scrambling to renew or expand capacity.

Not all MGAs are created equal. As the market grows, traditional carriers remain wary of new entrants chasing growth at all costs. Without strong governance and oversight, some MGAs may expose their capacity providers to unacceptable risk.

In softer market conditions, the temptation to prioritise premium over discipline increases. But one poor underwriting year can quickly erode trust—and jeopardise future capacity relationships.

Many MGAs promote themselves as data-driven or AI-powered, but delivering on that promise is not always straightforward. Model errors and algorithmic bias aren’t unique to MGAs, but smaller firms often lack the robust controls found in established carriers.

Cybersecurity is another concern. MGAs handle large volumes of sensitive personal data yet may not have the same infrastructure or protections as traditional insurers.

MGAs are facing pressure to mature their risk frameworks

New and complex risks are emerging faster than traditional insurers can respond. MGAs are well-positioned to design agile, specialist cover for areas like cyber, climate, parametric insurance, and AI liability.

Embedded insurance is a particularly fast-growing opportunity. MGAs can integrate coverage directly into the customer journey of non-insurance platforms—something traditional insurers have struggled to execute. Travel, e-commerce, and fintech sectors are actively exploring embedded solutions, while gig worker cover embedded in payroll platforms is another promising example.

With access to IoT, telematics, and behavioural data, MGAs are carving out new niches in usage- and behaviour-based insurance.

Auto insurers have experimented with driving data for years, but newer developments include home insurance linked to smart devices and health cover tied to wearables. Whether these innovations go mainstream or remain niche is unclear—but MGAs are leading the charge, using data to drive pricing, proactive risk management, and better user experiences.

MGAs have the structural flexibility to scale globally—particularly into developing markets where traditional carriers lack presence or appetite. Regions like Africa, Latin America, and Southeast Asia are seeing rising demand for insurance, and digital-first MGAs are responding with mobile-native and parametric products.

Often, they leverage experience from mature markets while partnering with local fronting insurers to navigate licensing barriers and regulatory complexity.

Nearly half of risk carriers increased their MGA capacity over the past year, and over half plan to expand it further within two years, according to the Managing General Agents Association report. One in three carriers are turning to MGAs to grow capabilities in specialty lines, with others expanding into financial and property insurance.

As price adequacy becomes harder to maintain, insurers are leaning on MGAs for their technical expertise, speed, and entrepreneurial edge. In a softening market, agility in underwriting may prove to be a critical advantage.

MGAs are more than a passing trend—they represent a fundamental shift in how insurance is evolving. As traditional carriers wrestle with legacy systems, broad-brush portfolios, and complex governance, MGAs are stepping in with speed, precision, and innovation.

They don’t replace traditional insurers, but they do enhance them—extending reach into risk classes that might otherwise remain untapped.

The U.S. and UK are expected to remain the most mature MGA markets. But Europe is primed for growth. Despite its relative immaturity, a licence to operate in the EEA grants access to 30 jurisdictions—offering MGAs and insurers significant opportunities to scale.

An MGA is a specialised intermediary with delegated authority from insurers to underwrite, price, issue policies, and sometimes handle claims—without carrying insurance risk themselves.

MGAs offer speed, expertise, and flexibility. They use lean teams, modern technology, and close broker relationships to deliver tailored solutions that large insurers often struggle to develop quickly.

While MGAs are growing fast, they face hurdles such as regulatory pressure, reliance on capacity providers, claims handling gaps, and the need to maintain strong underwriting discipline.

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support