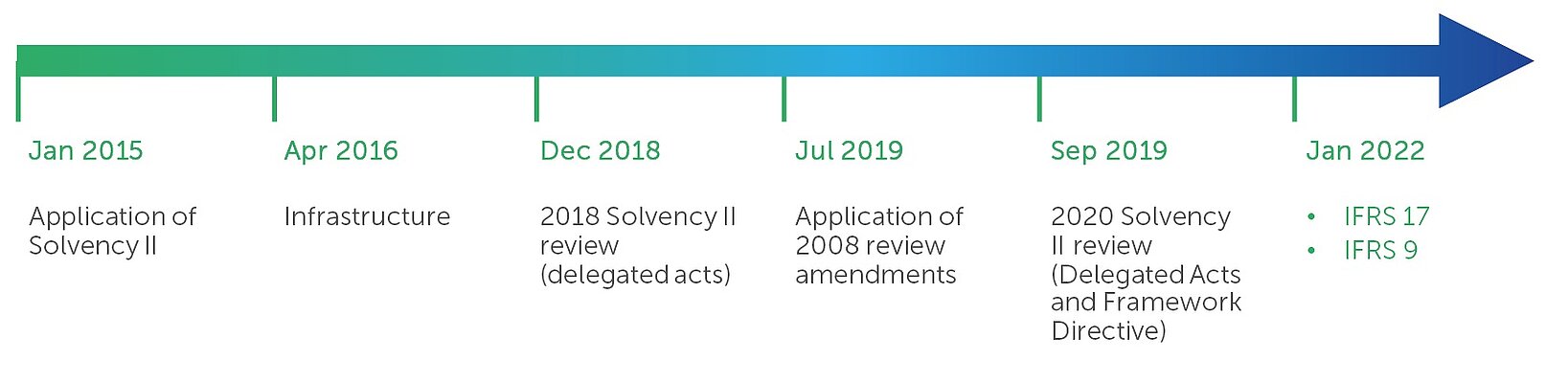

On 18th June 2019, The Official Journal of the EU has adopted a regulation amending Solvency II.

These changes are the results of the 2018 solvency review and aim at:

The vast majority of the amendments will enter into force on the twentieth day following their publication. However, some provisions will only apply as from 1st January 2020.

These are neither the first nor last changes to the Solvency II legislation. In 2016, amendments were adopted to incentivise investments in infrastructure and STS securitisations. Currently, the Commission is in a consultation process which aims at bringing amendments to the Solvency II Directive itself by 2020. This is commonly referred to as the 2020 Solvency II review.

In the annex to this paper, you will find a list of the “2018 Solvency II review” changes, presented in a user-friendly way which should help you navigate the amendments and identify the changes relevant to your organisation in an easier way.

The changes introduced by the “2018 Solvency II review” either replace or amend existing articles of the Delegated Acts or introduce new articles.

The 2018 Solvency II review introduces a significant number of new articles on simplified approaches for the calculation of:

Other new articles brought about by the 2018 Solvency II review have been incorporated in:

The 2018 Solvency II review includes amendments to:

It seems that the amendments brought by the 2018 Solvency II review partly achieve some of their stated objectives, in particular in terms of proportionality, removing inconsistencies between banking and insurance legislation, adjusting the calibration of some insurance risk modules and improving the recognition of insurance risk mitigation techniques.

However, many stakeholders expect more from the 2020 review, in particular in terms of incentivising long-term investments.

Furthermore, although the simplifications introduced for a number of risk modules are useful for many smaller insurers, they may come too late. Indeed, 3 years after the entry into force of Solvency II, it is thought that many of them would have already implemented the more complex approaches included in the Standard Formula.

There is another matter of adjustment for the loss-absorbing capacity of deferred taxes: we wrote a whole paper on this very relevant topic

| Amd # | Chapter | Section | Subsection (if applciable) | Existing Article Title | New Artcile Title | Type of change | Topic |

| 1 | CHAPTER I GENERAL PROVISIONS | SECTION 1 Definitions and general principles | N/A | Article 1 Definitions | N/A | New | Central counterparties (CCPs) |

| 2 | CHAPTER III RULES RELATING TO TECHNICAL PROVISIONS | SECTION 1 General provisions | N/A | Article 18 Boundary of an insurance or reinsurance contract | N/A | Amended | Contract Boundary |

| 3 | CHAPTER III RULES RELATING TO TECHNICAL PROVISIONS | SECTION 4 Relevant risk-free interest rate term structure | Subsection 2 Basic risk free interest rate term structure | Article 46 Extrapolation | N/A | Replaced | Transparency of caluclation of Risk Free Rate Curve |

| 4 | CHAPTER IV OWN FUNDS | SECTION 2 Classification of own funds | N/A | Article 71 Tier 1 — Features determining classification | N/A | Amended | Own Funds |

| 5 | CHAPTER IV OWN FUNDS | SECTION 2 Classification of own funds | N/A | Article 73 Tier 2 Basic own-funds — Features determining classification | N/A | New | Own Funds |

| 6 | CHAPTER IV OWN FUNDS | SECTION 2 Classification of own funds | N/A | Article 77 Tier 3 Basic own-funds– Features determining classification | N/A | New | Own Funds |

| 7 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 1 General provisions | Subsection 1 Scenario based calculations | Subsection 2 Look-through approach | N/A | Amended | Look-through |

| 8 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 1 General provisions | Subsection 6 Proportionality and simplifications | Article 88 Proportionality | N/A | Amended | Proportionality |

| 9 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 1 General provisions | Subsection 6 Proportionality and simplifications | N/A | Article 90a Simplified calculation for discontinuance of insurance policies in the non-life lapse risk sub-modul | New | Simplification |

| Article 90b Simplified calculation of the sum insured for natural catastrophe risks | New | Simplification | |||||

| Article 90c Simplified calculation of the capital requirement for fire risk | New | Simplification | |||||

| 10 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 1 General provisions | Subsection 6 Proportionality and simplifications | Article 91 Simplified calculation of the capital requirement for life mortality risk | N/A | Amended | Simplification |

| 11 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 1 General provisions | Subsection 6 Proportionality and simplifications | N/A | Article 95a Simplified calculation of the capital requirement for risks in the life lapse risk sub-module | New | Simplification |

| 12 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 1 General provisions | Subsection 6 Proportionality and simplifications | N/A | Article 96a Simplified calculation for discontinuance of insurance policies in the NSLT health lapse risk sub-module | New | Simplification |

| 13 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 1 General provisions | Subsection 6 Proportionality and simplifications | Article 97 Simplified calculation of the capital requirement for health mortality risk | N/A | Amended | Simplification |

| 14 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 1 General provisions | Subsection 6 Proportionality and simplifications | N/A | ‘Article 102a Simplified calculation of the capital requirement for risks in the SLT health lapse risk sub-module | New | Simplification |

| 15 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 1 General provisions | Subsection 6 Proportionality and simplifications | N/A | ‘Article 105a Simplified calculation for the risk factor in the spread risk sub-module and the market risk concentration sub-module | New | Simplification |

| 16 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 1 General provisions | Subsection 6 Proportionality and simplifications | Article 107 Simplified calculation of the risk mitigating effect for reinsurance arrangements or securitisation | N/A | Replaced | Recognition of Reinsurance |

| 17 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 1 General provisions | Subsection 6 Proportionality and simplifications | Article 108 Simplified calculation of the risk mitigating effect for proportional reinsurance arrangements | N/A | Replaced | Recognition of Reinsurance |

| 18 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 1 General provisions | Subsection 6 Proportionality and simplifications | Article 110 Simplified calculation — grouping of single name exposures | Article 110 Simplified calculation — grouping of single name exposures | Replaced | Concentration Risk |

| 19 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 1 General provisions | Subsection 6 Proportionality and simplifications | Article 111 Simplified calculation of the risk mitigating effect | N/A | Replaced | Recognition of Reinsurance |

| 20 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 1 General provisions | Subsection 6 Proportionality and simplifications | N/A | Article 111a Simplified calculation of the risk-mitigating effect on underwriting risk | New | Simplification / Recognition of Reinsurance |

| 21 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 1 General provisions | Subsection 6 Proportionality and simplifications | N/A | ‘Article 112a Simplified calculation of the loss-given-default for reinsurance | New | Simplification / Recognition of Reinsurance |

| Article 112b Simplified calculation of the capital requirement for counterparty default risk on type 1 exposure | New | Simplification | |||||

| 22 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 2 Non-life underwriting risk module | N/A | Article 115 Non-life premium and reserve risk sub-module | N/A | Replaced | Future Premiums in the Non-Life UW risk SCR |

| 23 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 2 Non-life underwriting risk module | N/A | Article 121 Windstorm risk sub-module | N/A | Amended | Windstrom risk SCR |

| 24 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 2 Non-life underwriting risk module | N/A | Article 122 Earthquake risk sub-module | N/A | Amended | Earthquake risk SCR |

| 25 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 2 Non-life underwriting risk module | N/A | Article 123 Flood risk sub-module | N/A | Amended | Flood risk SCR |

| 26 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 2 Non-life underwriting risk module | N/A | Article 124 Hail risk sub-module | N/A | Amended | Hail risk SCR |

| 27 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 2 Non-life underwriting risk module | N/A | Article 125 Subsidence risk sub-module | N/A | Amended | Subsidence risk SCR |

| 28 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 2 Non-life underwriting risk module | N/A | Article 130 Marine risk sub-module | N/A | Replaced | Marine risk sub-module |

| 29 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 2 Non-life underwriting risk module | N/A | Article 131 Aviation risk sub-module | N/A | Amended | Aviation Risk SCR |

| 30 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 2 Non-life underwriting risk module | N/A | Article 132 Fire risk sub-module | N/A | Replaced | Fire Risk SCR |

| 31 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 4 Health underwriting risk module | N/A | Article 147 Volume measure for NSLT health premium and reserve risk | N/A | Replaced | Future Premiums in the Non-Life UW risk SCR |

| 32 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 5 Market risk module | Subsection 3 Equity risk sub-module | Article 168 General provisions | N/A | Amended | Investments in Funds |

| 33 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 5 Market risk module | Subsection 3 Equity risk sub-module | N/A | ‘Article 168a Qualifying unlisted equity portfolios | New | Equity Risk SCR |

| 34 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 5 Market risk module | Subsection 3 Equity risk sub-module | Article 169 Standard equity risk sub-module | ‘Article 169 Standard equity risk sub-module | Replaced | Equity Risk SCR |

| 35 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 5 Market risk module | Subsection 3 Equity risk sub-module | N/A | ‘Article 171a Long-term equity investments | New | Equity Risk SCR |

| 36 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 5 Market risk module | Subsection 5 Spread risk sub-module | Article 176 Spread risk on bonds and loans | N/A | New | Spread Risk SCR |

| 37 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 5 Market risk module | Subsection 5 Spread risk sub-module | N/A | Article 176a Internal assessment of credit quality steps of bonds and loans | New | Spread Risk SCR |

| Article 176b Requirements for an undertaking's own internal credit assessment of bonds and loans | New | Spread Risk SCR | |||||

| Article 176c Assessment of credit quality steps of bonds and loans based on an approved internal model | New | Spread Risk SCR | |||||

| 38 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 5 Market risk module | Subsection 5 Spread risk sub-module | Article 180 Specific exposures | N/A | Amended | Spread Risk SCR |

| 39 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 5 Market risk module | Subsection 6 Market risk concentrations sub-module | Article 182 Single name exposure | N/A | New | Spread Risk SCR |

| 40 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 5 Market risk module | Subsection 6 Market risk concentrations sub-module | Article 184 Excess exposure | N/A | Replaced | Concentration Risk |

| 41 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 5 Market risk module | Subsection 6 Market risk concentrations sub-module | Article 186 Risk factor for market risk concentration | N/A | Deletion | Concentration Risk |

| 42 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 5 Market risk module | Subsection 6 Market risk concentrations sub-module | Article 187 Specific exposures | N/A | Amended | Spread Risk SCR |

| 43 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 5 Market risk module | Subsection 7 Currency risk sub-module | N/A | Amended | Currency Risk SCR | |

| 44 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 6 Counterparty default risk module | Subsection 1 General provisions | Article 192 Loss-given-default | N/A | Amended | Counterparty Default Risk |

| 45 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 6 Counterparty default risk module | Subsection 1 General provisions | N/A | ‘Article 192a Exposure to clearing members | New | Counterparty Default Risk |

| 46 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 6 Counterparty default risk module | Subsection 1 General provisions | Article 196 Risk-mitigating effect | ‘Article 196 Risk-mitigating effect | Replaced | Recognition of Reinsurance |

| 47 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 6 Counterparty default risk module | Subsection 1 General provisions | Article 197 Risk-adjusted value of collateral | N/A | Amended | Counterparty Default Risk |

| 48 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 6 Counterparty default risk module | Subsection 2 Type 1 exposures | Article 199 Probability of default | N/A | New | Counterparty Default Risk |

| 49 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 6 Counterparty default risk module | Subsection 2 Type 1 exposures | Article 201 Variance of the loss distribution of type 1 exposures | N/A | Replaced | Counterparty Default Risk |

| 50 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 9 Adjustment for the loss-absorbing capacity of technical provisions and deferred taxes | N/A | Article 207 Adjustment for the loss-absorbing capacity of deferred taxes | N/A | Amended | Deferred Taxes |

| 51 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 10 Risk mitigation techniques | N/A | Article 208 Methods and Assumptions | N/A | Replaced | Recognition of Reinsurance |

| 52 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 10 Risk mitigation techniques | N/A | Article 209 Qualitative Criteria | N/A | Replaced | Recognition of Reinsurance |

| 53 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 10 Risk mitigation techniques | N/A | Article 210 Effective Transfer of Risk | N/A | New | Recognition of Reinsurance |

| 54 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 10 Risk mitigation techniques | N/A | Article 211 Risk-Mitigation techniques using reinsurance contracts or special purpose vehicles | N/A | Amended | Recognition of Reinsurance |

| 55 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 10 Risk mitigation techniques | N/A | Article 212 Financial Risk-Mitigation techniques | N/A | Replaced | Recognition of Reinsurance |

| 56 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 10 Risk mitigation techniques | N/A | Article 213 Status of the counterparties | N/A | Replaced | Recognition of Reinsurance |

| 57 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 12 Undertaking-specific parameters | N/A | Article 218 Subset of standard parameters that may be replaced by undertaking-specific parameters | N/A | Amended | Recognition of Reinsurance |

| 58 | CHAPTER V SOLVENCY CAPITAL REQUIREMENT STANDARD FORMULA | SECTION 12 Undertaking-specific parameters | N/A | Article 220 Standardised methods to calculate the undertaking-specific parameters | N/A | Replaced | Recognition of Reinsurance |

| 59 | CHAPTER IX SYSTEM OF GOVERNANCE | SECTION 1 Elements of the system of governance | N/A | Article 260 Risk management areas | N/A | New | Deferred Taxes |

| 60 | CHAPTER XII PUBLIC DISCLOSURE | SECTION 1 Solvency and financial condition report: structure and contents | N/A | Article 297 Capital management | N/A | Amended | Deferred Taxes |

| 61 | CHAPTER XIII REGULAR SUPERVISORY REPORTING | SECTION 1 Elements and contents | N/A | Article 311 Capital management | N/A | Amended | Deferred Taxes |

| 62 | CHAPTER XV SPECIAL PURPOSE VEHICLES | SECTION 5 Solvency requirements | N/A | Article 326 Solvency requirements | N/A | Replaced | SPV |

| 63 | TITLE II INSURANCE GROUPS : CHAPTER I SOLVENCY CALCULATION AT GROUP LEVEL | SECTION 2 Group solvency: calculation methods | N/A | Article 335 Method 1: determination of consolidated data | N/A | Amended | Investments in Funds |

| 64 | TITLE II INSURANCE GROUPS : CHAPTER I SOLVENCY CALCULATION AT GROUP LEVEL | SECTION 2 Group solvency: calculation methods | N/A | Article 336 Method 1: Calculation of the consolidated group Solvency Capital Requirement | N/A | Amended | Investments in Funds |

| 65 | TITLE II INSURANCE GROUPS : CHAPTER I SOLVENCY CALCULATION AT GROUP LEVEL | SECTION 2 Group solvency: calculation methods | N/A | Article 337 Method 1: determination of the local currency for the purposes of the currency risk calculation | N/A | Replace | Currency Risk SCR |

| 66 | Annexes | Annex II | N/A | N/A | N/A | Replaced | Calibration of NL risk SCR |

| 67 | Annexes | Annex III | N/A | N/A | N/A | Amended | ANNEX III FACTOR FOR GEOGRAPHICAL DIVERSIFICATION OF PREMIUM AND RESERVE RISK |

| 68 | Annexes | Annex V | N/A | N/A | N/A | Replaced | Calibration of Windstorm risk SCR |

| 69 | Annexes | Annex VI | N/A | N/A | N/A | Amended | Calibration of Earthquake risk SCR |

| 70 | Annexes | Annex VII | N/A | N/A | N/A | Amended | Calibration of Flood risk SCR |

| 71 | Annexes | Annex VIII | N/A | N/A | N/A | Replaced | Calibration of Hail risk SCR |

| 72 | Annexes | Annex IX | N/A | N/A | N/A | Amended | Geographical Risk Zones for CAT risks |

| 73 | Annexes | Annex X | N/A | N/A | N/A | Replaced | Calibration of Windstorm, Earthquake, Flood and Hail risks SCR. |

| 74 | Annexes | Annex XIV | N/A | N/A | N/A | Amended | Calibration of Health risk SCR |

| 75 | Annexes | Annex XVI | N/A | N/A | N/A | Amended | Calibration of MASS ACCIDENT RISK SUB-MODULE AND ACCIDENT CONCENTRATION RISK SUB-MODULE |

| 76 | Annexes | Annex XVII | N/A | N/A | N/A | Amended | Non-proportional reinsurance method 2 - Input data and method-specific data requirements |

| 77 | Annexes | Annex XXI | N/A | N/A | N/A | Amended | ANNEX XXI AGGREGATE STATISTICAL DATA |

| 78 | Annexes | Annex XXII | N/A | N/A | N/A | Amended | ‘Correlation coefficients for windstorm risk in the Republic of Finland, in the Republic of Hungary, in the Kingdom of Sweden and in the Republic of Slovenia. |

| 79 | Annexes | Annex XXIII | N/A | N/A | N/A | Amended | Correlation coefficients for earthquake risk in the Hellenic Republic, in the Republic of Romania and in the Slovak Republic. |

| 80 | Annexes | Annex XXIV | N/A | N/A | N/A | Amended | Correlation coefficients for flood risk in the Republic of Hungary ane in the United Kingdom of Great Britain and Northern Ireland. |

| 81 | Annexes | Annex XXV | N/A | N/A | N/A | Amended | Correlation coefficients for hail risk in the Czech Republic and in the Republic of Slovenia. |

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support