Related Articles

How Finalyse can help

IFRS 9 financial instruments

The impairment methodology is forward-looking, requiring the reporting entity to report the changes in credit risk of financial institutions in a consistent way with the credit risk measurement methods. Particularly, banks will move from 1 year EL to Lifetime EL.

Finalyse can assist you by bringing our expertise in Risk Management and the fields of Credit Risk Modelling, Accounting and Performance Measurement by implementing the 3-stage model in your computational and reporting streams, to fulfil IFRS 9 requirements in a timely manner.

How does Finalyse address your challenges?

Guidance in the implementation of the 3-stage model for impairments

Proven know-how in credit risk measurement and advanced modelling techniques delivered by seasoned experts

Common interpretation of methodology and guaranteed compliance

Assistance in building a robust reporting stream for the disclosures of your loan loss allowances

Assistance in choosing one of the three approaches that will differ in assessing impairment requirements

A full monitoring of IFRS 9 impacts for P&L and capital planning purpose

Key Features

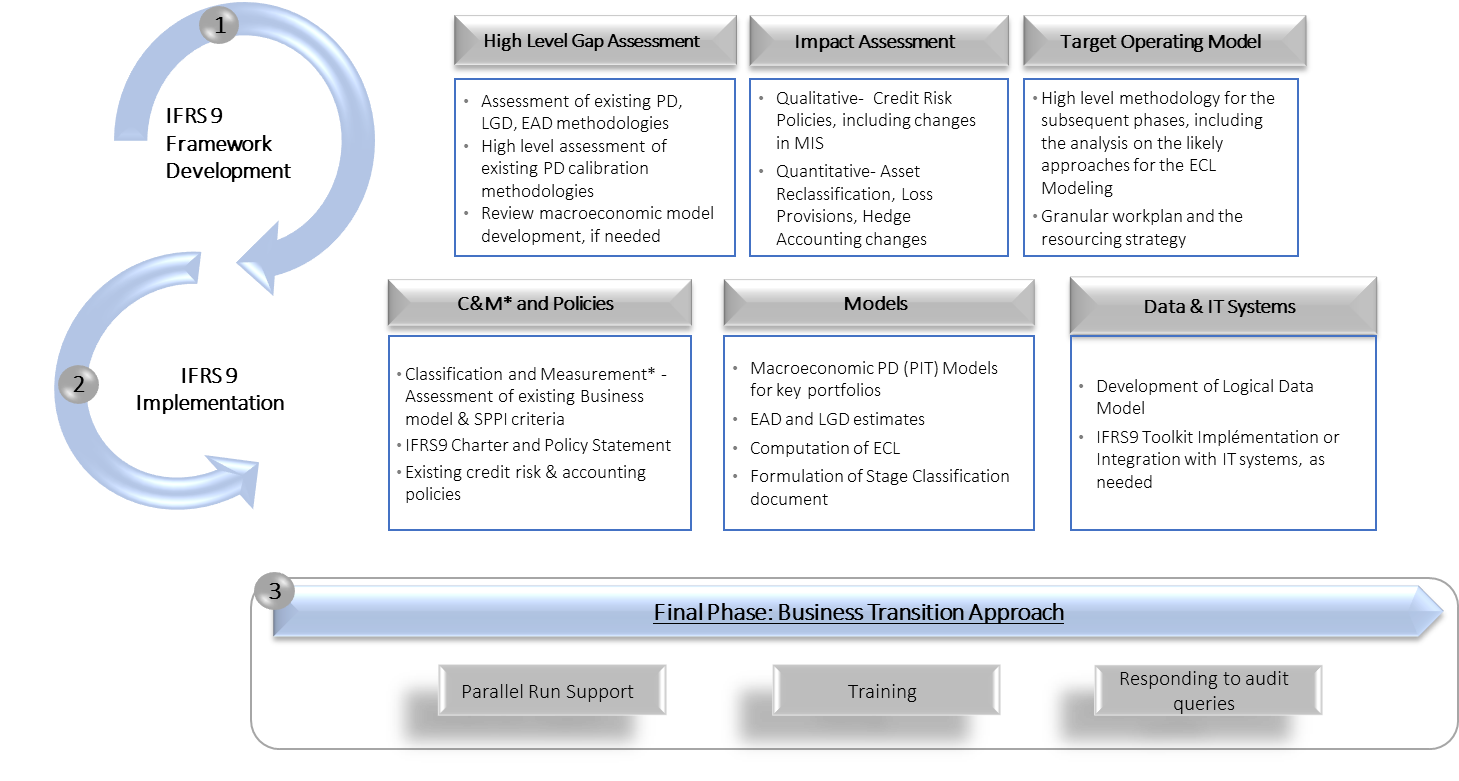

- Finalyse would design an IFRS 9 framework catering to the bank’s needs comprising of a High-level gap report, Target Operating Model and an Impact Assessment.

- During the IFRS 9 implementation phase, Finalyse would focus on the different aspects of Impairment modelling and Expected Credit Losses (ECL) estimation. The classification and measurement of IFRS 9 instruments (as per the SPPI tests) and IFRS 9 Policy documents could also be reviewed/updated as part of this exercise.

- Finalyse would also support in the Business Transition phase and ensure the IT/Systems are fully integrated in the parallel run.