Reviewed by Abishek Chopra, Principal Consultant • Risk Advisory for Banking

On January 1, 2025 the CRR3 went into legal force for most member states of the EU. Of particular consequence is the treatment of mortgage guarantees. A significant portion of the Dutch mortgage market is protected by the so called “Nationale Hypotheek Garantie” (NHG), or national mortgage guarantee. A common practice is to take the NHG into account in the IRB model as a risk driver or calibration segment. However, treating the NHG as Credit Risk Mitigation simplifies the model and leads to favourable risk weights, while also accurately reflecting the credit risk. Treating the NHG as a CRM brings along subtle but important issues.

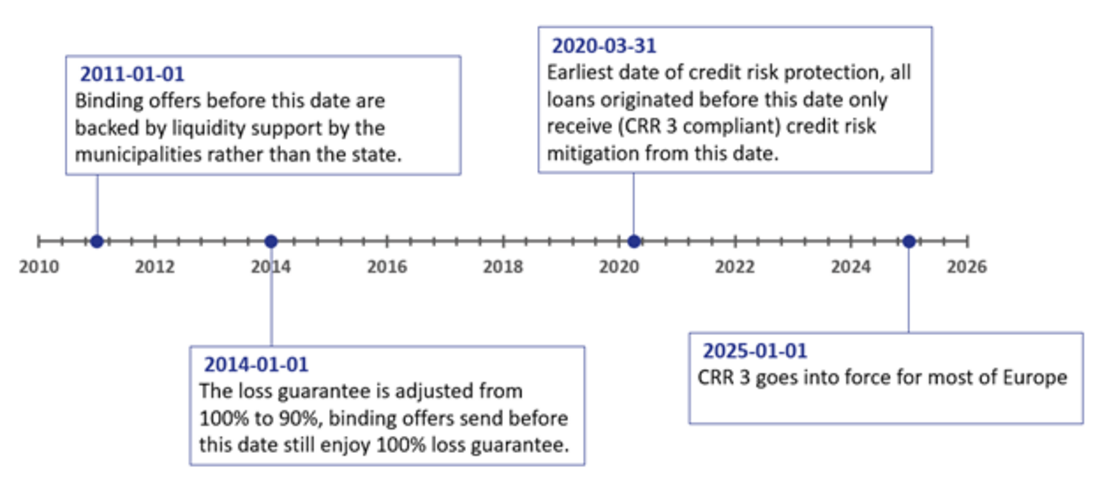

NHG is a guarantee that covers 100% (for loans for which the final offer is sent before January 2014) or 90% (for all other loans, see B.1.5 of [1]) of all residual debt after a default. NautaDutilh has tested the legal viability of the NHG and found it qualifies as credit risk protection for the CRR (see [2]). The NHG is provided by the organization WEW an organ of the Dutch state. WEW in turn is financially guaranteed (by the so called “back stop agreement”) by the municipalities relevant to the mortgage (for loans with guaranteed by NHG before 2011-01-01, see [3]), or the Dutch state directly (for the loans guaranteed by NHG later than 2011-01-01). This back stop agreement has also been tested by NautaDutilh and qualifies as CRR compliant credit risk protection. Finally, Dutch municipalities are considered a local government that are treated as exposures to the central government (see [4]). Therefore, mortgages that are protected by NHG benefit from a favorable reduction in risk weights when treated as CRM. The standardized risk weight for the Dutch central government, as well as its municipalities is 0%.

The B1 section of terms and conditions was updated in 2020 to reflect the obligation of NHG to pay out. This means that the date at which the CRM starts is 31st of March 2020 at the earliest (even for loans with NHG originating before this date), see [1].

Using the standardised risk weight for the CRM and the A-IRB approach for the real estate exposure, taking care not to double count the NHG during modelling, leads to the lowest Risk Weights as well as the most accurate assessment of the credit risk. The substitution approach allows the calculation of risk weighted exposure amount (RWEA) using the standardised risk weighting of the guarantor. The typical case that we will examine is a bank that has a real estate portfolio using the IRB approach and no IRB model for Public Sector Entities or Central Governments. In these cases, article 235(a) of the CRR gives the following formula:

where:

the exposure value with the credit conversion factor (CCF) set at 100%;

the exposure value with the credit conversion factor (CCF) set at 100%;

the amount of credit protection adjusted for foreign exchange risk, we will assume no foreign exchange risk for this article, this number will be 90% or 100% of the exposure depending on the date the loan was offered to the client;

the amount of credit protection adjusted for foreign exchange risk, we will assume no foreign exchange risk for this article, this number will be 90% or 100% of the exposure depending on the date the loan was offered to the client;

the IRB risk weight of the guaranteed exposure;

the IRB risk weight of the guaranteed exposure;

the standardised risk weight for the guarantor.

the standardised risk weight for the guarantor.

As the section above outlined the g in this formula should be set at 0%. For a NHG exposure of €400.000 with 10 percent IRB risk weight, that originated after 2014, the formula would reduce the RWEA to 1% of €400.000 or €4.000. Please refer to this article for details on how the standardised real estate risk weights work under CRR3.

The biggest risk is the double counting of the NHG effects in IRB model and in the risk substitution. Banks need to take extreme care not to take into the effects of NHG in either the development of their IRB models (both PD and LGD). Even if NHG is not taken into account directly as a risk driver or calibration segment the supervisor could still flag the LGD model as already using the effect of NHG, if the cash flows are taken into account during modelling or calibration.

The EBA guidelines on CRM for IRB (see [5], paragraph 35(a)) sees simply using the effects of the unfunded credit protection (NHG) on realised LGDs as already opting for the modelling approach rather than the substitution approach. This would mean that when cashflows of NHG are considered during the LGD calibration, the substitution approach can no longer be used, if the supervisor maintains the strictest standards on double counting.

There are some additional smaller pitfalls in the application:

Below we provide a simple example of a filled out COREP using the loan splitting approach, such a calculation would be done for the output floor or a standardised exposure. We make the choice to (conservatively) assign all the exposure not covered by the NHG to the unsecured (75% risk weight) tranche, although other approaches can be defended.

Characteristic | Value |

Market Value | 100,000 |

Exposure amount | 95,000 |

Unsecured part | 40,000 |

Secured before Eigen Risico | 55,000 |

Eigen Risico | 9,500 |

NHG | 85,500 |

Table 1: Loan characteristics

The COREP C7 would be filled in for our example loan as follows, also showing the inflow for central governments and central banks.

Exposure class | Exposure | 0% | 20% | 75% | CRM Unfunded credit protection | Outflow | inflow | Net exposure after CRM | RW |

Secured by mortgages on residential immovable property (non-IPRE) | 95,000 | - | - | 9,500 | 85,500 | 85,500 | - | 9,500 | 7,125 |

Central Governments or Central Banks | 85,500 | 85,500 |

Table 2: example COREP

The approach in this article is made possible by the introduction of CRR article 235a in CRR3. This article introduces the hybrid IRB (for the guaranteed exposure) and SA (for the guaranteeing party) approach. In the table below Table 3 the regulatory citations are laid out.

| Regulation | Impact |

CRR article 108 | Under paragraph 3, the credit risk mitigation is to be applied in the case of IRB exposure and SA guarantor. |

CRR article 213-215 | Nautadutilh has tested NHG and found it meeting the standards set out in CRR articles 213-215. In addition, the backstop agreement is also valid credit mitigation for CRR articles 213-215. This means NHG qualifies as Unfunded Credit Protection. |

CRR article 115, 114 EBA list under Article 115(2) of Regulation (EU) 575/2013 | Dutch municipalities are to be treated as exposures to Central Governments. Exposure to the Dutch Central Government shall be assigned a risk weight of 0%. |

CRR article 235a | Article 235a originates the formula used in the substitution approach. |

NHG terms and conditions B1.1 | The inception date for the CRM guarantee is 31st march 2020 at the earliest. |

Table 3: regulatory citations

CRR 3 has profound impact on the IRB modelling landscape and credit risk calculation. Seemingly small changes in the CRR can lead to big changes in capital calculation. With years of experience in implementing and validating CRR and Basel 4 across the world, Finalyse can help you deliver and validate a CRR 3 compliant capital calculation.

[1] NHG, Voorwaarden en normen 2025-1, 2025.

[2] Nautadutilh, Eligibility of National Mortgage Guarantee as credit protection under the CRR.

[3] NHG, www.nhg.nl/over-nhg/stakeholders/.

[4] EBA, List of EU regional governments and local authorities treated as exposures to central governments (Article 115 CRR).

[5] EBA, Guidelines on credit risk mitigation for institutions.

Article 235(a) is introduced, allowing banks to apply CRM for which they only have a Standardized risk weights to exposures that are risk weighted with IRB.

The NHG is Unfunded Credit Protection, in this category it is a “guarantee”

Yes, although for this case the introduction of CRR article 235(a) did not change anything.

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support