Simulation-driven capital floor optimisation

Designed to meet CRR amd CRD regulatory requirements for banks

How to maximize business value when implementing increasing regulatory-driven data management requirement?

By Abishek Chopra, Senior Consultant

Banks in the European Union are facing a unique predicament these days – between complying with the existing regulatory reporting practices (w.r.t CRD IV and Basel III), and preparing for the upcoming Basel IV norms (to be adopted by January 20221) and the latest EU Capital Requirements Regulations (CRD5/CRR2 directives and guidelines on other topics such as prudential backstop).

While enough resources are available online to deconstruct the upcoming regulations (more so from the Basel IV side), banks are still struggling to cope with the data requirements from a practical implementation point of view. This blog aims to simplify the critical data elements needed in order to be ready for a Basel IV implementation program (focusing on credit risk).

1 BCBS D424: Basel III: Finalising post-crisis reforms. One point to note here is that although the BCBS still calls this “Basel III”, in common banking parlance these are referred to as Basel IV guidelines.

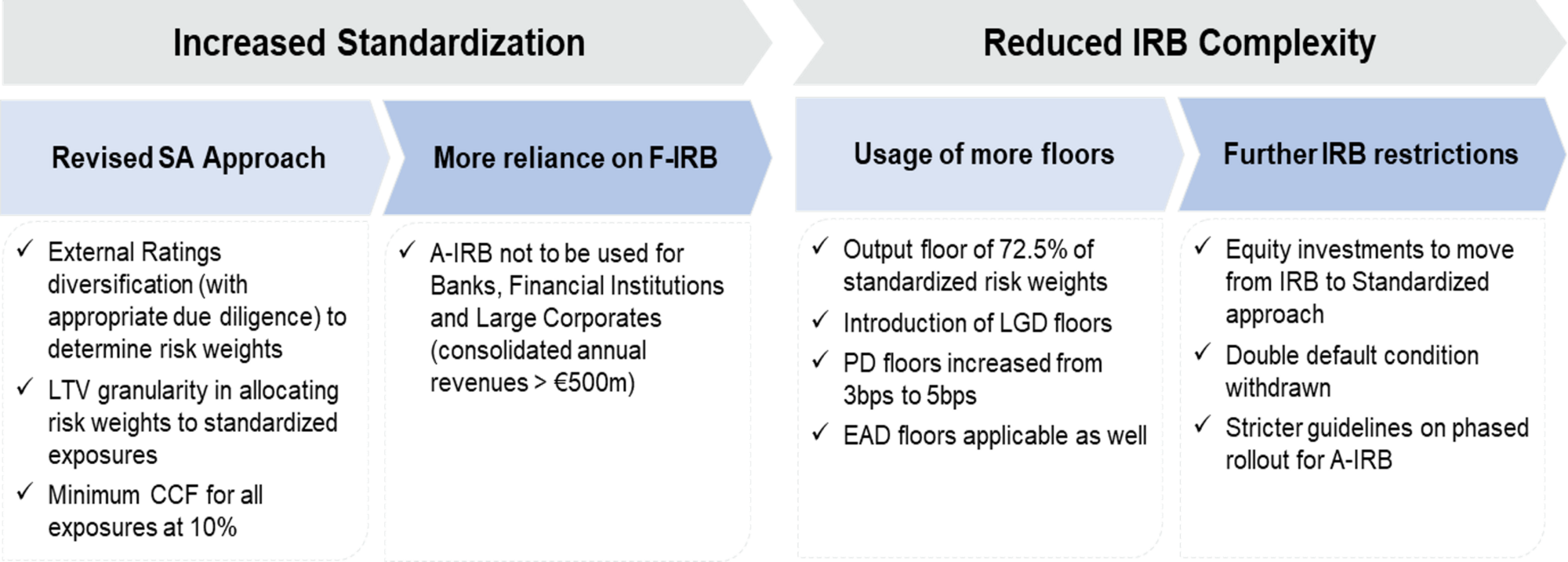

The aim of the guidelines is to reduce complexity and harmonize the calculation techniques from Basel III. The Standardized Approach has been revised to become more risk sensitive and the IRB Approach has been constrained to make it less complex (with the application of the 72.5% RWA Floor). These would mitigate the effect of operational and measurement errors in the model estimation, and eventually narrow the gaps between different banks on the standardized approaches vs. advanced approaches.

Here is a high-level summary of the guidelines:

Data sourcing is one of the most important aspects for any bank when it comes to adopting a new regulation. Of course, these are subjective, based on the bank’s system capabilities and priorities for implementation. For instance, a small bank may already be following the standardized approach for most of its portfolios, and therefore, the impact of the new BCBS regulations would be minimal and only focused on parameters which affect those derivations (collateral and LTV ratio calculations, etc.).

Some of the most critical data elements which banks must account for, during their Basel IV implementation, are described in the sections below. Please note that these data requirements have only been taken into consideration for application in the Corporate, Banks/Financial Institutions and Retail portfolios (further requirements can be analyzed for the implementation of Counterparty Credit Risk (SA-CCR), Specialized Lending (w.r.t slotting approaches), and other smaller portfolios (Equity, Covered Bonds, Other Assets, etc.)).

They are critical to reduce risk weights under the revised standardized approach for high rated corporates and banks.

Corporates: For corporate exposures, base risk weights are to be assigned as per the table below2.

2 The presumption being that European banks fall under the jurisdiction which allows the use of external ratings for regulatory purposes. Consequently, an “investment grade” indicator would not be significant for data requirements.

External rating of counterparty | AAA to AA– | A+ to A– | BBB+ to BBB– | BB+ to BB– | Below BB– | Unrated |

“Base” risk weight | 20% | 50% | 75% | 100% | 150% | 100% |

The differences between Basel III and Basel IV regulations are captured in bucket 3 above (BBB+ to BBB-), where the risk weights have been reduced from 100% to 75%. The majority of the current Corporate exposures for European banks would qualify for this bracket with risk weights ranging between 90% to 100%.

Therefore, it is extremely important for banks to ensure that the respective business entities maintain the external ratings information accurately.

Banks and Financial Institutions: In addition to the External Credit Risk Assessment Approach (ECRA), a Standardized Credit Risk Assessment Approach (SCRA) has been defined and can be particularly applicable for unrated bank exposures (while the rated bank exposures comply with the ECRA approach). More granularity has been added for the risk weight buckets, and it would be prudent for banks to source accurate and complete external ratings for their bank/FI exposures.

Additionally, external ratings would be relevant for banks following the IRB approach for their portfolios since now they have to benchmark their RWA with the output floor.

The right collateral data can make a phenomenal difference in ensuring the correct credit risk mitigation and thereby reducing the risk-weighted assets (RWA) to an optimal value for the bank.

Exposures secured by Commercial Real Estate (CRE) and Residential Real Estate (RRE) now have more granular risk weights corresponding to their LTV buckets (further classified by income producing real estate).

A key part of the Basel IV regulation is that banks must use the collateral value at origination to compute their LTV ratios (unless national supervisors decide to require banks to revise the property value downward). 3

3 BCBS D424: Page 20, paragraph 62

However, banks currently develop their LGD models (for AIRB approach exposures; mostly retail) using the latest collateral values. Therefore, banks will have to ensure that they now also source the value of the property at origination. This can be tricky for banking portfolios other than Mortgages, and banks must have proper sourcing mechanisms in place so that the correct transaction-level collateral is fetched by all business units. Transaction-level collateral is already important from the application of Standardized and FIRB approaches (to get updated LGDs based on secured-unsecured splits).

One possible synergy that could be achieved (for an ideal state) is the usage of the same collateral data for both the IFRS 9 and Basel IV calculation processes.

For off-balance sheet exposures, the CCF is used to derive the Exposure-at-Default (EAD) that would be used in the RWA and Expected Credit Losses (ECL) calculations. The applicable CCF is a percentage determined by mapping the off-balance component to regulatory product types.

In Basel IV, the minimum CCF values have now been revised from 0% to 10% for commitments that are unconditionally cancellable at any time by the bank without prior notice, or that effectively provide for automatic cancellation due to deterioration in a borrower’s creditworthiness . 4

4 BCBS D424: Section for Off-Balance Sheet items, page 158

It is critical that the correct CCF values are maintained in the bank databases as they could have a huge impact on the resultant EAD. Risk of misclassification would result in an under- or overstating EAD. The use of the minimum 10% CCF is at risk when the supervisor determines that the contractual conditions to use 10% CCF are not met in practice.

Moreover, as stated for section 3.1, banks following the IRB approach would also have to maintain CCFs to constrain their outputs to the standardized RWA floors.

All business lines should therefore ensure that the correct off-balance sheet product codes are mapped for all the different product types (resulting in the correct CCF application).

In Basel IV, an 85% risk-weight has been introduced for unrated Corporates which classify as Small & Medium Enterprises (SMEs)5 , as opposed to 100%.

This benefit of the SME identification for a corporate can be nullified if the data for classifying SMEs as such is not available. Most banks do not have sufficient/accurate information when it comes to client annual consolidated revenues, and this could be a problem for identifying the €50 million threshold. Banks would therefore be prudent to identify the correct sources of client revenue to get the benefit of the RWA reduction from SMEs (85% instead of 100%).

5 SMEs are defined as corporate exposures where the reported annual sales for the consolidated group of which the corporate counterparty is a part is less than or equal to €50 million for the most recent financial year.

Data improvements can therefore be obtained in the bank portfolios by adding/updating the SME indicator.

For retail exposures, further granularity has been introduced in Basel IV regulations for both the Standardized and IRB approaches.

Transactors are obligors for credit cards and charge cards where the balance has been repaid in full at each scheduled repayment date for the previous 12 months. Obligors in relation to overdraft facilities would also be considered as transactors if there have been no drawdowns over the previous 12 months. Revolvers, on the other hand, are obligors who only pay the minimum due payment for revolving products and do not qualify as “Transactors”. They carry a significant interest income as well as potential risks due to the nature of their spending activity. Consequently, transactors have a lower risk-weight assigned at 45% compared to revolvers (assigned at 75%).

The data aggregation of this indicator poses a unique challenge since banks will have to rely on historical data to populate this field.

It therefore becomes critical for the banks to tag these indicators in their revolving products (credit cards, charge cards and overdrafts), personal term loans and leases (instalment loans, auto loans and leases, student and educational loans, personal finance) and small business facilities and commitments.

While the importance of collateral information has been described in section 3.2, there are other parameters such as Liens (claims to the property) that could be useful to capture for banks dealing with real estate exposures and the application of the correct risk weights in Standardized Approach. Basel IV now prescribes the choice between the Whole Loan Approach or the Loan-Splitting Approach.6

In the Whole Loan Approach, the risk weight is applied to the total exposure amount and is based on the LTV Ratio and whether the loan repayment is materially dependent on the cash flows generated by the property. Meanwhile, in the Loan-Splitting Approach, the exposures that satisfy the criteria are split into 55% of the CRM value (risk weighted at 20%) and residual exposure risk weighted as that of the counterparty. Multiple options could be present wherein the bank has a Senior, Junior or an Intermediate lien on the property, and it would be prudent to capture this information.

Moreover, banks should emphasize on improving the underlying data captured for their PD/EAD/LGD modelling attributes and with the right degree of aggregation (counterparty/entity/exposure level).

6 BCBS D424: Page 22, paragraphs 64 and 65.

Overall, there is a lot of data preparation that needs to be done by banks for Basel IV implementation.

Some of the tasks to be Basel IV ready would involve higher complexities and may take longer processing times; for example, collateral sourcing. A mission-mode with strict timelines needs to be adopted and banks should start investing in the right people, policies, procedures, systems and databases to be well prepared for these regulatory deadlines.

Banks which were particularly relying on A-IRB for their Basel III calculations for most of their portfolios will face these challenges even more, since they will have to gather all accurate data pertaining to the Standardized approach due to the constraints on IRB.

Having supported some of the biggest banks in the Europe with their Basel IV implementation, Finalyse with its team of seasoned consultants can help you in mitigating the risks associated with such a large-scale project.

As time progresses, more banks will join the bandwagon to collect the most relevant information and deploy the right people to manage these activities. Those banks which account sufficiently for a parallel run to gauge the impact will end up having that competitive edge.

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support