Banks have long complained about the high complexity of the European regulatory environment.1 Recently, however, the various actors in European banking regulation and supervision seem to have listened. In October 2025, the European Banking Authority (EBA) published its Report on the efficiency of the regulatory and supervisory framework, 2 in which it announces the creation of the Task Force on the Efficiency of the Regulatory and Supervisory Framework (TFE). This task force has the mission to review four key areas of the current European banking regulatory framework in order to find potential simplifications. Simultaneously, the European Systemic Risk Board (ESRB) published a report 3 on streamlining and simplifying its supervisory tasks. Two months later, the European Central Bank (ECB) published the recommendations of its Governing Council’s High-Level Task Force on Simplification, with the aim of simplifying the European regulatory, supervisory and reporting framework for banks.

Following up this wave of regulation simplification ambitions, the EBA published the 9th February 2026 a discussion paper on the Simplification and assessment of the credit risk framework 4. This discussion has for main objective to support the efficiency and simplicity in the rules governing the calculation of credit risk Pillar 1 capital requirements. In a speech given in June 2025 5, the Chairperson of the EBA defined efficiency as “achieving the best result using our tools and resources in the best possible way and reducing any deterrent effects of complex regulations”, which is different from effectiveness, the focus on achieving the regulation goals.

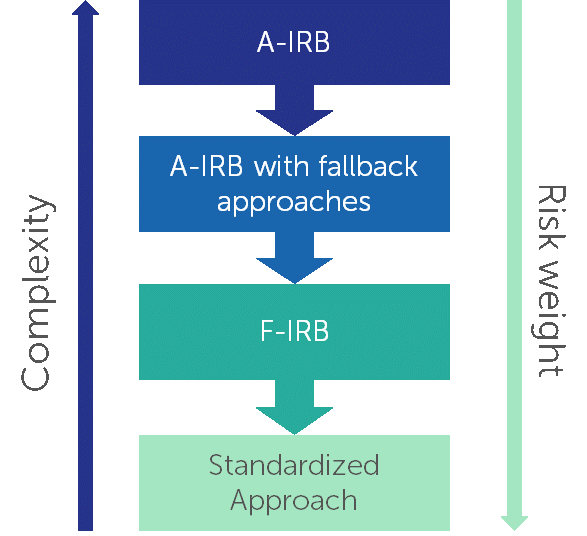

Most of the simplifications proposed in this discussion paper, especially those regarding the IRB models, are easier to implement than the current processes but are also conservative, in the sense they will increase the capital requirements if adopted. Those “fallback approaches” proposed introduce a new trade-off between simplicity and capital requirements’ efficiency for supervised entities: the simpler the approach, the more conservative it will be. Banks must now assess the burden of applying more complex regulatory items compared to simpler fallbacks: regulation becomes a spectrum between the most capital efficient but most complex methods (“full” A-IRB approach) and the simplest but most capital-intensive processes (Standardized Approach (SA)), with steps in-between (fallback approaches for specific items, F-IRB).

These fallback approaches may also provide on-site inspection teams and JSTs with more streamlined methods for imposing limitations 6 on A-IRB models. By establishing ready-made regulatory backstops, supervisors can more easily mandate conservative, "functioning" alternatives if specific components of an IRB model are deemed unsatisfactory.

In addition to fallback approaches that exchange simplicity for conservativeness there are several changes and opportunities in the EBA paper that could reduce undue (overly conservative by way of e.g. double counting) capital requirements. The request for comments is an opportunity for banks to assess where regulatory complexity has led to overly conservative distortions of their RWA calculations, for example through exploding levels of Margin of Conservatism.

In the end, the new regulatory framework that would be introduced by such simplifications would be hybrid approach in a continuum between risk-sensitive modelling (the EBA’s traditional point of view) 7 and conservative, simple rules of thumbs for capital requirements.

The proposed changes are of different categories:

Changes that are pure simplifications/harmonizations that should not have an RWA impact

Changes that offer banks the possibility to exchange a simplification for conservativeness

Changes that have potentially a larger RWA impact

Proposed change | IMPLEMENTATION impact | RWA impact |

Harmonizing SA Real Estate treatment | Pure harmonization | No or indirect impact |

ECAI’s use of implicit government support | Pure simplification | Increase |

Aggregate L2 and L3 IRB products, remove duplication | Pure simplification | No impact |

Harmonize testing requirements for Discrete and Continuous models | Medium to high depending on the results of the new tests on existing continuous models | No or very low impact |

Simplify definition of Facility | High for banks having different facility definitions for parameters | No or very low impact |

Harmonizing of representativeness | Low to medium | No or very low impact |

Simplified approach for MoC | Pure simplification | Increase or decrease |

Simplified approach for direct and indirect costs | Pure simplification | Increase |

Simplify the Downturn estimation | Pure simplification | Increase |

Simplify the LGDD estimation | Pure simplification | Increase |

Apply the fixed CCF to a larger scope | Pure simplification | Increase |

The impact on each portfolio will be different depending on both the composition of the portfolio and the way in which the rating system is set up.

Whether potentially significant simplifications occur will depend on the comments and suggestions that are provided by the banks and submitted before the 10th of May to EBA. Finalyse can help analyze the potential impact of the proposed changes to your specific situation with a workshop on the topic.

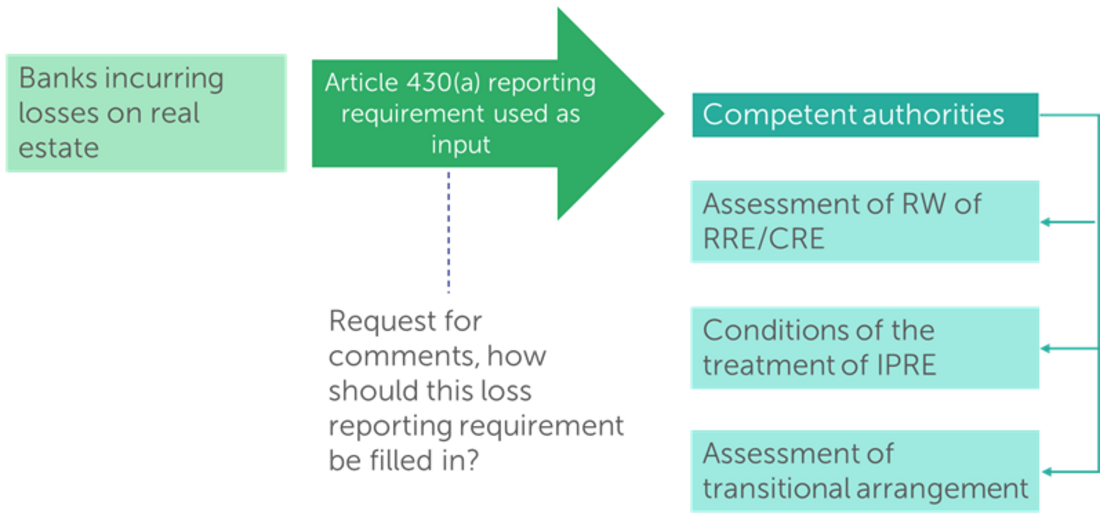

The EBA is consulting on how to harmonize the reporting of losses suffered on real estate exposures. Article 430(a) of the CRR requires banks to report “losses stemming from exposures for which an institution has recognized residential property as collateral”, however it has been confusing to banks how exactly this requirement should be filled in.

CRR 3 allows national supervisors a lot of room for derogation, articles 124(9), 125(2),126(2), 458, 465 and 133 allow for- or in practice lead to- derogations of the risk weighting of real estate. The EBA intends to acknowledge the specificity of the variance in national situations with regards to real estate, and the main harmonization the EBA proposes is w.r.t. article 430(a) of the CRR. Article 430(a) requires banks to report “losses stemming from exposures for which an institution has recognized residential property as collateral”. These reported losses feed in to the following decision making processes:

They are used by competent authorities (cf. art 124(9)) to assess if the risk weights for exposures secured by residential/commercial property (art. 125 and 126) are appropriate.

They are used by competent authorities (cf. art 125(2) and art 126 (2)) to consider the treatment of IPRE exposures as non-IPRE exposures.

They are considered in the member-state level decision to use article 465 to use a favorable transitional arrangement.

Since the introduction of the risk weight floor every bank with a real estate portfolio is exposed to standardized real estate calculations. Banks should assess the degree to which derogations relevant to the national market could help them or are currently hindering them. This is an opportunity to clarify your reporting requirements or remove unduly conservative requirements that are not appropriate to the market.

The EBA is consulting on how to implement the new rule excluding the consideration of implied government support in external credit ratings. If there is a good chance the institution will be supported by the government in case of a default, the debt is roughly as good as the government’s debt. A significant number of PSE’s and other institutions that are highly rated owe that to the implicit government support.

The impact of CRR article 138(g) is therefore significant for portfolios heavily exposed to large institutions that enjoy implied government support. The transitional arrangement allows the banks to use these credit rating until 31 December 2029. A potential disaster scenario turns every (previously A-AAA rated) institution with implied government support with a RW of about 20% into unrated exposures, for which the risk weight will be between 40% and 150%.

Fitch is the first Credit Rating Agent (CRA) to introduce an “ex-government support” (XGS) product compliant with article 138(g). To see an example of the XGS rating in action we take Qatar National Bank, when the implied government support is taken into consideration Fitch rates its long-term debt A+, however, its XGS rating is only BBBXGS+ 8, a drop of one credit quality step which results in a risk weight adjustment from 30% to 50%.

Both these scenarios could give a shock to the capital requirements of banks that goes beyond what CRR 138(g) bargained for. A case can be made that institutions rated AXGS (A rated without implied government support) are more robust than similar institutions with an A rating (possibly taking into account government support), furthermore clarification should be requested on the treatment of institutions for which no XGS rating is available.

EBA is considering consolidating the various guidelines, RTS and Q&As for credit risk, and potentially integrating environmental and social (E&S) risk into the credit risk framework. Since the publication of the first version of the CRR, numerous regulatory products have been published by the EBA related to the IRB models’ requirements, both a level 2 (RTS/ITS) 8 9 10 and level 3 (guidelines) 11 12 13 14 15 16 17 Although these regulatory texts help to clarify and specify regulatory expectations, their sheer number makes it difficult to find one's way through them.

Therefore, the EBA proposes to aggregate those items together by regulatory level or legal nature: the guidelines would be aggregated together and the RTS would be aggregated together into a separate item. Such bundling is meant to increase the readability of the credit risk regulation. While we agree that it will make the regulatory texts easier to navigate, we are also of the opinion that such bundling might make the readability of supervisory conclusions harder more opaque: past and on-going findings and recommendations/obligations will still refer to the old, disaggregated texts.

Secondly, the EBA proposes to integrate E&S risks in a more systematical manner into the credit risk parameters’ differentiation and quantification steps. While no details are given about such greater integration, we are of the opinion that it could be through the following propositions:

Prescribing mandatory E&S risk factors to be included in the list of risk drivers to be tested for risk differentiation

E&S overlay: on top of the PD grades, an ESG rating scale is mandatory, and the combination of the two ratings would up-notch or de-notch an exposure’s PD grade

An E&S risk-dedicated MoC (to cover for ESG data deficiencies 18 for example)

Incorporating specific E&S scenarios and risks in the valuation of collateral and guarantees 19

The integration of a climate-related downturn scenario for the LGD and CCF parameters

An E&S stress testing framework

We are of the opinion that, while such E&S risk integrations are interesting in themselves, they would add to the complexity of the regulatory framework instead of simplifying it.

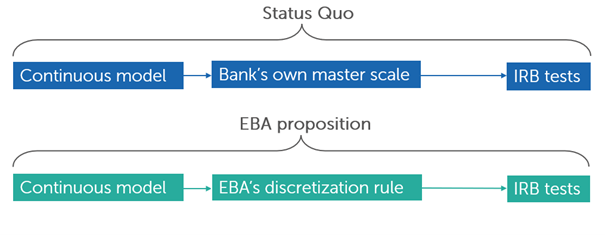

EBA considers developing a standard discretization for the continuous models for IRB testing purposes. CRR Article 169(3) allows banks to use direct estimates of a risk parameter and consider those estimates as being on a continuous rating scale. Such continuous scale would imply that each observation constitutes a grade in itself, and that the computation of own fund requirements is done on a continuous basis. 20

The use of a continuous scale provides challenges, particularly in terms of model validation, compared to the use of discrete scale models: it is impossible to directly test the homogeneity and heterogeneity, it is harder to directly test conservatism and the notion of overrides (usually done by “notching”) is fuzzier.

The EBA guidelines on PD and LGD estimation state that institutions should provide additional calibration tests at a level that is appropriate for the application of the PD or LGD model if using a continuous rating scale. 21 No further details are given by the EBA, leaving room for interpretation by the supervised entities and inspection teams (for example, testing directly on the full sample or slicing the continuous scale along discrete risk drivers).

To test for the accuracy of a continuous scale PD model is straightforward with the usual metrics (ROC curve and AUC) and statistical tests (Hosmer-Lemeshow 22 , Brier score) 23. An interesting test for accuracy when using a continuous rating scale is the Kolmogorov-Smirnov test, comparing the score densities of the defaulted and non-defaulted populations as this test is robust for imbalanced data.

The tricky part is to test for heterogeneity and homogeneity when there are no grades. For heterogeneity, a possible test with a continuous rating scale is the Cox Proportional Test 24, which runs a logistic regression of the realized defaults on the predicted default odds of the PD model, and concludes the model is heterogeneous if the slope is sufficiently close to unity and the intercept to the null.

With regard to homogeneity, a solution for continuous scale PD model is to use local smoothing (using a sliding window) in order to get a local slope. When the local slope deviates from the 45 degrees line, it indicates that there is a break of homogeneity locally. An example of such procedure is the LOESS (Locally Estimated Scatterplot Smoothing), for which it’s possible to formally test its deviation with respect to the 45 degrees straight line. 25

Another frequently used method is to map the continuous rating grades to the buckets of a master scale. Banks have a lot of discretion selecting this master scale, allowing them to use statistical methods to select a bucketing method that shows the model to have appropriate AUC, homogeneity, heterogeneity, and no overt concentration in any of the buckets.

In this discussion paper, the EBA proposes to add a requirement to have continuous rating scale discretized for the purpose of model validation (particularly for heterogeneity and homogeneity validation purposes). There are multiple possibilities for such discretization methods (equal-width binning, equal size binning, top-down binning procedures such as Multi Interval Discretization 26 or bottom-up binning such as Monotone Adjacent Pooling Algorithm 27). However, we tend to think that the chosen method would be simple enough to ensure its replicability and comparability across multiple banks and portfolios. The ECB, in its 2019 guide on reporting for validation results of internal models 28, states that the AUC should be calculated by mapping PD to a relevant master scale for continuous scale PD models, without specifying such master scale. However, it also specifies that for continuous LGD models, the gAUC should be calculated by mapping the LGD to an equal-width binning discretized scale. This is a possible avenue for future EBA recommendations regarding the discretization of continuous scale PD models.

A “one size fits all” method could introduce biases in model validation in our opinion, as the statistical tests might be inconclusive due to the sub-optimal nature of the discretization method instead of the poor performance of the direct estimate model.

EBA proposes to require banks to use a single definition of facility in their IRB rating system. CRR 3 introduced a new definition of what a facility is, allowing for the possibility of aggregating multiple contracts into a unique facility if it aligns the modelling with the business practices. Prior to this clarification, there was no clear definition of what a facility was, either in the CRR or by the EBA.

There is no obligation of consistency of the facility definition between parameters, meaning that the facility definition retained can be different for PD (for retail exposures, it is possible to define the default at facility level) and CCF. It is therefore possible for a bank to choose the facility level optimizing its capital requirements, such as having a single contract facility for the PD to limit the contagion and hence lower the realized default rate, and a multiple contracts facility to have different contracts balance cancelling each other and hence lowering the realized CCFs by circumventing the realized CCF floor to 0.

To illustrate this point, let’s suppose a retail customer have two revolving products, a credit card (limit of €5,000 and balance amount of €3,000) and an overdraft (limit of €2,000 and balance amount of €1,500). Just before defaulting, the client maxed out its overdraft (drawing €500) and used it to pay toward its credit card balance.

| Product | Undrawn amount at reference date | Net drawing | Realized CCF | Floored CCF | Obligor average CCF |

|---|---|---|---|---|---|

| Credit card | 3,000 | +500 | -16.6% | 0% | 50% |

| Overdraft | 500 | -500 | 100% | 100% | |

| Bundle | 3,500 | 0 | 0% | 0% |

By keeping the two contracts as separated facilities, the average CCF for this obligor is 50%, while by taking the two contracts as a single facility, the CCF drops to 0%, lowering the RWA.

In the discussion paper, the EBA is considering closing this arbitrage opportunity by forcing banks to adopt a single facility definition across all their parameters (at least for the same portfolio). It is, however, acknowledging that such additional guidance would force some banks to redevelop their models as they would have to change their current facility definition. Banks with models based on different facility definitions should seek to avoid sudden redevelopment burdens. We suggest proposing flexible transitionary measures to ensure a manageable migration to the updated framework.

Drawing on extensive experience with supervisory engagements, Finalyse can support banks in their IRB and standardized journey.

Finalyse has successfully helped clients:

Our consultants bring hands-on experience across regulatory, risk, and operational dimensions of credit risk, enabling institutions to move from concept to execution with confidence.

The remaining topics in the EBA simplification paper will be covered in a follow up article.

EBA is proposing simplifications in the capital calculation for Credit Risk.

Yes, this paper is a consultation and until the 10th of May relevant parties can submit their opinions and concerns.

Significant simplifications could lead to the forced redevelopment of IRB models, or could significantly increase RWA burden if the realized changes don’t take a particular bank’s concerns into account.

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support