In its continuous effort to harmonize the regulatory landscape and reduce undue Risk-Weighted Asset (RWA) variability across European banks, the European Banking Authority (EBA) has recently reviewed its Guidelines on the Definition of Default (DoD). In this amendment, the EBA reviewed the proposed changes introduced in its Consultation Paper (CP) on the DoD, namely:

A change in the 1% NPV loss threshold for forbearance NPE classification

A redesign of the forbearance NPE probation period

The introduction of guidelines on legislative moratoria

An extension of the technical past-due period for non-recourse factoring arrangements

Even if only this last change has been retained by the EBA in its final amendment to its DoD guidelines, it provides valuable insights and clarifications on its regulatory expectations regarding the DoD application, which we will detail in this blog post.

The EBA asked for a distinction between performing (PE) and non-performing (NPE) forborne exposures first in its 2013 ITS on reporting. No clear guidance on how to separate between performing and non-performing forbearance was given, resulting in wide differences in practice among banks, as highlighted by the Quantitative Impact Study of 2016. To remediate this variability, the NDoD introduced the NPV test for forbearance measures:

$$DO = \begin{array}{c} NPV_0 - NPV_1 \\ \hline NPV_0 \end{array}$$

Where \(NPV_1\) is the net present value of the contractual cash flows after the concession and \(NPV_0\) is the net present value of the contractual cash flows before the concession. To be close to the IFRS9 accounting norms, the discounting of the cash flows is done using the original contract’s effective interest rate.

A contract is considered as NPE (and the obligor/facility defaulted) if the NPV test is greater than 1%. In its CP, and now in the amendment of the guidelines, the EBA precises that the goal of the test is to distinguish between the concessions that will result in no diminished financial obligations for the obligor, and those that will mechanically introduce a loss for the bank. The 1% threshold is mainly chosen as a way to avoid any “technical” default due to minor discounting or rounding effects that would result by the adoption of a 0% threshold, such as:

Tiny NPV loss due to the rounding of the monthly principal and interest payment

Day count conventions (30/360, Actual/365…)

“de minimis” or nuisance amount adjustment (rounding of the payments and final payment adjusting the balance)

Changes in compounding frequency with rounding of the new contractual interest rate

It is interesting to note that there are currently different supervisory practices with respect to the calculation of this NPV threshold. For example, the Danish Supervisor allows for a delay in the NPV calculation if the institutions automatically classify the forborne exposures as defaulted.

In the CP, a 5% threshold has been considered to replace the 1% threshold currently in place. The idea behind such an increase is that the action of putting a facility or obligor into default has stronger effects than solely the recording of the loss, and hence a low NPV test threshold has a disproportionate effect on the banks’ provisioning. Indeed, defaulting a forborne exposure will result in:

Stage 3 provisioning

Contagion to other exposures in case of a default definition at obligor level or if the pulling effect is triggered

Increase of the recorded number of defaults, which will affect the backtesting and future calibration of IRB PD models

Increase of RWA (due to the fact to have defaulted exposures on the balance sheet) both standardized and IRB approaches

Operational and reputational costs of putting a client into default (collateral revaluation, margin call, change in commercial conditions…)

However, the EBA opposed this change of threshold. First and foremost, it considered it would defeat the purpose of the forbearance framework (Introduced by the EBA/ITS/2013/03 and extended by the EBA/GL/2018/06) which prevents the use of multiple restructurings to financially distressed obligors in order to avoid recording defaulted exposures (a practice also known as “zombie lending”). Indeed, a bank could grant a concession leading to a loss of 4.5%, and then another one, without recording a default, while getting a loss of more than 8.7% on the exposure.

A second argument used by the EBA is that a 5% threshold would create inconsistencies with the relative materiality threshold of 1% for the counting of the days past due (DPD). The idea here is that setting a forbearance materiality threshold higher than 1% creates an opportunity for 'regulatory arbitrage.' It would allow lenders to grant concessions to borrowers who have already breached the 1% DPD materiality threshold and are approaching 90 days past due without classifying them as NPEs, provided the NPV loss remains below the higher forbearance materiality threshold. Such an argument is however weak as it mixes up a threshold calculated at the facility level (the NPV loss test) and a threshold calculated at the obligor level (the DPD materiality threshold). Furthermore, it compares a loss (the write-off in NPV due to the concession) with a delay in repayment, which will potentially be repaid in the future.

A third argument put forward by the EBA is that banks are highly levered with regulatory leverage ratios around 5%, so a loss between 1% and 5% on a material part of their portfolio could almost wipe out their Tier 1 capital. Such an argument is, however, far-fetched in our opinion as it extrapolates the threshold calculated on a single facility with the bank-level capital buffer.

Some respondents of the CP argued that the 1% fixed NPV loss threshold doesn’t enable a fair and accurate NPE classification because the characteristics of the loan (interest rate, maturity) will impact the NPV for a given concession. For example, longer maturities amplify the impact of grace periods or loans originated during high-interest rate periods trigger the NPV loss threshold.

The EBA is however opposed to make the NPV threshold characteristic depend for two main reasons:

The loan characteristics (such as maturity and interest rate level) reflects the inherent risk of the obligor/facility, so if a change of contractual arrangement has a greater impact due to those characteristics, it signals that the concession is riskier and this grater riskiness is captured by the NPV

Introducing a loan characteristic-dependent NPV threshold would complexify the default framework and make it harder to supervise

In the CP, the EBA proposed two changes to the forbearance NPE probation period (PP) exit criteria. First the EBA proposed to shorten the probation period of non-performing forborne exposures to 3 months, from one year previously, under the condition that the forbearance was classified as NPE due to a NPV loss above 1% but below 5%.

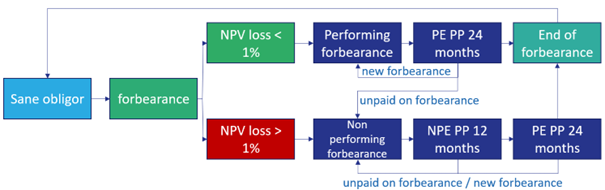

In the current forbearance framework, there are three reasons (see figure 1 below) for which a forborne exposure can be (re)classified as NPE:

An NPV test indicating a loss larger than 1%

A significant amount of arrears (30DPD) during any probation period

A new forbearance has been granted on a forborne contract that has been previously classified as NPE

A second proposition is to condition the exit from forborne NPE status to a material payment equal to the amount that has been written-off by the concession granted, capped at 20% of the principal outstanding prior to the concession.

We are of the opinion that aligning the NPE forborne PP to the other default PP would have made granting forbearance measures more attractive. First, the duration of the default period, due to the effect discounting of cash flows (EBA/GL/2017/16 paragraph 143), has a strong influence on the RWA impact of defaults. Second, reducing the length of the NPE period would hasten the exit of the NPE status and hence reduce the effect of NPE prudential backstops on CET1 capital. However, the proposed changes to the framework, conditioning the length and exit of the PP to additional calculations would have complexified unduly the already burdensome forbearance framework. Furthermore, the one-year NPE PP aligns with the length of the prudential backstop pause triggered by the granting of a forbearance to an already NPE exposure.

None of these changes have been retained and hence the forbearance framework remains unchanged: the NPV loss threshold remains at 1% and the NPE probation period stays at 12 months, without any further exit conditions.

In response to the increasing likelihood of recurring climate-related crises, the EBA considered whether to permanently embed rules for "general payment moratoria" into its Guidelines on the DoD. Such rules would clarify the process guiding exceptional moratoria, such as the one issued during the COVID-19 pandemic. The central regulatory concern regarding such moratoria is that, by allowing automatic concessions to borrowers, they would trigger a mass classification of loans classification as forborne (potentially NPE) under the current DoD.

The EBA rejected the idea of introducing a dedicated exemption related to moratoria as it would enable a Member State to issue a legislative moratorium whenever a specific crisis is affecting its territory. Such possibility would go against the objective of harmonisation of the DoD and would introduce undue RWA variability.

A factoring arrangement implies that a business sells its accounts receivable (unpaid customer invoices) to the factor (here the bank) at a discount in exchange for immediate cash. We can distinguish the recourse factoring arrangement, for which the business assumes the risk of non-payment from the customer, and the non-recourse factoring arrangement, for which the factor assumes the risk of non-payment from the customer.

In the latter case, the EBA recognizes that the counting of DPD does not reflect the specificities of the arrangement. Indeed, the payment is invoice-based: the customer does not owe a total amount but instead receives a distinct invoice for each service provided and each invoice has its own due date.

The regulatory definition of default focuses on the continuous period during which a customer has a past-due amount and does not differentiate by invoice. Hence, the counter starts the first day an amount is past due and does not reset to zero until the customer has paid off all their past-due amounts. In case of sequential late payments (a customer is constantly late on each of their invoice but by less than 30 days each time, for example paying their January’s invoice in February, their February’s invoice in March, etc…), the DPD counter will not reset to zero and will continue to increase, leading to a default even if the customer is a late payer by one month each time. This applies for both facility-level and obligor-level DoD, as the DPD clock continues to tick from facility to facility.

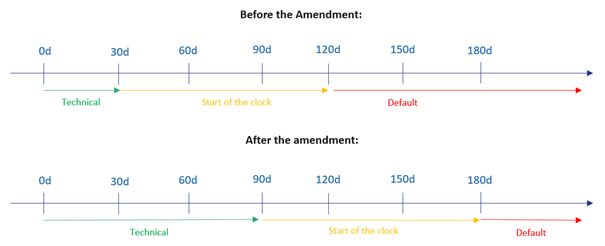

To not discourage institutions from offering non-recourse factoring arrangements, the EBA agreed in the DoD amendment to increase the technical past due situation from 30 days to 90 days. This implies that any past due amount above the 1% materiality threshold does not trigger the DPD count as long as the obligor is past due for less than 90 days (compared to 30 days previously, see figure 2).

We are of the opinion that this change has the potential to dramatically lower the observed default rate of non-recourse factoring portfolios, especially for PSE exposures which have lengthy administrative processes to validate their invoices.

Some respondents to the CP proposed extending this special treatment of the DPD count to operational leasing, i.e. a commercial rental agreement where a business (the lessee) rents an asset from a leasing company (the lessor) for a specific period, without taking ownership of the asset at the end of the contract. They draw a parallel between non-recourse factoring and operational leasing, as both are invoice-based and have overlapping instalments (new financial commitments before the previous expired).

The EBA ruled against this extension of the technical DPD to operational leasing as it argues that, whereas non-recourse factoring is a tri-partite arrangement, there is a direct contractual relationship in the case of leasing and hence the credit institution has full control of the payment collection process.

Two other modifications are introduced in this amendment to the DoD guidelines:

The removal of the notion of “distressed restructuring” in the guidelines due to the fact CRR3 replaced it by a direct reference to a “forbearance measure” in article 47b.

Removal of the passages mentioning the 180DPD exception, as this exception has been removed by CRR3.

Are you looking to simplify your IRB model landscape? To put a stop to the sprawling repair programs and countless findings? Drawing on extensive experience with supervisory engagements, Finalyse can support banks in their IRB and standardized approach journey.

Finalyse has successfully helped clients:

Ensure compliance with regulatory expectations (CRR and EBA)

Redevelop their IRB models

Implement their standardized capital calculation

Validate the IRB rating chain (models, data and governance)

Optimize their RWA calculation and remove unnecessary capital burden

Our consultants bring hands-on experience across regulatory, risk, and operational dimensions of credit risk, enabling institutions to move from concept to execution with confidence.

The European Banking Authority (EBA) reviewed its Guidelines on the Definition of Default (DoD), as per Article 178(7) of Regulation (EU) No 575/2013 (CRR).

The EBA initially proposed four key updates in its Consultation Paper: - A change to the 1% NPV loss threshold for forbearance NPE classification. - A redesign of the forbearance NPE probation period. - New guidelines regarding legislative moratoria. - An extension of the technical past-due period for non-recourse factoring.

Only one: the EBA ultimately decided to retain just the last point: extending the technical past-due period for non-recourse factoring arrangements. The other three proposals were dropped.

Finalyse InsuranceFinalyse offers specialized consulting for insurance and pension sectors, focusing on risk management, actuarial modeling, and regulatory compliance. Their services include Solvency II support, IFRS 17 implementation, and climate risk assessments, ensuring robust frameworks and regulatory alignment for institutions. |

Check out Finalyse Insurance services list that could help your business.

Get to know the people behind our services, feel free to ask them any questions.

Read Finalyse client cases regarding our insurance service offer.

Read Finalyse blog articles regarding our insurance service offer.

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department

Designed to meet regulatory and strategic requirements of the Actuarial and Risk department.

Designed to provide cost-efficient and independent assurance to insurance and reinsurance undertakings

Finalyse BankingFinalyse leverages 35+ years of banking expertise to guide you through regulatory challenges with tailored risk solutions. |

Designed to help your Risk Management (Validation/AI Team) department in complying with EU AI Act regulatory requirements

A tool for banks to validate the implementation of RWA calculations and be better prepared for CRR3 in 2025

In 2027, FRTB will become the European norm for Pillar I market risk. Enhanced reporting requirements will also kick in at the start of the year. Are you on track?

Finalyse ValuationValuing complex products is both costly and demanding, requiring quality data, advanced models, and expert support. Finalyse Valuation Services are tailored to client needs, ensuring transparency and ongoing collaboration. Our experts analyse and reconcile counterparty prices to explain and document any differences. |

Helping clients to reconcile price disputes

Save time reviewing the reports instead of producing them yourself

Helping institutions to cope with reporting-related requirements

Be confident about your derivative values with holistic market data at hand

Finalyse PublicationsDiscover Finalyse writings, written for you by our experienced consultants, read whitepapers, our RegBrief and blog articles to stay ahead of the trends in the Banking, Insurance and Managed Services world |

Finalyse’s take on risk-mitigation techniques and the regulatory requirements that they address

A regularly updated catalogue of key financial policy changes, focusing on risk management, reporting, governance, accounting, and trading

Read Finalyse whitepapers and research materials on trending subjects

About FinalyseOur aim is to support our clients incorporating changes and innovations in valuation, risk and compliance. We share the ambition to contribute to a sustainable and resilient financial system. Facing these extraordinary challenges is what drives us every day. |

Finalyse CareersUnlock your potential with Finalyse: as risk management pioneers with over 35 years of experience, we provide advisory services and empower clients in making informed decisions. Our mission is to support them in adapting to changes and innovations, contributing to a sustainable and resilient financial system. |

Get to know our diverse and multicultural teams, committed to bring new ideas

We combine growing fintech expertise, ownership, and a passion for tailored solutions to make a real impact

Discover our three business lines and the expert teams delivering smart, reliable support